Best Stocks Below Their Graham Number – August 2017

One popular approach to investing based on Benjamin Graham’s methods is to use the so-called “Graham Number.” There are some important differences between the Graham Number and the Graham Formula, but using the Graham Number is definitely useful even if the investor only uses it as a screening tactic.

I’ve selected the best companies reviewed by ModernGraham which trade below their Graham Number. The companies selected all are found suitable for the Defensive Investor and/or the Enterprising Investor, and have been valued as undervalued based on the ModernGraham valuation model. Further, the overall screen found 36 companies meeting these criteria (out of the 897+ companies covered by ModernGraham), and the full list can be found near the end of this article; however, to cut down on the length of the post, I’ve selected the ten which trade furthest below their Graham Number.

Defensive Investors are defined as investors who are not able or willing to do substantial research into individual investments, and therefore need to select only the companies that present the least amount of risk. Enterprising Investors, on the other hand, are able to do substantial research and can select companies that present a moderate (though still low) amount of risk. Each company suitable for the Defensive Investor is also suitable for Enterprising Investors.

These companies have demonstrated strong financial positions through passing the rigorous requirements of the ModernGraham Investor and show potential for capital growth based on their current price in relation to intrinsic value. As such, these graham number stocks may be a great investment if they prove to be suitable for your portfolio after your own additional research.

Capital One Financial Corp. (COF)

Capital One Financial Corp. is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability over the last ten years. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $5.15 in 2012 to an estimated $7.13 for 2016. This level of demonstrated earnings growth outpaces the market’s implied estimate of 0.05% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on Benjamin Graham’s formula, returns an estimate of intrinsic value above the price. (See the full valuation)

