2 Tech Stocks To "Buy The Dip"

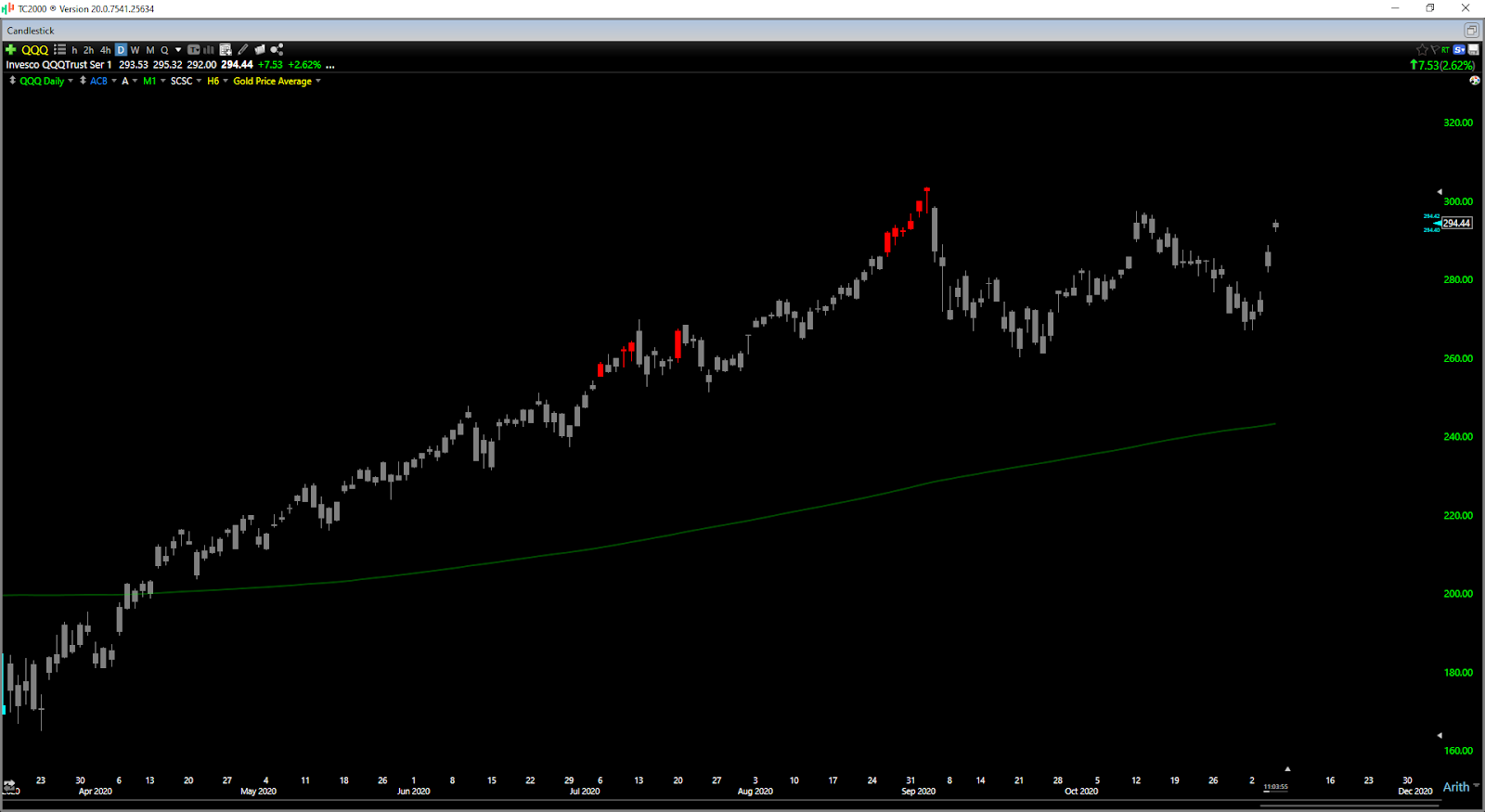

It’s been a wild start to November for investors with the Nasdaq Composite (COMP) coming off of its worst 5-day stretch since September, before following that up with one of its strongest rallies all year. The Nasdaq is now less than 3% from new all-time highs, which has led to a surge in demand for leading growth stocks.

