Burning Time With The Unbalanced Butterfly

Today, we are looking at the unbalanced butterfly. We will discuss the trade set up and walk you through some examples. Let’s get started.

Introduction

The unbalanced butterfly is an options strategy that has three short legs located at the same strike. An unbalanced butterfly strategy has positive theta, which means that it benefits as time passes. The at-the-money strike generally has the highest extrinsic value. That means that it has the most time premium to lose as it goes to expiration.

Putting all three short legs of the unbalance butterfly near the stock price allows us to sell time premium, especially if the stock is range-bound and implied volatility is high.

Unbalanced Butterfly Example – Post Earnings Reaction

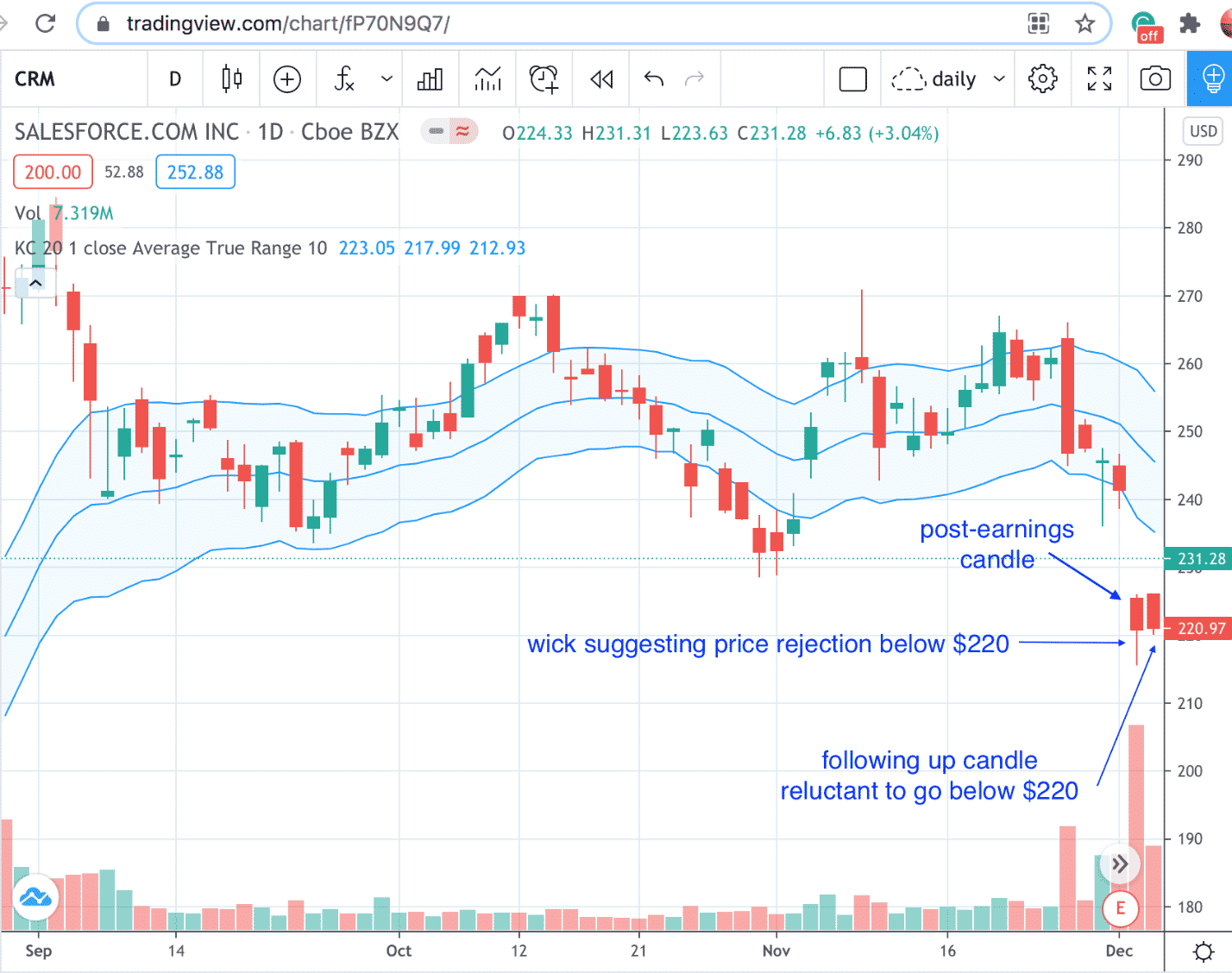

Salesforce (CRM) reported earnings after the market closed on Dec. 1, 2020. The following trading day, the price gapped down outside of the Keltner Channels. It resulted in a candle with a bottom wick, suggesting price rejection below the $220 level.