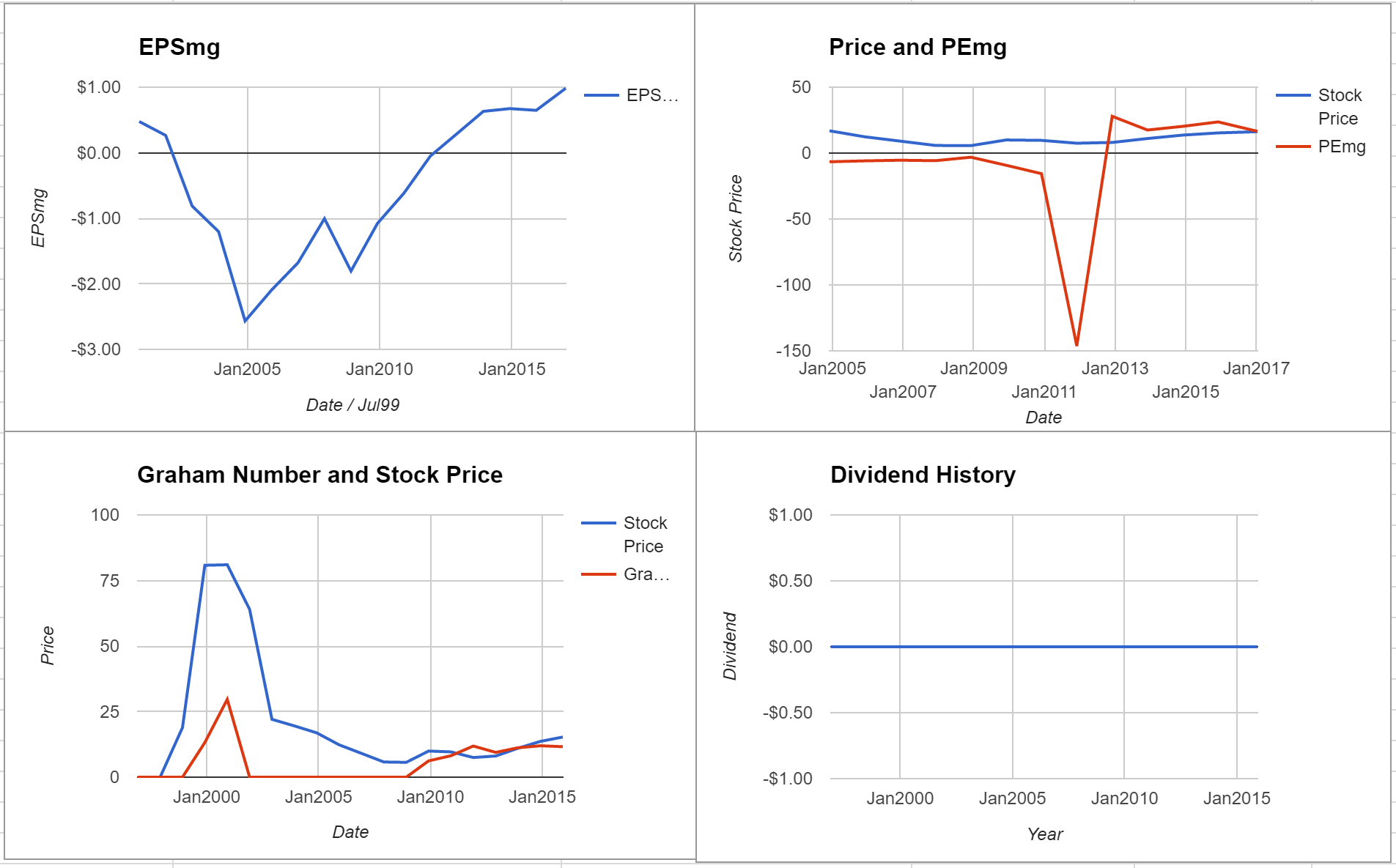

Celestica Inc (CLS)

Celestica Inc is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the small size, low current ratio, insufficient earnings stability or growth over the last ten years, and the poor dividend history. The Enterprising Investor is only concerned with the lack of dividends. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $0.29 in 2012 to an estimated $0.98 for 2016. This level of demonstrated earnings growth outpaces the market’s implied estimate of 4% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value above the price.

At the time of valuation, further research into Celestica Inc revealed the company was trading below its Graham Number of $20.71. The company does not pay a dividend. Its PEmg (price over earnings per share – ModernGraham) was 16.51, which was below the industry average of 28.12, which by some methods of valuation makes it one of the most undervalued stocks in its industry. Finally, the company was trading above its Net Current Asset Value (NCAV) of $6.81. (See the full valuation)

Foot Locker, Inc. (FL)

Foot Locker, Inc. is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability over the last ten years, and the high PB ratio. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $2.16 in 2014 to an estimated $4.47 for 2018. This level of demonstrated earnings growth outpaces the market’s implied estimate of 4.23% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value above the price.

At the time of valuation, further research into Foot Locker, Inc. revealed the company was trading above its Graham Number of $48.72. The company pays a dividend of $1.1 per share, for a yield of 1.5% Its PEmg (price over earnings per share – ModernGraham) was 16.96, which was below the industry average of 50.09, which by some methods of valuation makes it one of the most undervalued stocks in its industry. Finally, the company was trading above its Net Current Asset Value (NCAV) of $11.28. (See the full valuation)

Kelly Services, Inc. (KELYA)

Kelly Services, Inc. is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the small size, low current ratio, insufficient earnings stability or growth over the last ten years, and the poor dividend history. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $1.1 in 2013 to an estimated $1.8 for 2017. This level of demonstrated earnings growth outpaces the market’s implied estimate of 1.74% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value above the price.

At the time of valuation, further research into Kelly Services, Inc. revealed the company was trading below its Graham Number of $30.13. The company pays a dividend of $0.28 per share, for a yield of 1.3% Its PEmg (price over earnings per share – ModernGraham) was 11.99, which was below the industry average of 21.9, which by some methods of valuation makes it one of the most undervalued stocks in its industry. Finally, the company was trading above its Net Current Asset Value (NCAV) of $5.19. (See the full valuation)