Fortunately, while the Nasdaq Composite is beginning to get a little extended short-term, there are a couple of tech stocks have spent the past month pulling back to support levels that are getting closer to low-risk buy areas. These names are both leaders in their respective industry groups when it comes to sales growth, and they should be at the top of one’s shopping list. Let’s take a closer look at them below:

(Click on image to enlarge)

(Source: TC2000.com)

Zillow Group (ZG) and Avalara (AVLR) don’t have a ton in common other than being relatively newer public companies, but both are sporting strong sales growth and have unique products & services that give them a long runway for growth. In Zillow’s case, the company has de-cluttered the home buying and selling process with its new Zillow ‘Offers’. This allows anyone looking to sell their home the ability to get a cash offer from Zillow without showing the home, worrying about staging it, or having to wait for a drawn-out closing date.

In Avalara’s case, the company is the #1 software product for automated tax compliance, with AvaTax helping businesses navigate the confusing tax laws that differ from state to state. Both companies posted 25% plus sales growth in their most recent quarter, and fund ownership for each name has climbed for three consecutive quarters as growth funds prepare for each company to become profitable.

Beginning with Avalara, the company went public in 2018 and has put up an incredible performance since its debut with a 200% return. The stock’s outperformance vs. its peers is partially due to the South Dakota v. Wayfair ruling in 2018, which saw the Supreme Court rule in favor of South Dakota, which allowed states to require remote sellers to collect and remit sales tax. For businesses operating with minimal issues for years across several state lines, things quickly became confusing as every state has its different thresholds that decide when sales tax must be collected. Worse, some states even have different rules across separate counties or jurisdictions.

This is a massive headache for a business owner trying to focus on sales and keeping its clients happy that now has to have an accountant to ensure everything is done correctly on the tax side. Fortunately, Avalara has fixed this issue with AvaTax, software that automatically calculates sales tax for all your transactions and even pays it for you.

(Click on image to enlarge)

(Source: YCharts.com, Author’s Chart)

