Image: Bigstock

Thursday seemed poised to be a brutal day for the stock market, with S&P 500 futures down big on Wednesday night before stocks opened over 2% lower as Wall Street reacted to increased Russian aggression in Ukraine. The Nasdaq was down 3% on Thursday and it was well into bear market territory before it mounted an incredible rally to finish the day 3.3% higher.

Stocks surged again on Friday on reports that Moscow is prepared to hold talks with Ukrainian leadership, though the conflict is still ongoing. The geopolitical situation is in flux, and attempting to forecast what will happen next is extremely difficult. The last week, however, does highlight why some investors might want to stay exposed to the market even during turmoil.

The ratcheted up geopolitical tensions have sent tremors through Wall Street. The prospect of higher interest right around the corner is also at the top of many investors' minds. Yet, a fair amount of the current worries have been priced into the market, with the Nasdaq 15% off its records and the S&P 500 still down around 9%.

Taking into account all of the legitimate concerns and acknowledging the uncertainties ahead, investors with longer-term horizons might want to consider buying stocks now and holding. And even with rising prices, and all of the other aforementioned factors tugging at the market, the outlook for S&P 500 earnings, revenue, and margins are strong for 2022 and 2023.

Today, we will explore a couple of Zacks Rank #1 (Strong Buy) stocks from different sectors that offer investors exposure to stable long-term growth, as well as great value, at the moment.

Image Source: Zacks Investment Research

Gildan Activewear Inc. (GIL - Free Report)

Gildan is a clothing company that many people might not even know they own. The company is essentially a wholesaler of everyday basic apparel that are most often branded by some other entity. If one were to look in their closet at any vacation destination T-shirt, school sweatshirt, or company polo, there’s a great chance at least one of them is made by Gildan.

Gildan’s diverse portfolio includes its namesake, American Apparel, Comfort Colors, GoldToe, and others. Its products feature sweatshirts/fleece, T-shirts & tanks, socks, activewear, underwear, and many other basic wardrobe staples. And GIL’s ability to operate in the background makes it less susceptible to the ever-changing fashion world.

The pandemic hit Gildan hard, with revenue down 30% last year. But it bounced back in 2021, with revenue up 48% to $2.9 billion to surpass its pre-COVID-19 total. The firm also swung from an adjusted loss of -$0.18 a share to +$2.72 per share. GIL beat our Q4 earnings estimate by 31% on Feb. 23, with it having beaten our EPS projection by an average of 67% in the trailing four quarters.

Image Source: Zacks Investment Research

Analysts have upped their FY22 and FY23 earnings estimates since the report to help it land its Zacks Rank #1 (Strong Buy). Zacks estimates call for its FY22 revenue to climb another 6% and for its adjusted earnings to pop another 3.3% higher, with more top and bottom-line growth expected in 2023.

Gildan reinstated its buyback program in August and its strong free cash flow has helped it reduce its debt load. The firm’s dividend yield sits at 1.6% at the moment to top the S&P 500 average. Plus, its Textile – Apparel space lands in the top 11% of over 250 Zacks industries, and Wall Street is high on the stock, with seven of the nine brokerage recommendations Zacks has at “Strong Buys” or “Buys.”

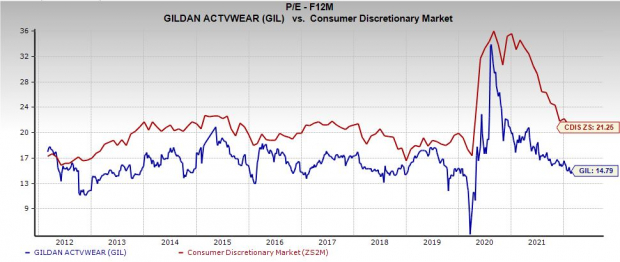

GIL shares have climbed 200% in the past decade to double its sector and blow away its industry’s 56% average. This outperformance is more striking in the last 12 months, with Gildan up 28% vs. the S&P 500’s 13% run. At roughly $39.08 a share, GIL trades 10% below its November records.

Plus, it trades at a 33% discount to its year-long highs at 14.8X forward 12-month earnings. It also trades at a discount to its 10-year median and offers great value compared to the Consumer Discretionary Market’s 21.2X.

KB Home (KBH - Free Report)

KB Home is one of the largest U.S. homebuilders, currently operating in nearly 50 markets, including popular areas within Colorado, Arizona, Texas, California, and Nevada. KBH allows buyers to customize many aspects of their homes. KBH is also committed to more energy-efficient offerings, with the firm boasting it’s “the first builder to make every home we build ENERGY STAR certified.”

KBH has benefited from the booming COVID-19 housing market that’s been driven by low interest rates, the desire for more space, and other bullish factors. Better still, millennials are finally fueling the market and will likely continue to for at least the near future. This plays into KBH’s strength since a majority (62% in 2021) of its clients are first-time buyers.

The housing market remains hot, with existing-home sales up 6.7% in January from December. Most importantly, reports suggest the U.S. housing market is millions of single-family homes short of demand. And even though interest rates are rising, 30-year mortgage rates are now around where they were in the front half of 2019 and well within their range during the past 10 years, at 3.89%.

Image Source: Zacks Investment Research

KBH topped Zacks Q4 earnings estimates in January, with FY21 revenue up 37%. KB Home closed the year with a $4.95 billion backlog, up 67% year-over-year. Company executives raised their 2022 outlook and projected an average selling price between $480 thousand to $490 thousand, which marks a significant jump from 2021’s $423 thousand average, as rising prices reach every corner of the economy.

Zacks estimates call for KB Home’s 2022 sales to surge another 30% to $7.5 billion, with FY23 set to climb 12% higher. Meanwhile, its adjusted earnings are expected to soar 68% and 10%, respectively. And analysts have lifted their EPS projections since its fourth quarter release. KBH’s 2022 consensus EPS estimate has improved by 29%, with FY23 25% higher, which helps it grab its Zacks Rank #1 (Strong Buy).

KBH shares have jumped 115% in the last five years to outclimb its industry’s 80% and the S&P 500’s 90%. The stock has cooled off, with it down 5% in the last year and 14% in 2022. KB Home's stock popped on Friday, and it still trades roughly 25% below its May records at around $38.32 a share.

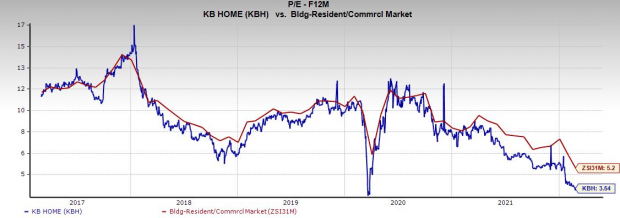

Even though KB Home stock is up 245% in the past 10 years vs. the S&P 500’s 230% and its industry’s 195%, it trades at roughly decade-long lows (outside of the COVID-19 selloff) at 3.5X forward 12-month earnings.

KB Home’s valuation marks a 60% discount to its own five-year median, 80% vs. its highs, and 33% against its peers. On top of all of that, KBH’s Building Products-Home Builders space ranks in the top 6% of over 250 Zacks industries and its 1.6% dividend yield tops the S&P 500 1.3%.

Comments

Log in or sign up to join the conversation.