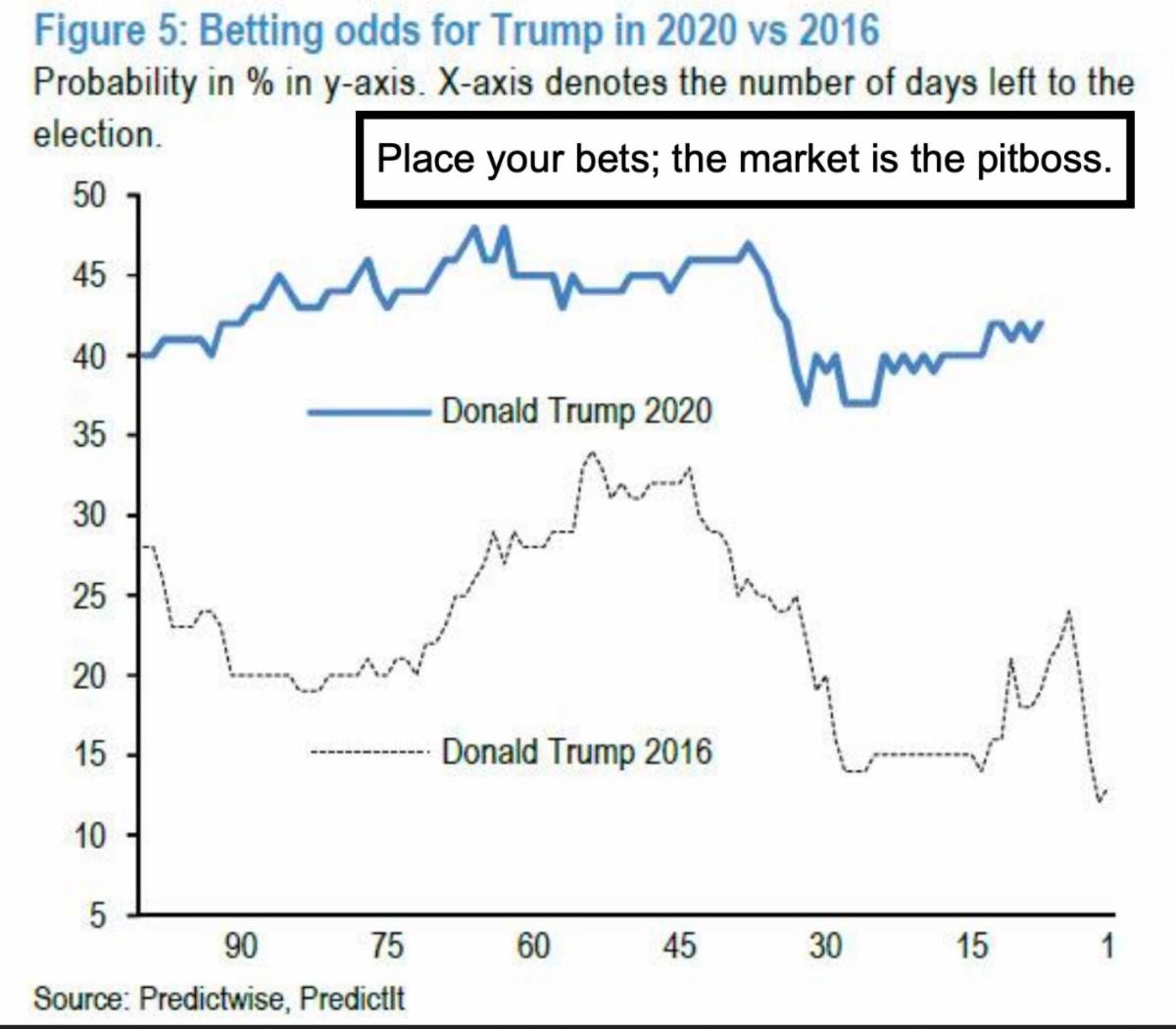

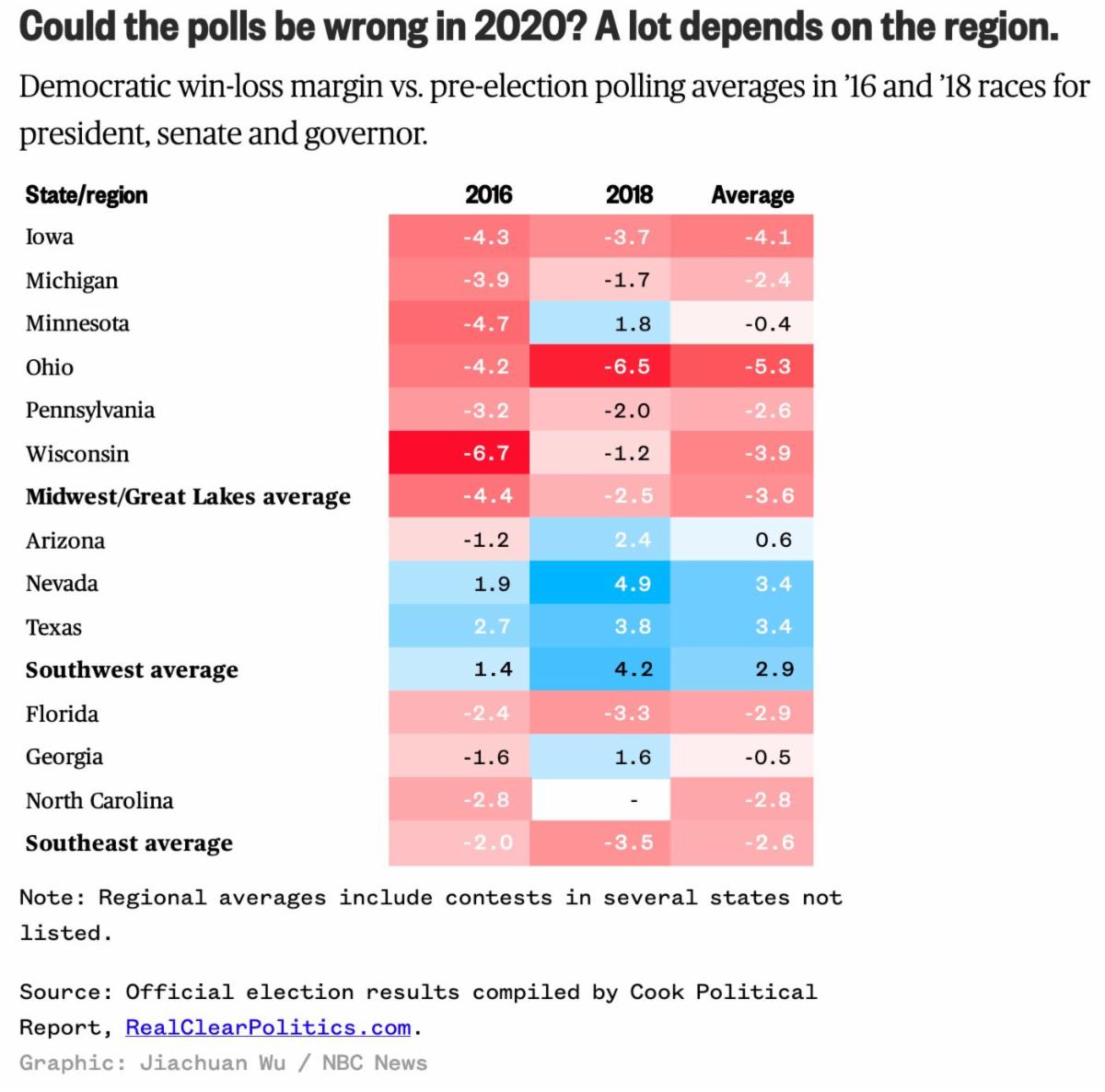

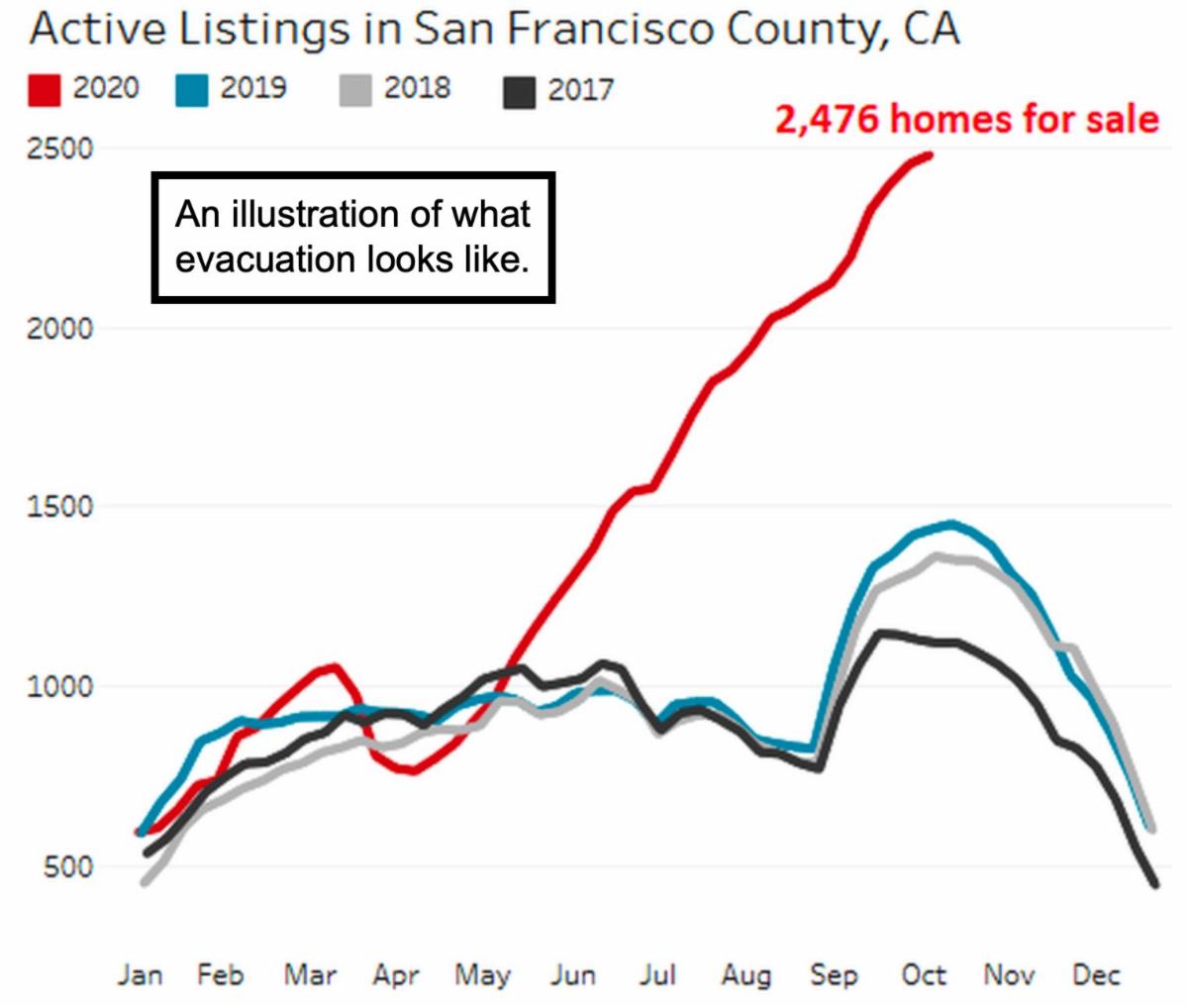

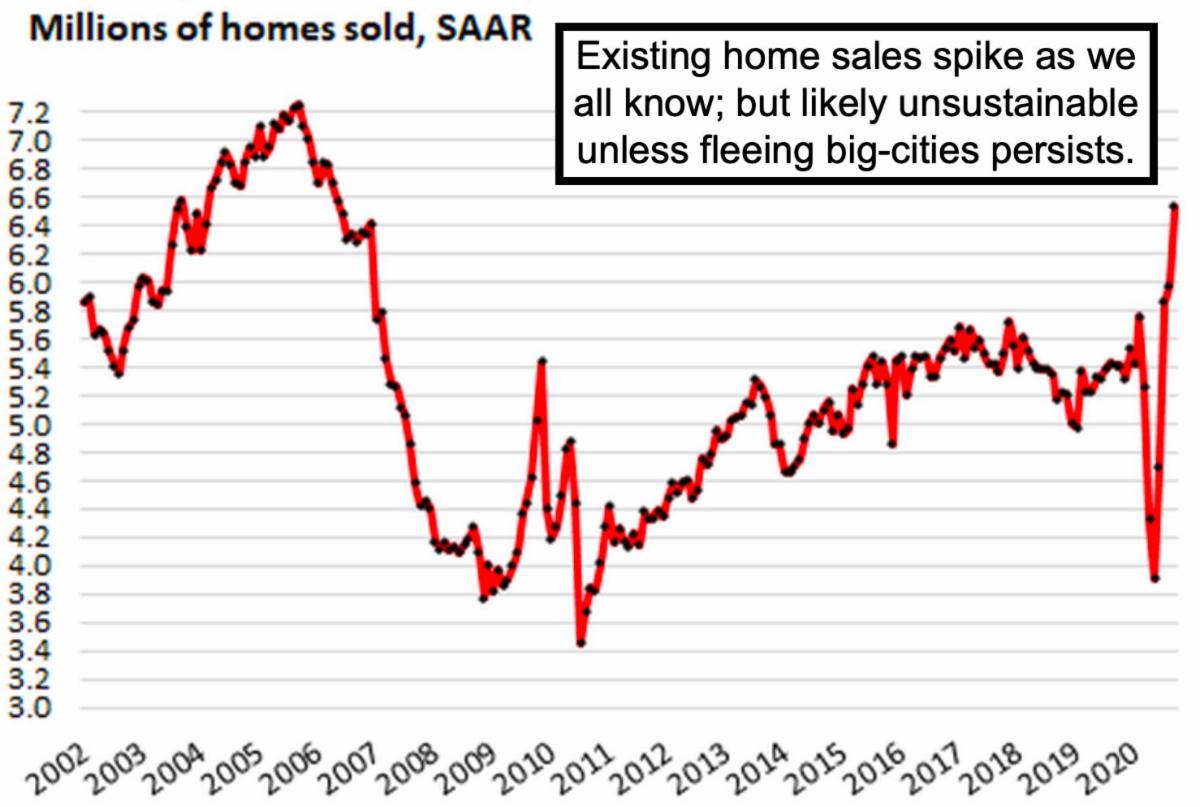

|

Executive summary:

- Little has changed, as S&P efforts at consolidating Monday's heavier hit were uninspiring, hence frustration grew through much of the afternoon.

- It is all part of the same defensive pattern, related to technicals outlined already (the break of S&P's 50-Day, rebound tries, and then likely lower),

- Everyone likely heard about disappointing (or slowly proceeding) COVID vaccines, and in-theory this may bolster the 2nd generation developers, although the 1st generation vaccines have 'some' expected efficacy.

- With patience thin, these delays not only enhance desired therapeutics (as 'if' efficacious, a patient knows within hours or a day or so because it is not a vaccine but a treatment), but they focus upon the COVID 'timeline'.

- With Europe now acknowledging it cannot (even with a proven vaccine) be vaccinated effectively for two years or so, that delays business and of course travel, beyond the range most are anticipating for now.