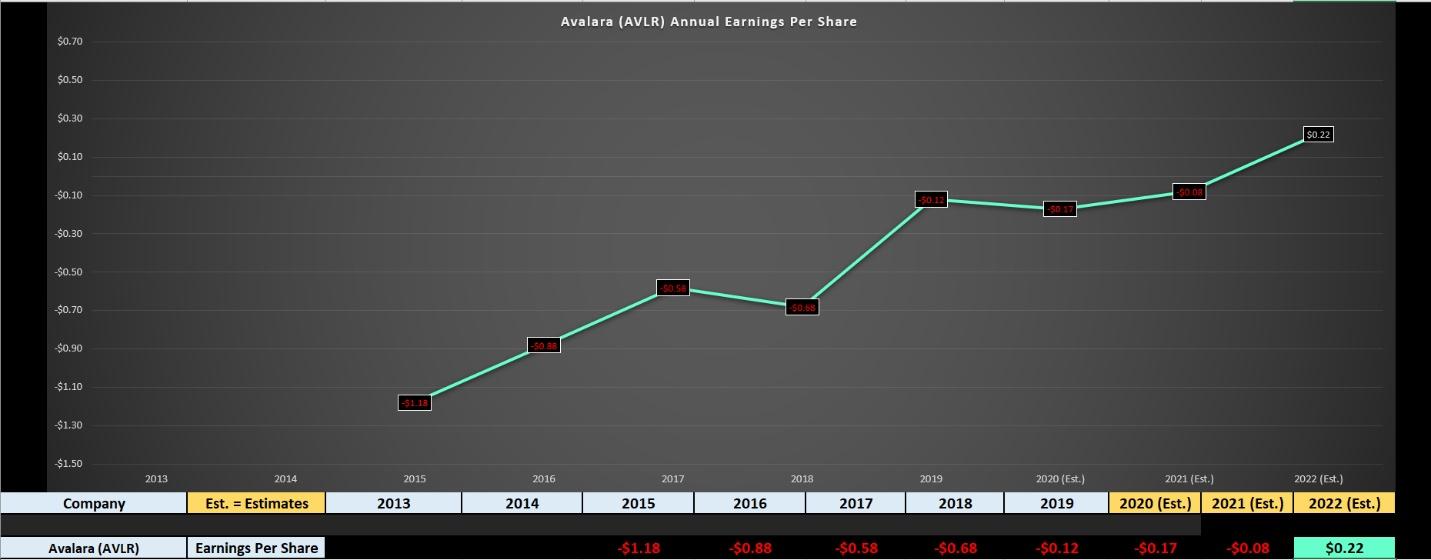

Since its IPO, Avalara’s revenue has surged from $65~ million in Q2 2018 to $117~ million in the most recent quarter, an incredible growth rate of 80% in less than two years. However, the company has continuously posted net losses per share while it makes strategic acquisitions and broadens its offerings, and this has kept some growth funds away.

Fortunately, the company is finally ready to report its first year of positive annual EPS in FY2022, and this could be a catalyst for some growth funds that wait for earnings to begin starting positions in the stock. Given that the stock has barely scratched the surface internationally and has a significant addressable market in Europe, I believe its growth story is still in its early innings.

(Click on image to enlarge)

(Source: TC2000.com)