Let's say the investor watches for one more day on Dec. 3. If it continues to trade lower, the investor will assume that Salesforce stock is still on the move as spurred by the earnings announcement. It just so happens that it did not trade below the previous day’s low.

The investor initiates an unbalanced butterfly at the end of the market day on Dec. 3. Here are some details of this example trade:

- Date: Dec. 3, 2020.

- Price: $220.97.

- Buy: Two Jan. 15 CRM $230 put @ $17.00.

- Sell: Three Jan. 15 CRM $220 put @ $11.10.

- Buy: One Jan. 15 CRM $210 put @ $7.08.

- Debit: $777.50.

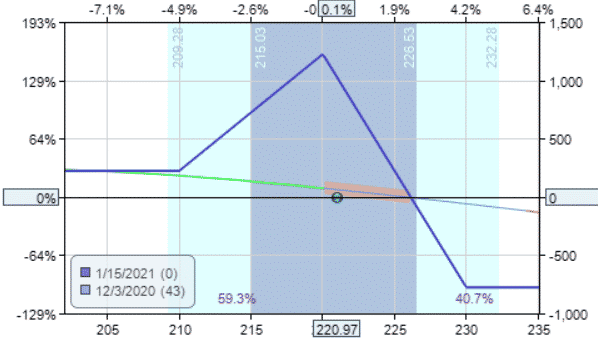

The payoff diagram looks as follows:

The trade is structured to eliminate risk on the downside. Since the stock often continues in the direction of the earnings gap, we don’t want any risk should the price continue downward. The max risk of $777.50 is on the upside.

The extrinsic value of each leg is:

- $210 put: $7.07.

- $220 put: $11.10.

- $230 put: $7.97.

As you can see, the at-the-money strike of 220 had the highest extrinsic value. We are sellers of that leg. And buyers of the other two legs. Computing the net extrinsic value, we get:

- $1110 x 3 + $707 x 1 + $797 x 2 = $1029.

