Image Source: Unsplash

In our recent two-part series on the yield curve (Part One Part Two) we discussed the four predominant yield curve shifts and what they imply about economic activity and monetary policy. Additionally, given the current bullish steepening trend of the yield curve, we provided data on how prior bull steepening environments impacted various stock indexes, sectors, and factors. Missing from our analysis was a discussion of a specific type of REIT whose valuations are well correlated with the shape of the yield curve. If you are buying this bull steepener, agency REITs are worth your consideration.

What is an Agency Mortgage REIT?

REITs own, manage, or hold the debt on income-producing properties. REITs must pay out at least 90% of their taxable profits to shareholders annually. This unique legal structure makes investment analysis of REITs different than most companies. REIT investors must analyze how changing economic, financial market, and monetary policy conditions affect the interplay between their underlying assets and liabilities.

Within the REIT category are a subclass investors call agency REITs. These companies own mortgages on residential real estate. Furthermore, as connotated by the word “agency,” most of the mortgages are secured and guaranteed against default by government agencies such as Fannie Mae, Freddie Mac, and Ginnie Mae. These securities are called Mortgage-Backed Securities (MBS). Because the U.S. government owns the agencies, MBS is essentially free of credit risk.

How Agency REITs Make Money

Agency REIT earnings primarily come from three sources: the spread between the assets and liabilities (mortgage yield and debt), hedging costs, and the amount of leverage employed.

Hypothetically, let’s start a new agency REIT to help you appreciate how they operate.

- We solicit $1 billion from equity investors.

- A significant portion of the $1 billion is used to buy mortgage-backed securities (MBS).

- We then borrow $4 billion from a bank using the $1 billion of MBS as collateral.

- The proceeds from the $4 billion loan also purchase MBS.

- Our new REIT has about $5 billion of MBS against $1 billion of equity and $4 billion of debt.

- As a result, the REIT has 5x leverage.

Assuming our mortgages pay 6% and our debt costs 4%, we can make $140 million a year, equating to a 14% return for our equity holders. That handily surpasses the 6% return if leverage wasn’t employed.

The math is relatively simple. On the $1 billion of MBS funded with equity, the REIT will make 6% or $60 million. On the $4 billion of MBS funded with debt, the REIT will earn the 2% difference between the MBS and the debt, or $80 million. The total earnings of $140 million divided by the $1 billion equity stake equals 14%.

Unfortunately, managing an agency REIT is not nearly as simple as we illustrate.

The Complexities Of Agency REIT Portfolio Management

MBS are a unique type of bond. The mortgagors, homeowners, can partially or fully pay down their mortgages whenever they want. As a result of the unique prepay option, the duration of MBS varies significantly with mortgage rates. At the same time, the duration of a REIT’s liabilities are much more stable. Accordingly, the portfolio managers take on duration mismatch risk.