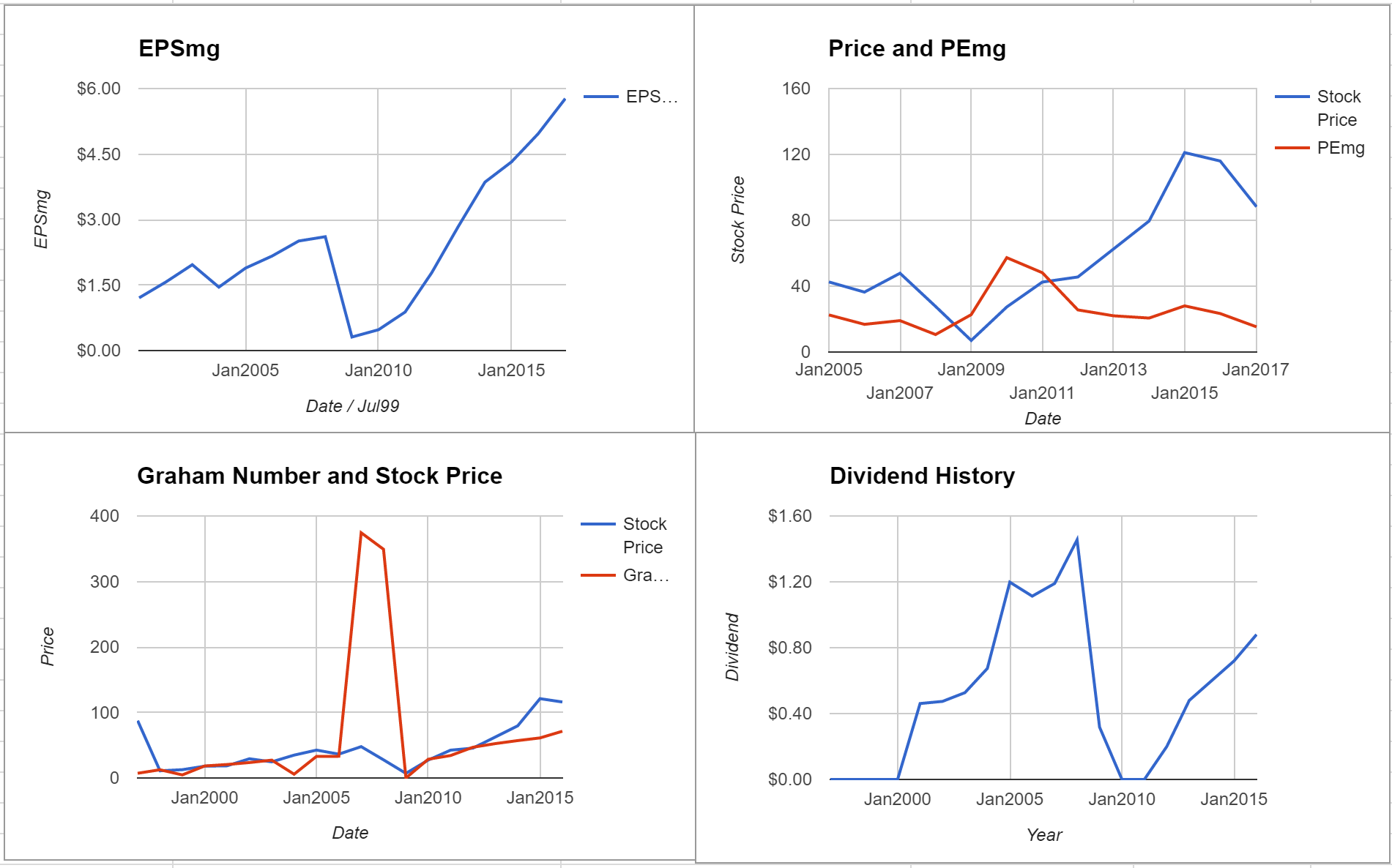

Signet Jewelers Ltd. (SIG)

Signet Jewelers Ltd. is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability or growth over the last ten years, and the poor dividend history. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $2.84 in 2013 to an estimated $5.77 for 2017. This level of demonstrated earnings growth outpaces the market’s implied estimate of 3.39% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value above the price.

At the time of valuation, further research into Signet Jewelers Ltd. revealed the company was trading above its Graham Number of $71.41. The company pays a dividend of $1 per share, for a yield of 1.1% Its PEmg (price over earnings per share – ModernGraham) was 15.29, which was below the industry average of 26.36, which by some methods of valuation makes it one of the most undervalued stocks in its industry. Finally, the company was trading above its Net Current Asset Value (NCAV) of $4.06. (See the full valuation)