- In Italy and in France, street violence has occurred because of mandated mask wearing, and perhaps more so by small businesses protesting the new shutdowns, which most simply won't survive financially.

- Aside business, the politics of 'masking' (as inane as they may be) reach across oceans too, with those opposing it 'usually' changing their views if someone close to them sadly contracts the virus.

- The good news is that there is less flu (well masks and no handshakes is a factor), while the bad news is these current waves have not peaked nor will they on November 4, in the U.S. or other countries also impacted.

- As or if we see more restraint on business activity, that contributes more than the tax-selling (political) aspects to a further market shakeout, since it brings into question profitability and continuation of the 'reflation' trade.

- However (and it could be any day) the first vaccine to be approved will be well-received (by markets at least briefly), and I suspect a MAB (that's the monoclonal antibody treatment) even more so if one is found effective).

- Speaking of there is no news on MAB's or anything during today's trade in Sorrento (SRNE), although they filed for a couple new Phase 1 Trials.

- What is eye-opening was after-the-close they withdrew a 'shelf offering' in which funding had come in the form of up to 250 million from a somewhat hidden Caribbean entity that was actually a sketchy Canadian.

- Withdrawing that shelf, means any such dilution ends, perhaps they don't need the money (unclear how it could be already), or something favorable is on-tap almost immediately (we have always lacked confidence in their management, but interested in the varied portfolio of solutions, but if they are maturing and not getting funding in sub-optimal ways, that's good).

- Perhaps they have done something constructive, they have a big litigation that they won, with settlement not required until next year, but that guy (a tycoon who owns the LA Times) resigned from NantKwest yesterday, so that's also possibly a coincidence (this is late-breaking so don't know).

- Coincidence or not, this is where the short-term downtrend intersects with a longer-term uptrend in Sorrento, so an interesting spot to possibly turn the tide higher, based on technicals, if not fundamental progress as yet.

- Chicago has now banned 'indoor dining' and other cities are restricting, as a lot put curfews on too, and that's here and abroad, this likes gets played as a political issue, but actual restrictions seem to be based on not merely high cases, but increasing hospitalizations.

- It's not universal, here in Florida cases (not positivity rates) are higher but there are no new restrictions, perhaps we'll know in 2-3 weeks if that's at all wise, the beat goes on with all this, and yes that's frustrating to us all as well as the stock market's near-term prospects.

- Besides tax concerns one-way or the other, a proven therapeutic within a couple weeks (not months) would be the ticket to arrest defensive market conditions, which otherwise continue to shuffle in a corrective way.

|

|