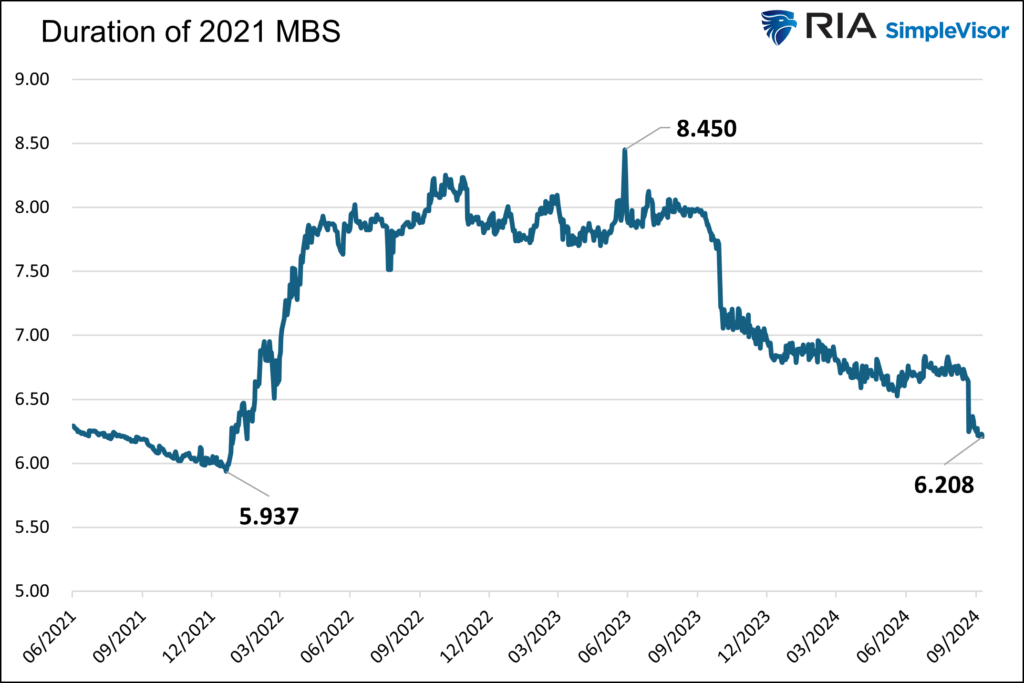

The following chart shows the duration of a Fannie Mae MBS originated in 2021. The weighted average mortgage rates of the underlying loans in the MBS are 3.36%. When rates started rising rapidly in 2022, the mortgagors had no incentive to prepay their loans. As a result, the duration of this MBS rose by 2.50 years. Since then, the duration has fallen with mortgage rates, as the odds of prepayments have increased. A duration change of 2.50 years may not seem like a lot, but when leverage is used, such a change can result in a relatively large duration mismatch and significant gains or losses.

(Click on image to enlarge)

Because the duration of our MBS varies and our liabilities are relatively constant, agency REITs are constantly hedging duration risk. Furthermore, the yield spread between MBS and Treasuries introduces spread risk. The more a REIT hedges to minimize potential duration mismatches or spread risk, the less risk they take. But the hedging costs eat into profits. Lesser hedging can produce more profits but poses more significant risks.

A Steeper Yield Curve Should Help REITs

Like banks, most agency REITs borrow for shorter terms than the duration of their assets. Creating such a mismatch in a positively sloped yield curve can result in additional profits as borrowing costs are less than asset yields.

If the bull steepener yield curve trend continues, agency REIT MBS should gain value. However, the duration of the MBS will shrink due to prepayments. New MBS replacements will have lower yields. However, funding costs should decline. There are many moving parts to consider. While the environment is conducive for profits, as we noted earlier, the performance of agency REITs comes down to hedging accumen.

Several agency REITs are worth exploring, but for demonstration purposes, we focus on the oldest and largest public agency REIT, Annaly Capital Management (NLY). (Disclosure: RIA Advisors has a position in NLY in its client portfolios.)