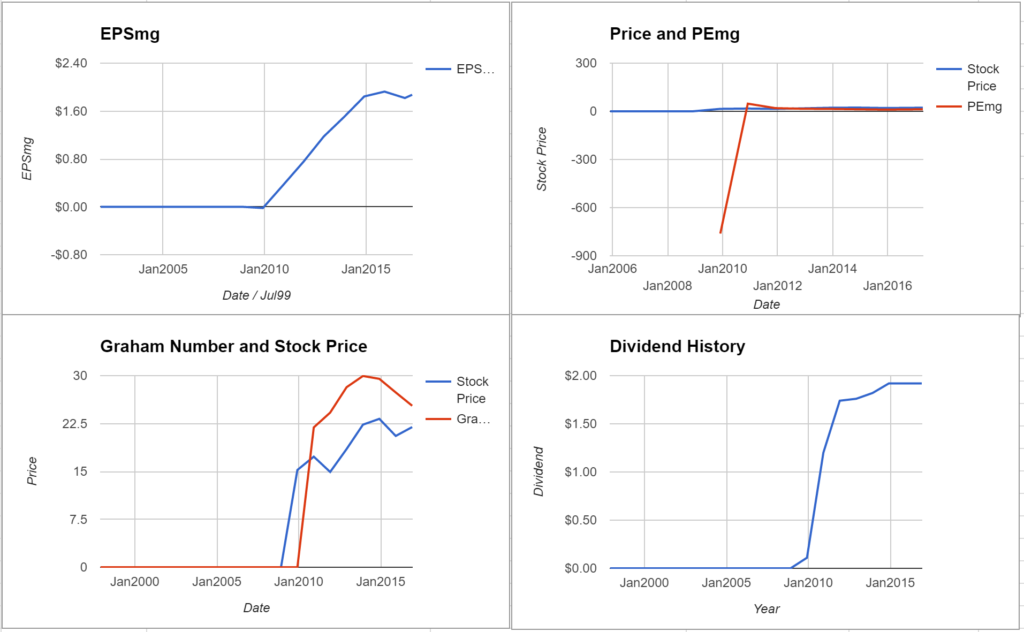

Starwood Property Trust, Inc. (STWD)

Starwood Property Trust, Inc. is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability over the last ten years, and the poor dividend history. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Fairly Valued after growing its EPSmg (normalized earnings) from $1.5 in 2013 to an estimated $1.87 for 2017. This level of demonstrated earnings growth supports the market’s implied estimate of 1.84% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on Benjamin Graham’s formula, returns an estimate of intrinsic value within a margin of safety relative to the price.

At the time of valuation, further research into Starwood Property Trust, Inc. revealed the company was trading below its Graham Number of $29.28. The company pays a dividend of $1.92 per share, for a yield of 8.4%, putting it among the best dividend paying stocks today. Its PEmg (price over earnings per share – ModernGraham) was 12.17, which was below the industry average of 51.63, which by some methods of valuation makes it one of the most undervalued stocks in its industry. (See the full valuation)

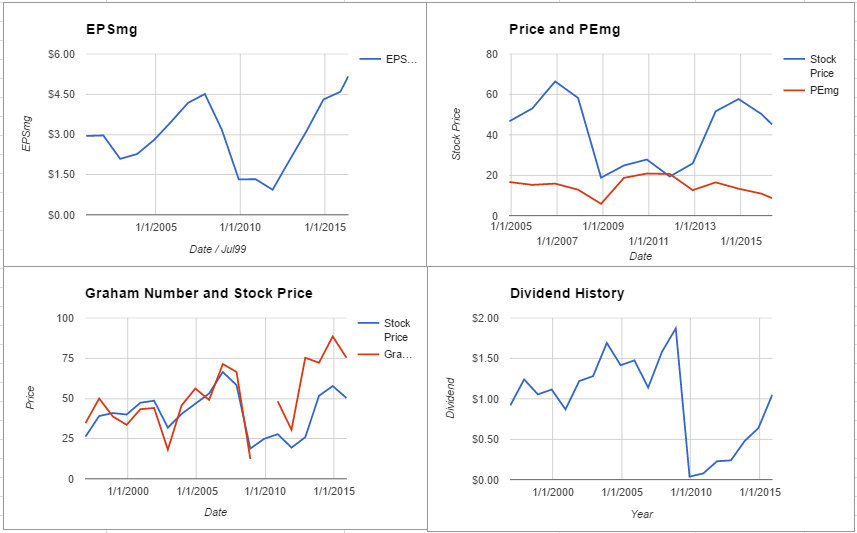

Lincoln National Corporation (LNC)