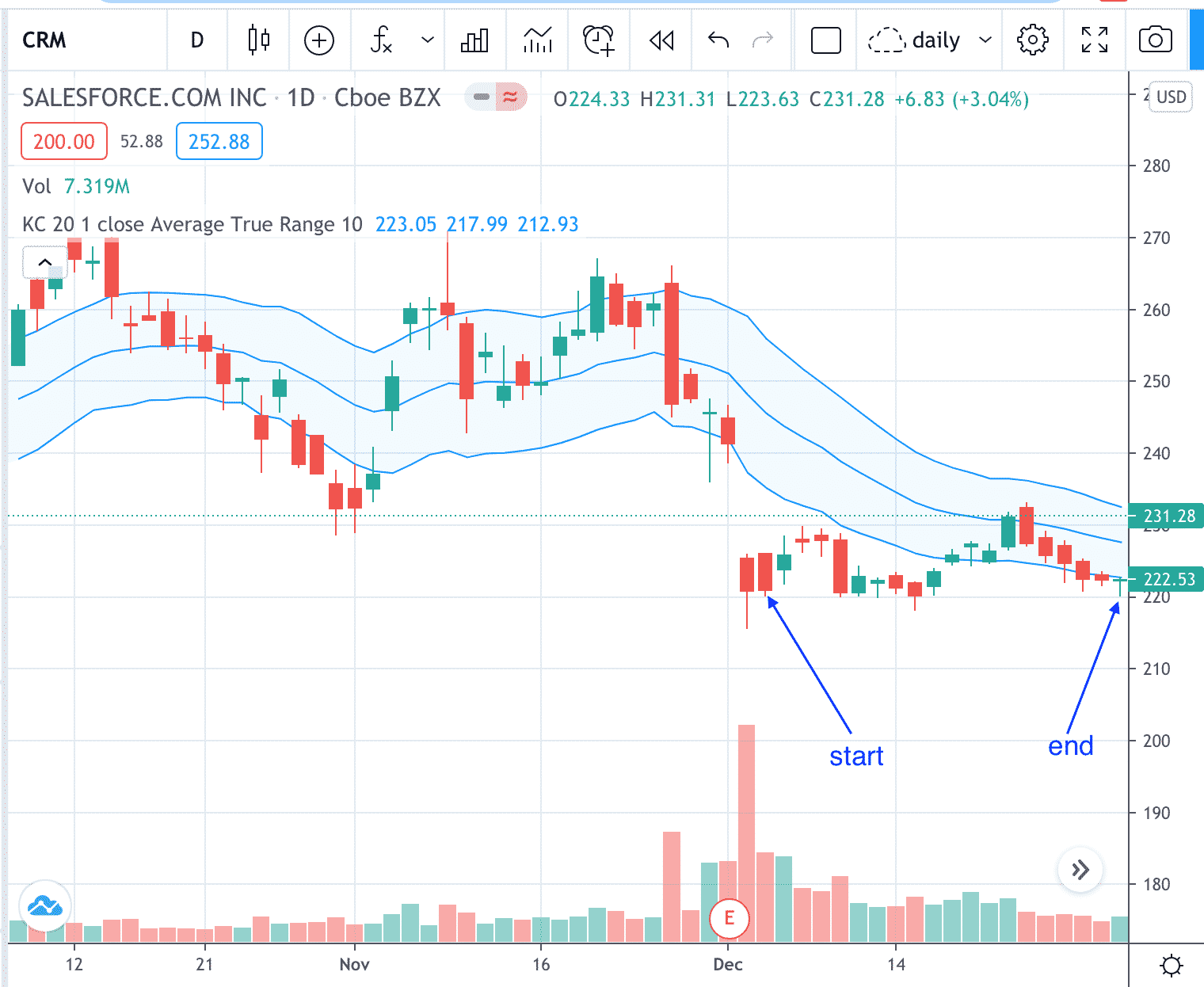

The investor plans to exit the trade if losses exceed $388.75, half of the initial debit invested. The target profit is 10% to 15% of the initial debit. On Dec. 31, CRM closed at $222.53. The trade reached the profit target. The investor exited the trade with a profit of $102.50, or 13% of the initial capital invested.

The stock cooperated nicely by trading sideways for 19 trading days and held the $220 level like a straight edge. The extrinsic value of each leg at exit are:

- $210 put: $1.58 (lost $5.49, or 78%).

- $220 put: $4.32 (lost $6.78, or 61%).

- $230 put: $2.63 (lost $5.34, or 67%).

On a dollar-per-share basis, the center short $220 strike lost the most extrinsic value. We would like the center $220 strike option leg to lose value because we sold that leg. We do not want the other two legs to lose value because we are long those legs.

The investor’s net profit can be calculated as:

- $678 x 3 – $549 x 1 – $534 x 2 = $417.

Overall, the investor benefited from the extrinsic value changes. Of course, many other factors affected the pricing of the three legs, which then translates into the final P&L.

Net Sellers of Extrinsic Value

The unbalanced butterfly is similar to the broken wing butterfly and is a positive theta trade. Positive theta means that it profits as time passes. We are net sellers of extrinsic value. Extrinsic value is the extra price tacked onto an option representing market participants’ perceived additional value due to time opportunity and implied volatility. Extrinsic value decreases with time as it approaches expiration.

There is less time for opportunities to occur. As such, extrinsic value and time premium are the same thing. As net sellers of time, we are watching time burn away with each passing day.

We sold $1029 worth of extrinsic value at the start of the trade. To exit the trade, we had to buy back $612 of extrinsic value. Selling high at $1029 and buying low at $612 means that we gained $417. $612 was computed by from:

- $432 x 3 – $158 x 1 – $263 x 2 = $612.

