Is This Juicy 11.6% Yield Going The Wrong Way?

Washington Prime Group (NYSE: WPG) is on a lot of income investors’ radars because of its juicy 11.6% yield.

But can a yield that high – in a real estate investment trust (REIT) that owns malls and shopping centers – be safe?

The company has been around for only three years. It was a spinoff of Simon Property Group (NYSE: SPG) in 2014.

Washington Prime owns properties in 29 states, including the West Ridge Mall in Topeka, Kansas; Arbor Hills in Ann Arbor, Michigan; and The Arboretum in Austin, Texas.

Track Record

Washington Prime’s dividend has been consistent since it spun off from Simon Property. The company pays a quarterly dividend of $0.25 per share, which comes out to $1 annually.

However, because it has been paying a dividend for only three years, we can’t use its track record as an indicator of whether the dividend is reliable. Typically, if a company has paid a consistent dividend for 10 years or longer, I’m more confident that management is serious about sustaining the dividend.

Plenty of Cash Flow

One thing investors can feel good about is that Washington Prime generates plenty of cash flow.

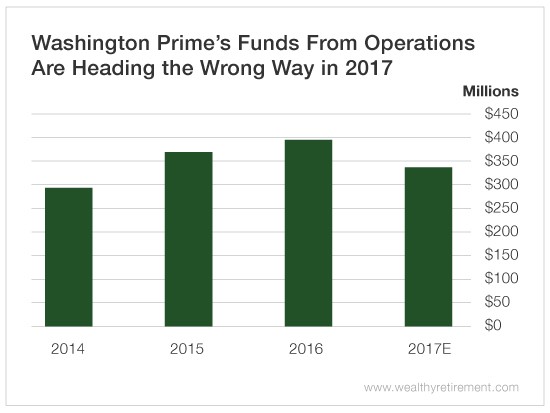

Last year, funds from operations (FFO), a measure of cash flow for REITs, were $398 million. During the year, the company paid $236 million in dividends. So the payout ratio was a very comfortable 59%.

In fact, in all three years of the company’s existence, FFO has been significantly greater than dividends paid.

This year, that’s expected to be the case again – although with a wrinkle. FFO is forecast to decline this year to $336 million.

Again, that’s more than enough to cover the expected $236 million in dividends, but we do not like to see cash flow or FFO declining. It’s something to keep an eye on, especially in the struggling retail space.

As of June 20 of this year, roughly 5,300 retail stores have closed. If closings continue at the same pace for the rest of the year, more stores will shutter in 2017 than those that closed during the Great Recession.

If FFO is not expected to decline again in 2018, the stock will likely get an upgrade.

For now, the short track record and declining cash flow, combined with a dividend that is easily covered by cash flow, make the stock only a moderate risk for a dividend cut in the next 12 months.

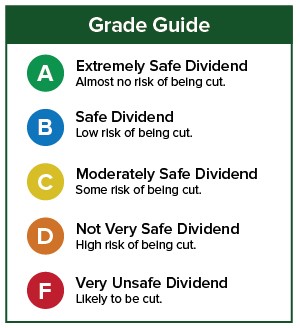

Dividend Safety Rating: C

Disclaimer: Nothing published by Wealthy Retirement should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not ...

more