Lincoln National Corporation is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability over the last ten years. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $2.04 in 2012 to an estimated $5.16 for 2016. This level of demonstrated earnings growth outpaces the market’s implied estimate of 0.12% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on Benjamin Graham’s formula, returns an estimate of intrinsic value above the price. (See the full valuation)

Canadian Western Bank (CBWBF)

Canadian Western Bank qualifies for both the Defensive Investor and the Enterprising Investor. In fact, the company meets all of the requirements of both investor types, a rare accomplishment indicative of the company’s strong financial position. The Enterprising Investor has no initial concerns. As a result, all value investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $2.14 in 2013 to an estimated $2.69 for 2017. This level of demonstrated earnings growth outpaces the market’s implied estimate of 1.1% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on Benjamin Graham’s formula, returns an estimate of intrinsic value above the price.

At the time of valuation, further research into Canadian Western Bank revealed the company was trading below its Graham Number of $36.05. The company pays a dividend of $0.92 per share, for a yield of 3.2%, putting it among the best dividend paying stocks today. Its PEmg (price over earnings per share – ModernGraham) was 10.7, which was below the industry average of 21.43, which by some methods of valuation makes it one of the most undervalued stocks in its industry. (See the full valuation)

Citigroup Inc (C)

Citigroup Inc is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the insufficient earnings stability or growth over the last ten years, and the poor dividend history. The Enterprising Investor has no initial concerns. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $-2.31 in 2012 to an estimated $4.1 for 2016. This level of demonstrated earnings growth outpaces the market’s implied estimate of 1.16% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on Benjamin Graham’s formula, returns an estimate of intrinsic value above the price. (See the full valuation)

Linamar Corporation (LNR)

Linamar Corporation is suitable for the Enterprising Investor but not the more conservative Defensive Investor. The Defensive Investor is concerned with the low current ratio, insufficient earnings stability over the last ten years. The Enterprising Investor is only concerned with the level of debt relative to the net current assets. As a result, all Enterprising Investors following the ModernGraham approach should feel comfortable proceeding with the analysis.

As for a valuation, the company appears to be Undervalued after growing its EPSmg (normalized earnings) from $2.22 in 2013 to an estimated $6.93 for 2017. This level of demonstrated earnings growth outpaces the market’s implied estimate of 0.1% annual earnings growth over the next 7-10 years. As a result, the ModernGraham valuation model, based on the Benjamin Graham value investing formula, returns an estimate of intrinsic value above the price.

At the time of valuation, further research into Linamar Corporation revealed the company was trading below its Graham Number of $83.15. The company pays a dividend of $0.4 per share, for a yield of 0.7% Its PEmg (price over earnings per share – ModernGraham) was 8.7, which was below the industry average of 18.47, which by some methods of valuation makes it one of the most undervalued stocks in its industry. Finally, the company was trading above its Net Current Asset Value (NCAV) of $-7.49. (See the full valuation)

The Full List

To view the MG Value and PEmg information, you must be logged in as a premium member. Clicking on the company name will take you to the company’s latest valuation.

For the investor type, a “D” indicates the company is suitable for the Defensive Investor, an “E” indicates the company is suitable for the Enterprising Investor, and an “S” indicates the company is considered speculative at this time.

| Ticker | Name with Link | Investor Type | Latest Valuation Date | MG Value | Recent Price | Price as a percent of Value | PEmg Ratio | Div. Yield | Graham Number |

| AFL | AFLAC Incorporated | D | 12/19/2016 | — | $79.84 | — | — | 2.05% | $87.98 |

| AHL | Aspen Insurance Holdings Limited | E | 12/13/2016 | — | $46.75 | — | — | 1.84% | $82.44 |

| ARW | Arrow Electronics, Inc. | E | 7/3/2016 | — | $74.23 | — | — | 0.00% | $81.27 |

| ASH | Ashland Global Holdings Inc. | E | 7/27/2016 | — | $60.98 | — | — | 2.56% | $73.88 |

| BAC | Bank of America Corp | E | 7/14/2016 | — | $23.62 | — | — | 0.85% | $23.92 |

