2020 BDC List And The Top 4 BDCs For High Income

Business Development Companies, otherwise known as BDCs, are highly popular among income investors. BDCs widely have high dividend yields of 5% or higher. The strongest BDCs also have the ability to raise their dividends on occasion. This makes BDCs very appealing for income investors such as retirees, especially in a low interest rate environment.

With this in mind, we’ve created a list of the BDCs we currently cover in the Sure Analysis Research Database.

You can download your free copy of our BDC list, along with relevant financial metrics such as P/E ratios and dividend payout ratios, by clicking on the link below: Click here to download your BDC Excel Spreadsheet List now.

Of course, before investing in BDCs, investors should understand the unique characteristics of the sector. This article will provide an overview of BDCs, as well as our top 4 BDCs right now as ranked by expected total returns over the next five years.

Overview of BDCs

Business Development Companies are closed-end investment firms. Their business model involves making debt and/or equity investments in other companies, typically small or mid-size businesses. These target companies may not have access to traditional means of raising capital, which makes them suitable partners for a BDC. BDCs invest in a variety of companies, including turnarounds, developing, or distressed companies.

BDCs are registered under the Investment Company Act of 1940. As they are publicly-traded, BDCs must also be registered with the Securities and Exchange Commission. To qualify as a BDC, the firm must invest at least 70% of its assets in private or publicly-held companies with market capitalizations of $250 million or below.

BDCs make money by investing with the goal of generating income, as well as capital gains on their investments if and when they are sold. In this way, BDCs operate similar business models as a private equity firm or venture capital firm. The major difference is that private equity and venture capital investment is typically restricted to accredited investors, while anyone can invest in publicly-traded BDCs.

Why Invest In BDCs?

The obvious appeal for BDCs is their high dividend yields. It is not uncommon to find BDCs with dividend yields above 5%. In some cases, certain BDCs provide 10%+ yields. Of course, investors should conduct a thorough amount of due diligence, to make sure the underlying fundamentals support the dividend. As always, investors should avoid dividend cuts whenever possible. Any stock that has an abnormally high yield is a potential danger.

Indeed, there are multiple risk factors that investors should know before they invest in BDCs. First and foremost, BDCs are often heavily indebted. This result is commonplace across BDCs, as their business model involves borrowing to make investments in other companies. The end result is that BDCs are often significantly leveraged companies.

When the economy is strong and markets are rising, leverage can help amplify positive returns. However, the flip side is that leverage can accelerate losses as well, which can happen in bear markets or recessions.

Another risk to be aware of is interest rates. Since the BDC business model heavily utilizes debt, investors should understand the interest rate environment before investing. For example, rising interest rates can negatively affect BDCs if it causes a spike in borrowing costs. That said, BDCs may benefit from falling interest rates. In the current climate of low interest rates, many BDCs could see a tailwind.

Lastly, credit risk is an additional consideration for investors. As previously mentioned, BDCs make investments in small to mid-size businesses. Therefore, the quality of the BDC’s portfolio must be assessed, to make sure the BDC will not experience a high level of defaults within its investment portfolio. This would cause adverse results for the BDC itself, which could negatively impact its ability to maintain distributions to shareholders.

Another unique characteristic of BDCs that investors should know before buying is taxation. BDC dividends are typically not “qualified dividends” for tax purposes, which is generally a more favorable tax rate. Instead, BDC distributions are taxable at the investor’s ordinary income rates, while the BDC’s capital gains and qualified dividend income is taxed at capital gains rates.

After taking all of this into account, investors might decide that BDCs are a good fit for their portfolios. If that is the case, income investors might consider one of the following BDCs.

The Top 4 BDCs Today

With all this in mind, here are our top 4 BDCs today, ranked by expected total returns over the next five years. Stocks are listed from lowest to highest expected five-year return.

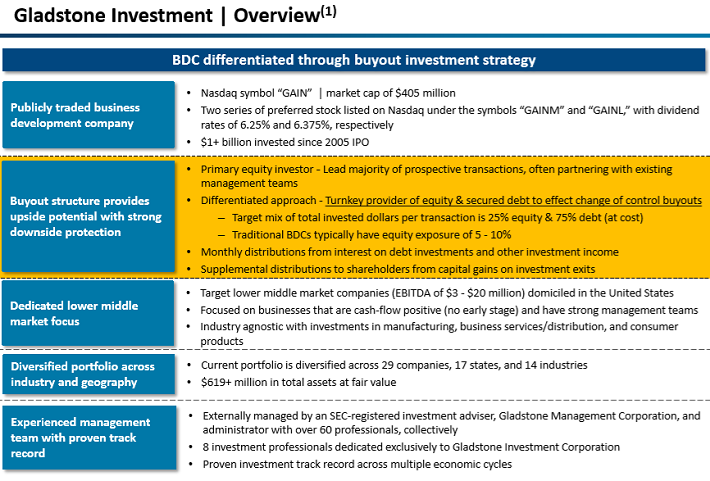

BDC #4: Gladstone Investment Corp. (GAIN)