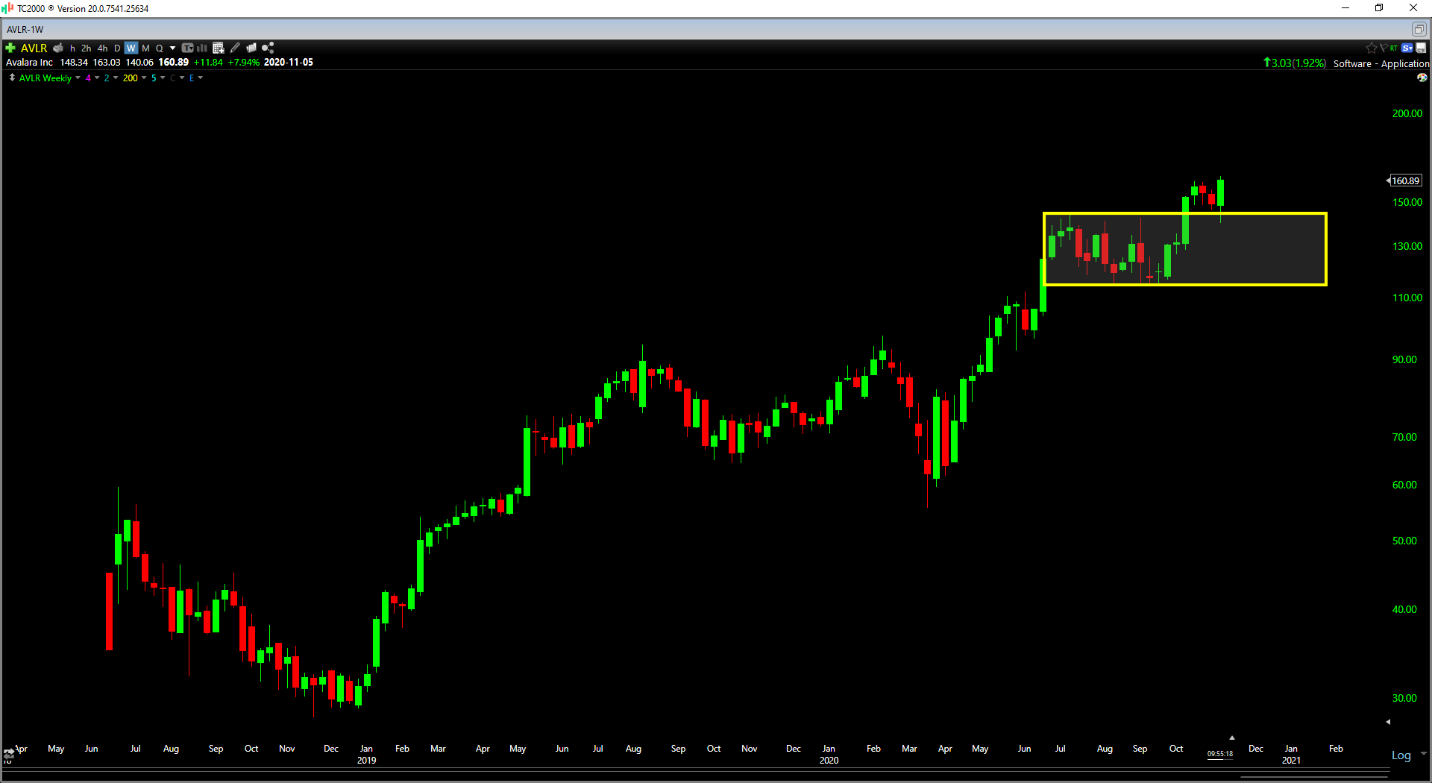

As shown above, Avalara has just broken out of a multi-week base to new highs well ahead of the overall market. This is a great sign that the company is likely to continue being a market leader, and I would expect the stock to find support near $145.00 on any pullbacks. Therefore, for investors looking to start a position, I would watch this area closely if we do see any sharp pullbacks.

(Source: Zillow Company Presentation)

Moving over to Zillow Group, the stock went nowhere from 2014 to 2019 as the market wasn’t crazy about its legacy Internet, Media & Technology real estate business. However, the company has recently revamped itself with a Homes segment and a Mortgages segment and is getting into the massive lending business and home-buying/selling business.

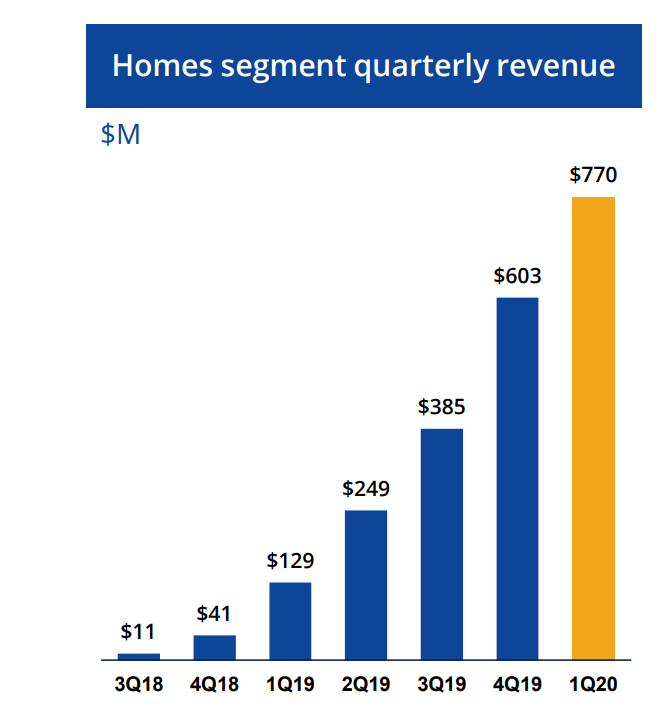

This shift significantly increases the company’s TAM, and thus far, the bold shift has paid off. The company has generated over $2 million in revenue in the past two years alone in its Homes segment, and sales growth has shown no signs of slowing down just yet. In fact, Homes revenue grew from $603 million in Q4 2019 to $770 million in Q1 2020 despite lapping a quarter of 50%+ sequential growth.

(Source: Company Presentation)

While some critics have argued that Zillow’s Homes business has little future as it has similar costs to real-estate agents, these critics forget that most people are looking for convenience. The ability to sell one’s home quickly without any hassle for roughly the same price and similar fees is a massive benefit to those leading busy lifestyles, and the fact that it’s more challenging to show home due to COVID-19 has only become a tailwind to this trend.

Meanwhile, the added social unrest the past two months have also become a further tailwind as some families are not going to sit by and watch riots go on near them if they have young families at home. Therefore, what started as a convenience service has turned into an essential service, and this could continue if we get a contested election and further unrest in some states.

