Social Security Is America’s Pension

Abhorrent income inequality along with issues related to social safety nets like Social Security are political hot potatoes. They should be considered human issues.

I’m certain that most readers regardless of political affiliation have witnessed or experienced firsthand, wage stagnation; people close to retirement who complete comprehensive financial planning realize the positive impact Social Security has on retirement success rates.

Without Social Security included, even those who are excellent savers (I personally witness close to half), may experience financial vulnerability in retirement. Include Social Security or an inflation-adjusted income annuity that lasts a lifetime, and a retiree may depend less on variable assets like stocks to create a dependable, predictable income especially during market cycles characterized by poor sequence of returns risk. In other words, when investment assets do poorly over a series of years (believe it or not this does occur), lifetime income sources can pick up the slack and increase portfolio longevity – there’s less pressure to withdraw from variable assets that may require time to prosper or recover.

The fortunate few who have pensions AND Social Security are able to retire sooner and comfortably compared to their non-pension brethren, regardless of savings habits. According to Willis Towers Watson, only 16% of Fortune 500 companies offer defined benefits plans (pensions) to new hires (2017), compared to 59% in 1998.

According to surveys conducted by the Social Security Administration, roughly half the aged population live in households that receive at least 50% of total family income from Social Security. About a quarter of senior households receive at least 90% of household income from Social Security

The 2018 OASDI Trust fund balance (thanks to www.savvysocialsecurity.com), was $2.95 trillion. Social Security expenses will exceed income beginning in 2020 until 2034. At that time, payroll taxes alone are slated to pay roughly 79% of current benefits.

Depending on costs, birth/death rates, job growth and various other factors, Trust fund projections are just that – educated guesses. At best, we know that based on payroll taxes alone the system is currently cash-flow negative. Yet, I remain confident that both sides of the Congressional aisle will eventually come together to bolster the program. Why? Simple. Social Security has become America’s pension even though it was not designed to be. Without it, we would face mass homelessness. I’m not trying to be bombastic. It’s a pragmatic assessment.

The failure of the program or reduction of Social Security benefits would lead to wholesale poverty. A retirement nest-egg comprised solely of variable assets like stocks and bonds doesn’t cut it for most Americans. There are many reasons why defined contribution plans like 401ks are failures – High costs, the ability to tap accounts for wants like house down payments (ridiculous), investing in the market just to break even most of the time, underfunding. However, I believe the crux of financial vulnerability and root cause for lack of saving and investment is structural wage stagnation.

As I wrote in my book in 2012, employers shall remain forever in recession mode where every day they’ll be thinking about how to replace employees with technology which has been one reason behind poor U.S. productivity numbers. Lance and other contributors to RIA have been writing about how the recent Tax Cuts & Job Act benefits would be directed more toward share buybacks, not employee wages.