Gladstone Investment is BDC that focuses on U.S.-based small- and medium-sized companies. Industries which Gladstone Investment targets include aerospace & defense, oil & gas, machinery, electronics, and media & communications. Gladstone Investment was founded in 2005, and trades with a market capitalization of just $450 million.

Gladstone Investment’s business model is relatively straightforward. The company lends money to small- and mid-sized companies. Position sizes for debt investments usually range from $5 million to $30 million. The company also takes equity stakes in such companies, with position sizes for equity investments typically ranging from $10 million to $40 million.

Source: Investor Presentation

The companies Gladstone Investment does business with usually cannot access debt or equity markets directly, as bond sales and public listings are not possible for them due to their small size. Gladstone Investment makes its money via spreads between the interest rates the company pays on cash that it borrows, and the interest rates the company receives on cash that it lends – the same principle as with banks.

Declining interest rates could turn into a headwind, but during the most recent quarter Gladstone Investment’s weighted average interest yield was actually up on a year-over-year basis, to 15.0%. The company generates additional earnings through appreciation of its equity investments.

Gladstone Investment reported its second quarter (fiscal 2019) earnings results on November 4. The company generated total investment income – Gladstone Investment’s revenue equivalent – of $16.6 million during the quarter, which represents a decline of 3.9% compared to the prior year’s quarter. This number beat the analyst consensus estimate easily, by $2.6 million, as analysts expected an even bigger decline for the company’s top line.

Gladstone Investment’s adjusted net investment income-per-share totaled $0.23 during the second quarter, which was in line with what the analyst community had estimated. Adjusted net income-per-share was down from $0.25 in the previous year’s quarter.

Gladstone is a monthly dividend stock, meaning it pays a dividend every month instead of once per quarter like most stocks. It recently raised its monthly dividend by 2.9%, to $0.07 per share. Annualized, the $0.84 per share dividend payout represents a high yield of 6.1%. We expect total returns of 5%-6% per year over the next five years, made up mostly of dividends as NII per share will likely be offset by a declining valuation multiple.

BDC #3: Prospect Capital Corporation (PSEC)

Prospect Capital Corporation provides private debt and private equity to middle-market companies in the U.S. The company focuses on direct lending to owner-operated companies, as well as sponsor-backed transactions.

Prospect invests primarily in first and second lien senior loans and mezzanine debt, with occasional equity investments. Prospect’s investment objective is to generate current income and long-term capital appreciation. The company went public in 2004 and currently has a market capitalization of ~$2.4 billion.

Source: Investor Presentation

Prospect reported first fiscal-quarter earnings on 11/6/19 and results met consensus, but were weak on a year-over-year basis. Net investment income came to $71.1 million, down sharply from the $85.2 million in the year-ago period. Net Asset Value (NAV) declined year-over-year from $9.39 to $8.87 as a result of the fair value of the company’s investments declining year-over-year and quarter-over-quarter to $5.45 billion.

Prospect’s annualized current yield on its portfolio of investments also declined from 10.6% to 10.2%. Prospect originated $95 million in new loans in Q1, but received $245 million in repayments. This led to a shrinking of the company’s portfolio as it was reduced in size by $150 million in Q1.

Growth has been tough to come by for Prospect for the past decade. Since 2012, net investment income has struggled to grow. Part of this is due to Prospect’s prodigious share count, which is about six times higher today than it was a decade ago. While it is typical for a BDC to issue shares to fund acquisitions, Prospect’s dilution has been excessive.

Given this history of dilution and weak net investment income performance, we don’t expect NII growth on a per share basis. This will weigh on future returns. Fortunately for investors, the stock has a very high yield of 11%. However, we expect the valuation multiple to decline and reduce annual returns by 3%-4% annually through 2025. Total returns are therefore expected in the 7%-8% range each year, over the next five years.

BDC #2: Main Street Capital (MAIN)

Main Street provides long-term debt and equity capital to lower middle market companies and debt capital to middle market companies. Main Street defines lower middle market companies as generally having annual revenues between $10 million and $150 million. The company’s investments typically support management buyouts, recapitalizations, growth financings, refinancing and acquisitions.