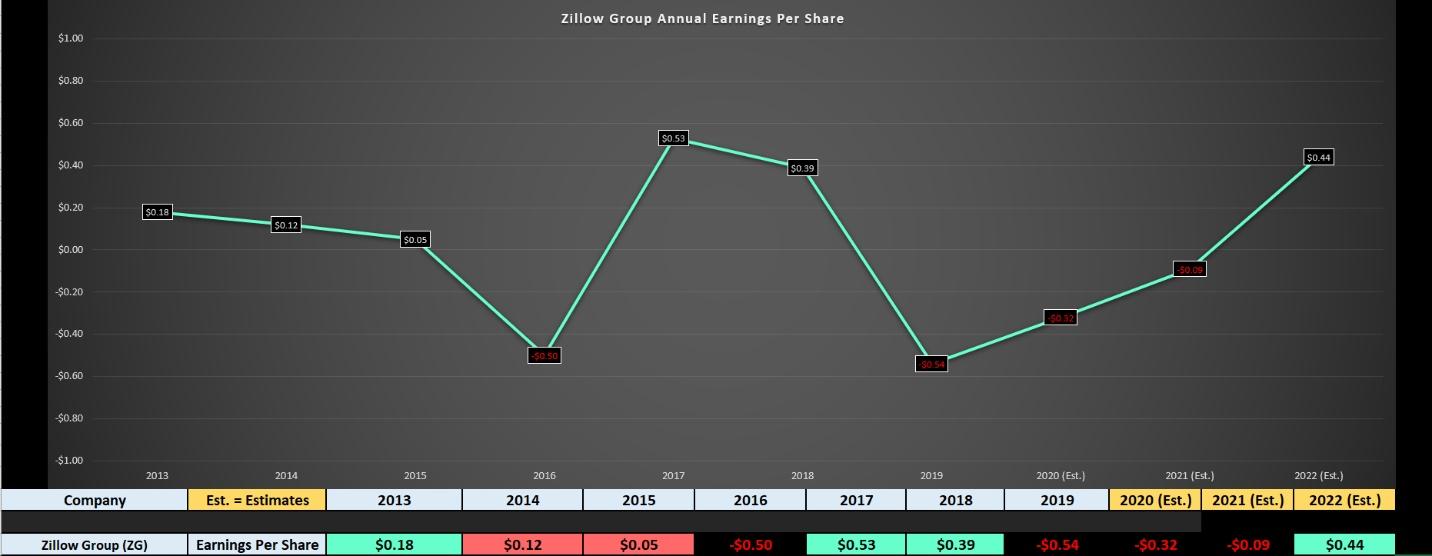

(Click on image to enlarge)

(Source: YCharts.com, Author’s Chart)

If we look at the above chart, it’s clear Zillow doesn’t have a very inspiring earnings trend. However, it’s important to note that the shift to new segments (Homes & Mortgages) put a dent in what was otherwise a profitable business due to significant investments. Fortunately, the company is on a trajectory to report positive annual EPS in FY2022 of $0.44, which is confirmation that this massive pivot in the business is working.

Ultimately, I believe the cutting out of the middle-men in the real estate process could be a massive trend either with or without COVID-19. In fact, I would not be surprised to see annual revenue increase to over $5.5 billion within two years (trailing-twelve-month revenue is $3.5 billion currently).