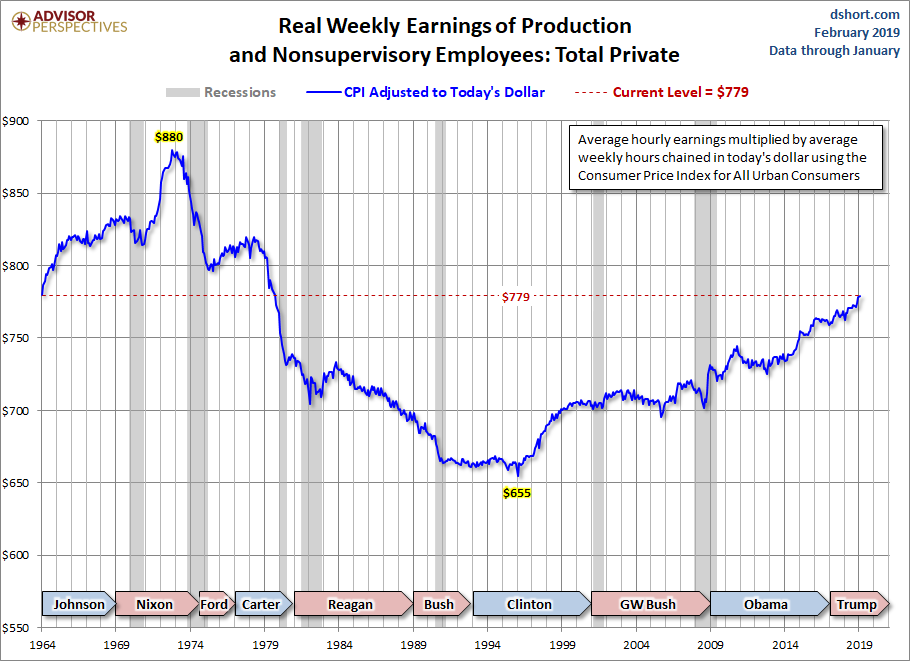

Doug Short does a monumental job (like Lance), analyzing economic data and turning it into visuals that shock and awe. Above, real (adjusted for inflation) weekly earnings of production multiplied by the average work week showcases the latest data point at 8.5% below the 1972 peak. I think this chart outlines best the financial headwind the middle class has faced.

So, as much as I wish we didn’t need Social Security, we do. The program demands reform. Hey, want to fix Social Security? Yes, you as a reader can do it. Want to try your hand at it?

The American Academy of Actuaries created The Social Security Game. I bet your choices in the game can improve the future viability of Social Security. Also, the website provides a wealth of education about practical reform.

The Social Security Expansion Act was initially introduced in 2017 and is now being introduced in the House by Democratic Representative Peter DeFazio of Oregon. This payroll-tax initiative has the potential to extend Social Security solvency to 2073.

Expansion of the Social Security payroll tax cap is on the table. Currently, a Social Security payroll tax of 12.4% (6.2% for employee and employer) is applied to the maximum wage earnings of $132,900 for 2019. The cap on payroll tax leads more of the middle class to pay compared to those with higher wages and investment income. Wages for the top 1% of earners have grown dramatically; as the chart above outlines, wages for the bottom 99% have been stagnant since the early 70s. The proposal is for the payroll tax to apply to wage income above $200,000 for singles and $250,000 for couples. Those with investment income of $200,000 (single), $250,000 (couple) would pay an additional 6.2% in taxes as well.

The Center for Economic and Policy Research in their report “Who Pays if We Modify the Social Security Payroll Tax Cap?” outlines that 1 in 16 people or 6.2% of workers would be affected if the payroll tax were applied to those who earn $250,000 or greater. The majority of workers would not experience a change. Another proposal submitted recently would subject payroll taxes on those who earn more than $400,000 in wages which would only affect to the top 1%. Expanding the taxable earnings base or eliminating the cap altogether would sustain Social Security indefinitely if there are enough current workers in the system to pay the tax.

Individuals frustrated by payroll taxes who believe they can do better on their own are, to be candid, allowing politics not economics drive their mindset. Especially if they believe they may better invest the funds. To place money designed to provide lifetime income into variable risk assets like stocks is not the answer. Also, I have yet to find a private-sector annuity that compares to the payouts and survivor benefits offered by Social Security.

Whether you make $100,000 a year, or a million, you are entitled to receive Social Security benefits. Currently, only half of American workers have access to retirement plans.

Unless corporations are going to return to offering defined benefits plans or pensions to their employees, Social Security will remain am economic necessity for an overwhelming majority of Americans.

The original vision of Social Security was to provide a safety net for workers. It was not designed to be the U.S. pension system. Social Security was to supplement private-sector pension system.

The fault of the over-dependency on a social program lies square on the shoulders of publicly-traded corporations that eliminated pensions to place maximizing shareholder wealth above all else.

Can you imagine a CEO of a publicly-traded company uttering these words today?

“The four parties of any business in order of importance are customers, employees, community and stockholders.”

That was Gen. Robert E. Woods the chief executive of Sears, Roebuck & Company who served as chairman from 1939-1954. He was a former officer in the U.S. Army and a Republican leader of the American Conservatism movement for 40 years.

For those who seek to learn about how American workers have lost leverage and benefits throughout the decades should read Rick Wartzman’s The End of Loyalty and Jonathan Tepper’s recent eye-opener – The Myth of Capitalism.

The RIA Advisor team helps people make smart Social Security and Medicare decisions. Please reach out to us if you need assistance.