As of the end of third quarter 2019, Main Street had an interest in 68 lower middle market companies, 52 middle market companies and 62 private loan investments. The company has a market capitalization of $2.8 billion and generated $157 million in net investment income last year.

Main Street has generated impressive growth in NII, NAV, and dividends over the past decade.

Source: Investor Presentation

On November 7th, Main Street Capital released third quarter results and reported net investment income of $39.0 million, a 2% increase compared to $38.1 million a year ago. The corporation generated net investment income per share of $0.62 per share, down 1.6% from last year’s income of $0.63. Distributable net investment income totaled $0.66 per share, identical to the third quarter of 2018.

Main Street’s net asset value increased $0.11 to $24.20 since the start of 2019, an increase of 0.5%. Adjusting for the semi-annual supplemental cash dividend, net asset value would have increased by $0.36 per share, or 1.5%.

The company completed $25.5 million in total lower middle market portfolio investments, $8.8 million of which was issued to a new company in the lower middle market portfolio. The lower middle market portfolio had a net decrease of $9.8 million, while the middle market and private loan portfolios were both higher by $26 million, and $32 million.

We estimate total returns near 8% per year moving forward, consisting of the 5.5% yield, 4.0% expected NII per share growth and a ~2% negative reduction from multiple valuation compression.

BDC #1: Ares Capital Corporation (ARCC)

Ares Capital Corporation is a specialty finance BDC. It focuses on generating both current income and capital appreciation through debt and equity investments. The company invests primarily in U.S. middle-market companies, as well as larger companies.

Its portfolio is comprised of first and second lien senior secured loans as well as mezzanine debt, diversified by industry and sector. The company was founded in 2004 and has a market capitalization of ~$8 billion.

Source: Investor Presentation

ARCC reported its third-quarter results on October 30th, with $0.48 in earnings-per-share beating consensus estimates of $0.46, and rising from $0.45 in the year-ago quarter. NAV also has risen to $17.26 from $17.12 at the beginning of the year. Net investment income grew considerably during the quarter to $212 million, up from $185 million in the year-ago quarter.

The company also continued to make substantial investments by deploying $2.41 billion in additional capital during the quarter, dwarfing the $1.42 billion in exits made during the same period. Its new investments were allocated as follows: 90% into first lien senior secured loans, 7% in second lien senior secured loans, 2% in other equity securities, and 1% in subordinated certificates of the SDLP (96% of which were in floating rate debt securities). As of October 24th, the company had an investment backlog of $665 billion and a pipeline of $265 million.

Ares Capital’s strong 2018 and first three quarters of 2019 investment income growth was driven by high LIBOR, improved aggregate portfolio yields, and limited credit issues. Management’s repeated dividend hikes and significant insider purchases in recent quarters backs their confident rhetoric that this level of earnings is sustainable for the foreseeable future.

Additionally, management recently extended its stock repurchase plan for another year and increased its size from $300 million to $500 million (nearly 7% of shares outstanding at current prices), with the announced intent of repurchasing shares should they drop below NAV. As a result, the share price and potentially earnings-per-share have some solid tailwinds behind them.

That said, the highly leveraged state of the economy and several signals that it may be slowing combine with the company’s choppy earnings history to make us cautious on the company’s growth prospects. As a result, we assume an annual growth rate of just 1% over the next five years.

Ares Capital is arguably the safest BDC given that it is the only one with investment-grade ratings from all three major rating agencies. Additionally, its balance sheet is in a very strong position with solid and stable asset quality and a diversified long-duration liability structure. It also has very diversified holdings (342 different companies) with weighted average interest coverage of 2.1 times, minimizing default risk. Its competitive advantage comes from its superior size and scale as one of the largest BDCs.

We view Ares stock as fairly valued. Overall, total returns are expected to slightly exceed 9% per year, comprised of 1% annual NII growth and the 8.4% dividend yield.

Final Thoughts

Business Development Companies allow everyday retail investors the opportunity to invest indirectly in small and mid-size businesses. Previously, investment in early-stage or developing companies was restricted to accredited investors, through venture capital.

And, BDCs have obvious appeal for income investors. BDCs widely have high dividend yields above 5%, and many BDCs pay dividends every month instead of the more typical quarterly payment schedule.

Of course, investors should consider all of the unique characteristics, including but not limited to the tax implications of BDCs. Investors should also be aware of the risk factors associated with investing in BDCs, such as the use of leverage, interest rate risk, and default risk.

If investors understand the various implications and make the decision to invest in BDCs, the four individual stocks on this list could provide attractive total returns and dividends over the next several years.

Disclaimer: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more