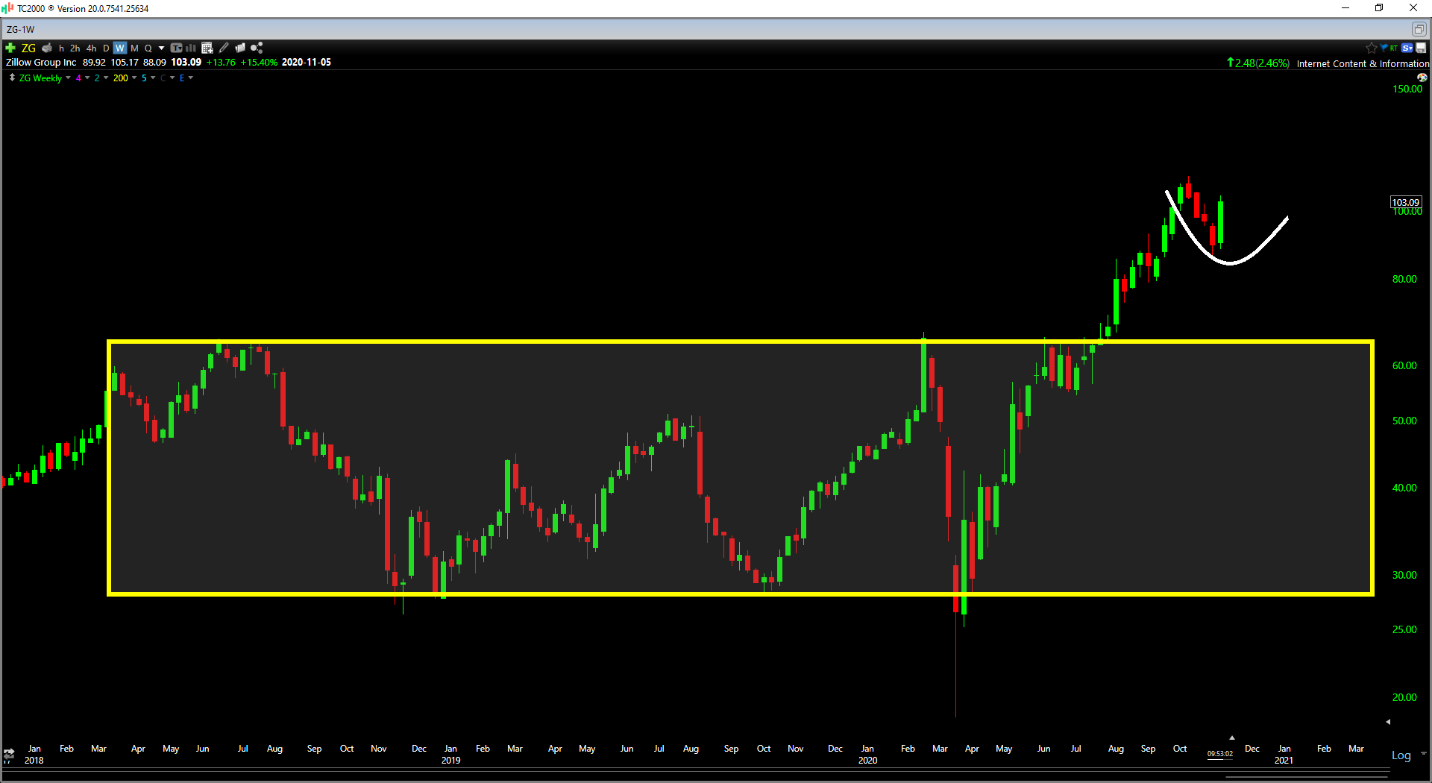

(Click on image to enlarge)

(Source: TC2000.com)

As the chart above shows, the stock is undergoing its first pullback since breaking out of a massive multi-year base, and buyers have stepped in to support the stock near $90.00. While there’s no guarantee that the stock lifts off and heads straight to new highs, I would expect the $88.00 – $90.00 area to be defended on any pullbacks. Therefore, for investors looking for a position in this innovative real-estate trend, this is an area to keep a close eye on.

While we continue to have quite a bit of complacency in the market and the Nasdaq is getting a little overbought short-term, AVLR and ZG are two ways to play the market without worrying as much about what the Nasdaq is doing. This is because these two stocks have defied gravity this year and massively outperformed the Nasdaq, and I would expect them to continue making new highs as more investors catch on to their unique growth stories. In summary, for those looking for a shopping list, if we do see some downside volatility, ZG and AVLR are two names to monitor closely.

ZG shares were trading at $104.54 per share on Thursday afternoon, up to $3.93 (+3.91%). Year-to-date, ZG has gained 128.55%, versus a 10.70% rise in the benchmark S&P 500 index during the same period.

Disclosure: I am long ZG.

Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an ...

more