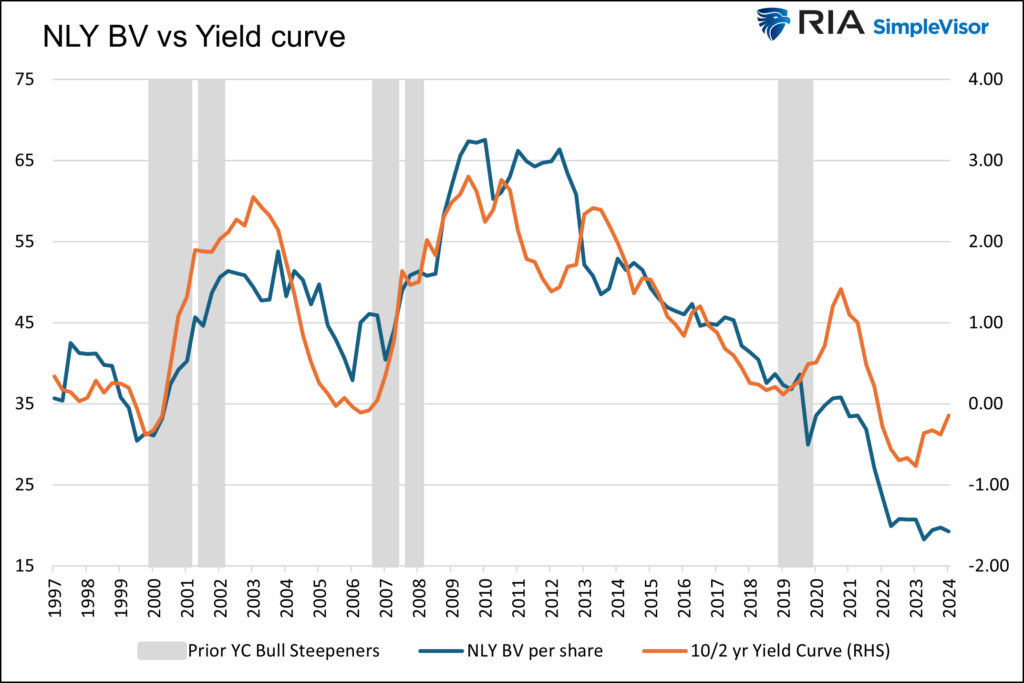

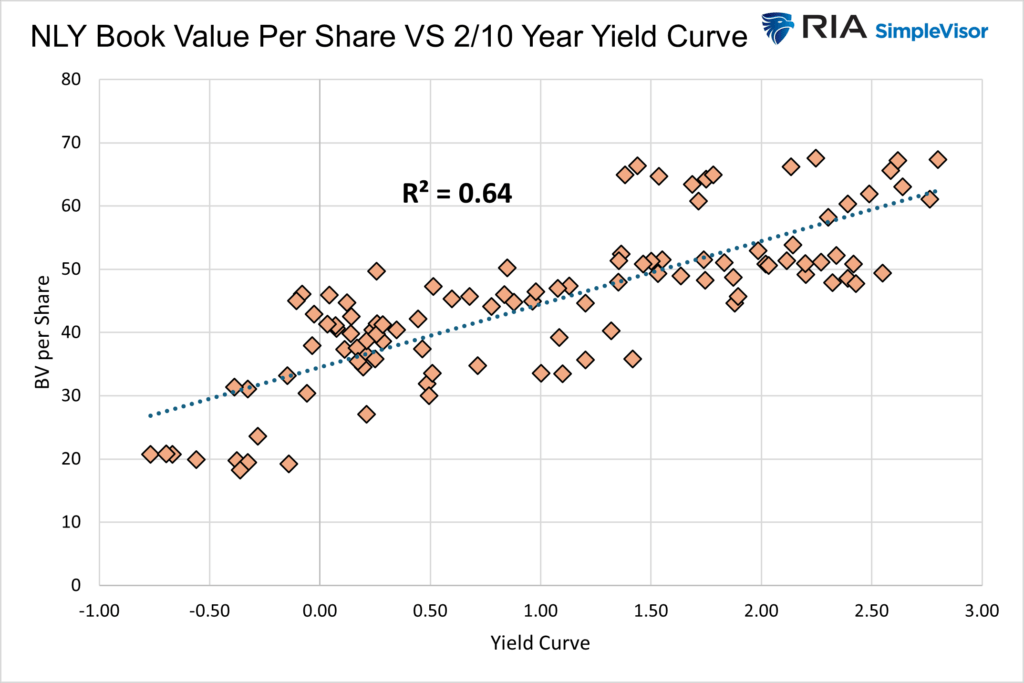

The graph below compares NLY’s book value per share with the 10/2-year yield curve. The gray bars highlight the last five persistent bull steepener periods. Its book value and the yield curve track each other closely. The high correlation is shown in the second graph.

(Click on image to enlarge)

NLY’s BV per share has risen during bull steepeners, except for 2020.