| BBBY | Bed Bath & Beyond Inc. | D | 6/14/2016 | — | $27.27 | — | — | 0.00% | $41.96 |

| C | Citigroup Inc | E | 7/19/2016 | — | $66.58 | — | — | 0.30% | $85.07 |

| CNO | CNO Financial Group Inc | E | 1/28/2017 | — | $22.31 | — | — | 1.34% | $24.73 |

| COF | Capital One Financial Corp. | E | 7/6/2016 | — | $81.53 | — | — | 1.96% | $122.14 |

| CVG | Convergys Corp | E | 3/18/2017 | — | $22.92 | — | — | 1.53% | $23.70 |

| DFS | Discover Financial Services | D | 1/28/2017 | — | $59.43 | — | — | 1.95% | $62.08 |

| FL | Foot Locker, Inc. | E | 3/6/2017 | — | $34.38 | — | — | 3.20% | $48.72 |

| KBH | KB Home | E | 2/4/2017 | — | $22.21 | — | — | 0.45% | $25.21 |

| KELYA | Kelly Services, Inc. | E | 2/7/2017 | — | $21.37 | — | — | 1.31% | $30.13 |

| LNC | Lincoln National Corporation | E | 5/20/2016 | — | $68.02 | — | — | 1.62% | $89.07 |

| MET | Metlife Inc | E | 12/13/2016 | — | $47.02 | — | — | 3.30% | $78.35 |

| NAVI | Navient Corp | E | 8/31/2016 | — | $13.60 | — | — | 4.71% | $21.98 |

| PBCT | People’s United Financial, Inc. | D | 6/20/2016 | — | $16.63 | — | — | 4.03% | $17.28 |

| RF | Regions Financial Corp | E | 6/27/2016 | — | $14.06 | — | — | 1.71% | $14.93 |

| SANM | Sanmina Corp | E | 12/5/2016 | — | $35.20 | — | — | 0.00% | $36.05 |

| SENEA | Seneca Foods Corp | E | 12/22/2016 | — | $28.90 | — | — | 0.00% | $69.20 |

| SIG | Signet Jewelers Ltd. | E | 1/9/2017 | — | $53.59 | — | — | 1.87% | $71.41 |

| SPOK | Spok Holdings, Inc. | E | 2/9/2017 | — | $16.25 | — | — | 3.08% | $38.13 |

| STI | SunTrust Banks, Inc. | E | 4/11/2017 | — | $56.13 | — | — | 1.78% | $61.96 |

| STWD | Starwood Property Trust, Inc. | E | 4/11/2017 | — | $22.08 | — | — | 8.70% | $29.28 |

| SUP | Superior Industries International Inc | E | 3/7/2017 | — | $14.35 | — | — | 5.02% | $25.53 |

| SYF | Synchrony Financial | E | 3/2/2017 | — | $30.07 | — | — | 0.86% | $34.07 |

| SYKE | Sykes Enterprises, Incorporated | E | 3/20/2017 | — | $26.14 | — | — | 0.00% | $27.43 |

| TCF | TCF Financial Corporation | E | 3/26/2017 | — | $14.93 | — | — | 2.01% | $18.02 |

| TRV | Travelers Companies Inc | D | 12/1/2016 | — | $127.89 | — | — | 1.52% | $134.38 |

| TSE:CLS | Celestica Inc | E | 1/11/2017 | — | $14.38 | — | — | 0.00% | $20.71 |

| TSE:CM | Canadian Imperial Bank of Commerce | E | 1/12/2017 | — | $106.94 | — | — | 4.44% | $114.08 |

| TSE:CWB | Canadian Western Bank | D | 3/25/2017 | — | $28.00 | — | — | 3.29% | $36.05 |

| TSE:LNR | Linamar Corporation | E | 3/26/2017 | — | $67.67 | — | — | 0.59% | $83.15 |

| TSE:TD | Toronto-Dominion Bank | D | 4/11/2017 | — | $63.73 | — | — | 3.45% | $65.31 |

| URBN | Urban Outfitters, Inc. | D | 7/19/2016 | — | $19.27 | — | — | 0.00% | $20.09 |

Disclaimer:

The author held a long position in Starwood Property Trust (STWD) but did not hold a position in any other company mentioned in this article at the time of ...

more