Image Source: Pexels

Insurance giant Progressive Corporation (PGR - Free Report) and banking leader PNC Financial Services Group (PNC - Free Report) are two top-rated finance stocks to consider after exceeding their Q3 top and bottom line expectations on Tuesday.

Here’s a brief review of their Q3 reports and a look at why now is still a good time to buy Progressive shares which have soared nearly +60% year to date and PNC’s stock which has risen over +20% in 2024.

Image Source: Zacks Investment Research

Progressive’s Q3 Results

Zacks Rank #1 (Strong Buy)

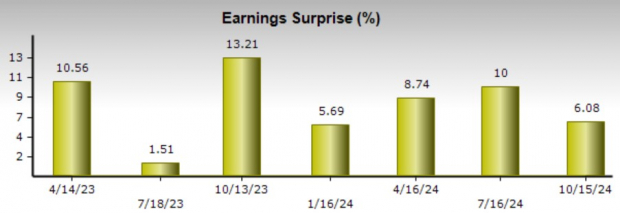

Attributed to a sharp spike in net premiums written, Progressive’s Q3 sales of $19.43 billion beat estimates by 2% and increased 24% from $15.7 billion in the comparative quarter. Capitalizing on its market position and ability to implement higher premium rates, Progressive’s Q3 EPS of $3.58 skyrocketed 71% from $2.09 per share a year ago.

This also beat Q3 EPS estimates of $3.40 by 5% with it noteworthy that Progressive has surpassed the Zacks EPS Consensus for five consecutive quarters posting a very impressive average earnings surprise of 19.85% in its last four quarterly reports.

Image Source: Zacks Investment Research

PNC’s Q3 Results

Zacks Rank #2 (Buy)

Posting Q3 sales of $5.43 billion, PNC's top line expanded 3% year over year and was able to beat estimates of $5.36 billion by 1%. Q3 EPS of $3.49 beat estimates of $3.29 a share by 6%. This was despite PNC’s bottom line contracting from $3.60 per share in the prior-year quarter due to lower customer interest payments and setting aside a larger reserve to cover any unpaid loans.

However, CEO Bill Demchak stated that PNC is well-positioned to capitalize on its market position as well and should achieve record net interest income (NII) in 2025. Plus, PNC has exceeded earnings expectations for seven consecutive quarters posting an average EPS surprise of 7.63% in its last four quarterly reports.

Image Source: Zacks Investment Research

PGR & PNC’s Attractive Valuation (P/E)

Notably, EPS estimates for Progressive and PNC’s fiscal 2024 and FY25 have continued to trend higher over the last 30 days which magnifies their reasonable forward P/E multiples of 19.6X and 14.4X respectively.

Image Source: Zacks Investment Research

Takeaway

After exceeding Q3 expectations, earnings estimate revisions may continue to trend higher for Progressive and PNC in the coming weeks. This could certainly extend the year to date rally in these top finance stocks which remain viable long-term investments, especially at their current levels.

More By This Author:

Top Value Stocks Nearing 52-Week Highs With Stellar Dividends3 Large-Cap Value Funds With Upside To Avoid Present Market Volatility

Bull Of The Day: JD.com

Comments

Log in or sign up to join the conversation.