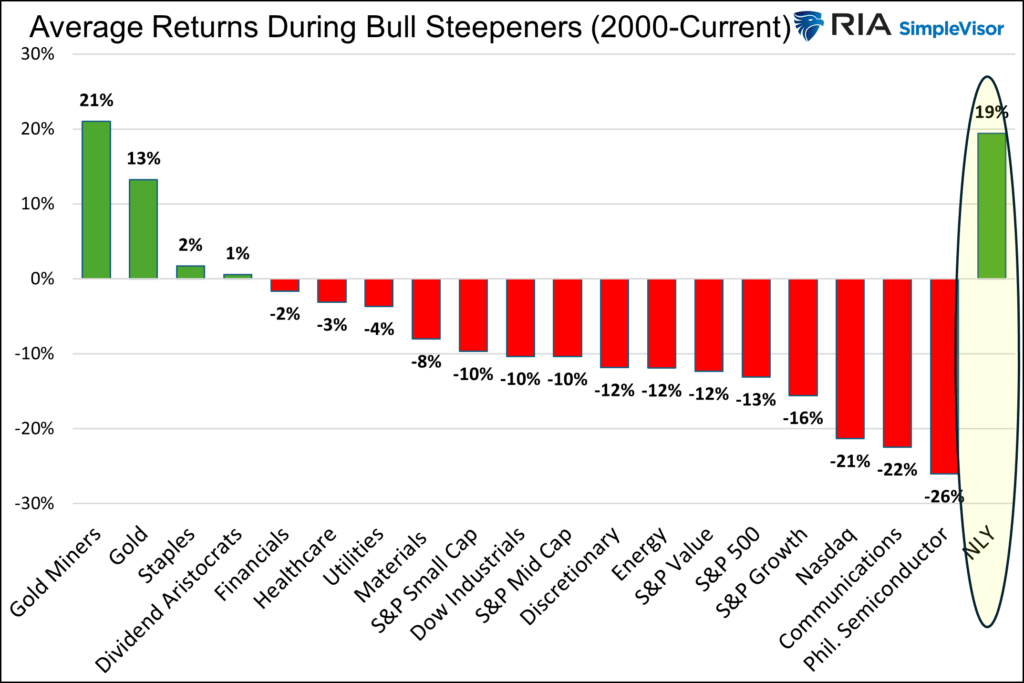

NLY has averaged a 19% return during the five latest bull steepeners. That beats every other equity asset in the graph below, except for gold miners.

(Click on image to enlarge)

No Guarantees

While NLY has done well during bull steepeners on average, it did lose 30% during the pandemic. As such, we shouldn’t take the yield curve environment for granted. However, the rare nature of the pandemic resulted in hedging difficulties due to volatile bond markets and irregular mortgagor behaviors. A repeat of similar conditions is unlikely.

Investors should be aware of market valuations in addition to the fundamental valuation of REIT portfolios. The other reason for NLY’s steep decline in 2020 was fearful equity investors. As shown below, courtesy of Zacks, NLY’s price-to-book value fell from nearly 1.00 before the pandemic to 0.68 at the end of March 2020. Investors were fearful and discounted the stock by over 30% from its book value.

There are additional risks as follows:

- The current bull steepener ends as bond yields increase and the yield curve re-inverts. In such a scenario, book value would likely fall.

- Leverage is easy to maintain when markets are liquid; however, in 2008, REITs were forced to sell assets and reduce leverage, negatively affecting earnings and dividends.

- Management does not adequately hedge the portfolio.

Summary

Despite double-digit dividend yields in many cases and the cushion such high dividends provide, buying agency REITs is not a guaranteed home run in a bull steepener. That said, these firms offer investors a way to benefit from a steepening yield curve while avoiding an earnings slowdown that may hamper many stocks in an economic downturn.

More By This Author:

Government Dysfunction Is Back On The Calendar

Trump Or Harris: Corporate Tax Winners And Losers

Bull Steepening Is Bearish For Stocks – Part Two

Comments

Log in or sign up to join the conversation.