7 Potential High Dividend Growth REITs To Watch

For income-focused investors, real estate investment trusts (REITs) offer the attractive combination of moderate to high yields and the potential for substantial dividend growth. New REITs hit the market through IPO’s or spin-offs and typically come with an exciting story and not much of a track record. With my focus on the safety of dividend payments and visibility of future dividend growth, I like to let new REITs get seasoned in the market before I make an investment decision.

My REIT database includes seven REITs that launched with IPO’s and are now approximately one-year-old as publicly traded companies. Let’s take a quick review of what has happened with each from the IPO until the present time.

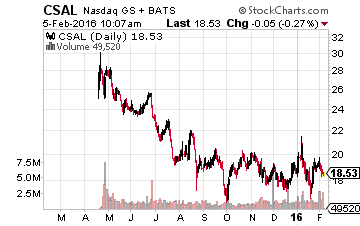

Communications Sales & Leasing Inc. (NASDAQ: CSAL) was spun-off by telecom company Windstream Holdings, Inc. (NASDAQ: WIN) with an April 2015 IPO. With the spin-off, CSAL received Windstream’s 3.5 million mile fiber network and 235,000 miles of copper wire lines. These assets market CSAL as a new type of REIT. At its launch, the REIT had just the single customer, Windstream, with a long-term contract that provided enough cash flow to support an initial $0.60 per share quarterly dividend rate. CSAL management’s stated goal is to acquire additional telecom infrastructure assets to grow revenues and distributable cash flow.

In January 2016, the company announced its first acquisition, a $409 million deal to purchase PEG Bandwidth, a provider of cell site backhaul and dark fiber for telecoms. The CSAL shares had a $30 IPO price and now trade for less than $19. The fairly secure dividend provides a near 13% yield. If CSAL can grow FFO per share and diversify its customer base, this will be a very attractive investment going forward.

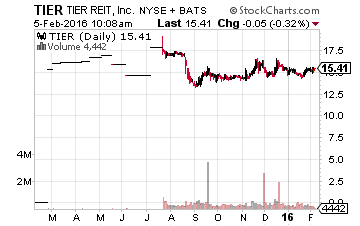

TIER REIT Inc. (NYSE: TIER) is an office REIT that was a non-public REIT that transitioned to a publicly traded company in July 2015. The company owns about 30 Class A office buildings in 15 cities. Management claims net operating income growth potential of 33% (13% annualized) between the end of 2015 and the end of 2017. With its first two quarters as a public company, cash flow results were one-quarter lower by about 10% and one-quarter higher by a similar percentage compared to results when TIER was a non-public company. This REIT needs to show more stable cash flow growth

This REIT needs to show more stable cash flow growth and, at least, one dividend increase before I will again take a closer look at its investment potential. TIER currently yields 4.7%, an above average rate for a high-quality office REIT.

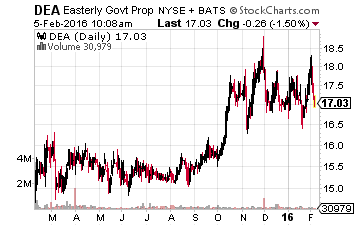

Easterly Government Properties Inc. (NYSE: DEA) lives up to its name with a business focused on the acquisition, development, and management of Class A commercial properties that are leased to U.S. Government agencies. DEA came to market with a February 2015 IPO. Business results since the IPO have focused on the acquisition part of the equation, buying six properties to bring the portfolio total to 32 since the IPO. The company also increased its dividend by 5% after its second full quarter as a public company. So far DEA has shown an attractive portfolio and cash flow growth trajectory. With a current 5% dividend yield, it may be time to start accumulating shares.

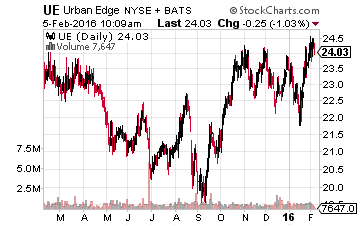

Urban Edge Properties (NYSE: UE) is a strip mall operator that was spun-off by Vornado Realty Trust (NYSE: VNO) in January 2015. UE has paid four consecutive $0.20 dividends since the IPO and has generated a steady quarterly FFO of $0.30 per share. To date, cash flow and dividend coverage are good, but there has not been significant revenue or FFO growth. With a current 3.3% yield, Urban Edge does not offer a compelling investment opportunity.

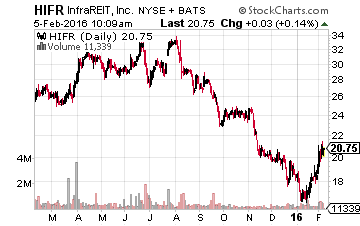

InfraREIT Inc. (NYSE: HIFR) is another new type of REIT, owning electric power transmission and distribution lines. All of the company’s current assets are located in Texas. The assets are leased by Sharyland Utilities, LP which is a Texas-based public electric utility. Growth potential comes from rights of first offer on assets owned by the REITs external manager, Hunt Utility Services, and third party acquisitions. The company believes it can participate in the electric utility service growth in Texas fueled by economic growth. Distributable cash flow should be very steady and the $0.23 quarterly dividend represents 82% of the cash available for distribution. I would wait on this REIT to see if it can make acquisitions and grow cash flow per share to support a growing dividend. HIFR currently yields 4.3%.

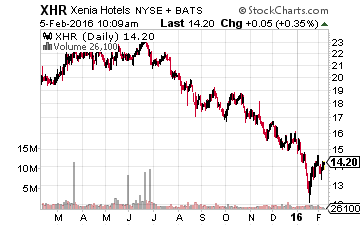

Xenia Hotels & Resorts Inc. (NYSE: XHR) launched with a February 2015 IPO. Last year was terrible for the hotel REITs as a group, and the XHR share price has mirrored the sector, losing one-third of its share value since the IPO. Xenia appears to be a well-managed lodging REIT. The current problem is with all of the hotel REITs. The question is the market right now and the recent revenue growth trajectory is over or is the market wrong and the hotel REITs will continue to grow cash flow and dividend rates. Through the first three quarters of 2015, XHR grew FFO per share by 26% and there is plenty of room for a dividend increase. If cash flow growth continued through the end of the year, XHR (and a few other quality hotel REITs) have tremendous total return potential in 2016. XHR currently yields 6.5%.

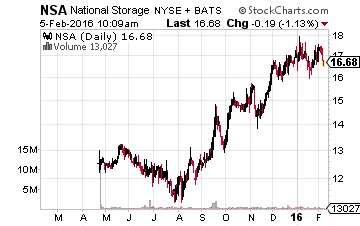

National Storage Affiliates Trust (NYSE: NSA) came to market with an April 2015 IPO. Self-storage may be the hottest REIT growth sector. In its third quarter earnings, NSA reported 14% year-over-year core FFO per share growth. Soon after, the company increased its dividend by 5.2% after less than two full quarters of public operating. The investment question concerning NSA is whether to go with the newcomer to the self-storage sector and take a chance on the growth rate or stick with a proven performer like Extra Space Storage, Inc. (NYSE: EXR), which has been able to increase dividends at a 20% annual growth rate. I need to see a few more quarters of results from NSA before deciding on its investment potential. The shares yield 4.7%, which is well above the yields on the more established self-storage REITs.

As you can see, there are a couple here that are already showing signs of winning investment choices and several more that still have something to prove.

Finding stable companies that regularly increase their dividends is the strategy that I use myself to produce superior results, no matter if the market moves up or down in the shorter term. The combination of a high yield and regular dividend growth in stocks is what has given me the most consistent gains out of any strategy that I have tried.

Disclosure: more