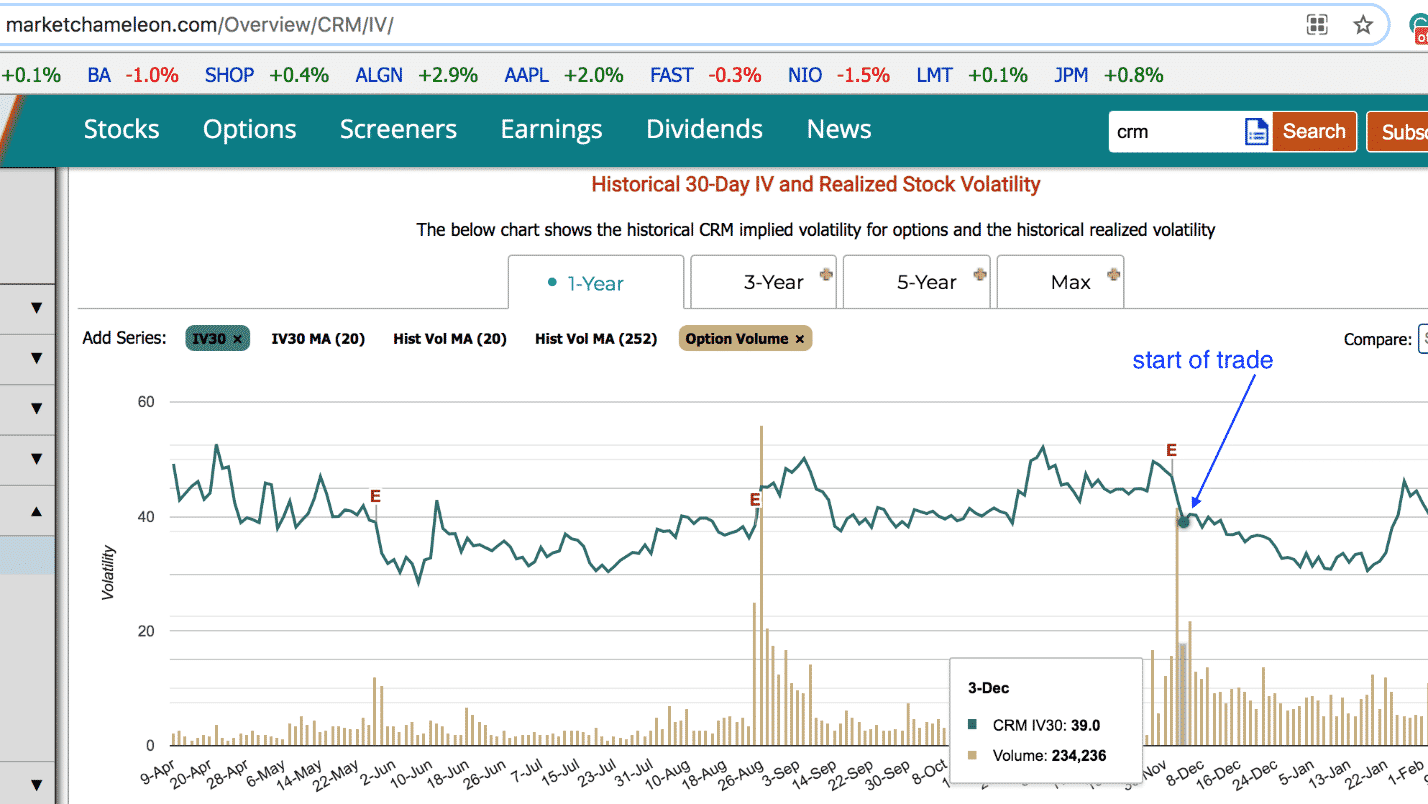

Extrinsic value also decreases if implied volatility decreases. While it is true that implied volatility had already made a big drop post-earnings right before the trade was initiated, it does not mean that implied volatility cannot still go down further. In fact, the implied volatility of Salesforce continued to drop many days after earnings.

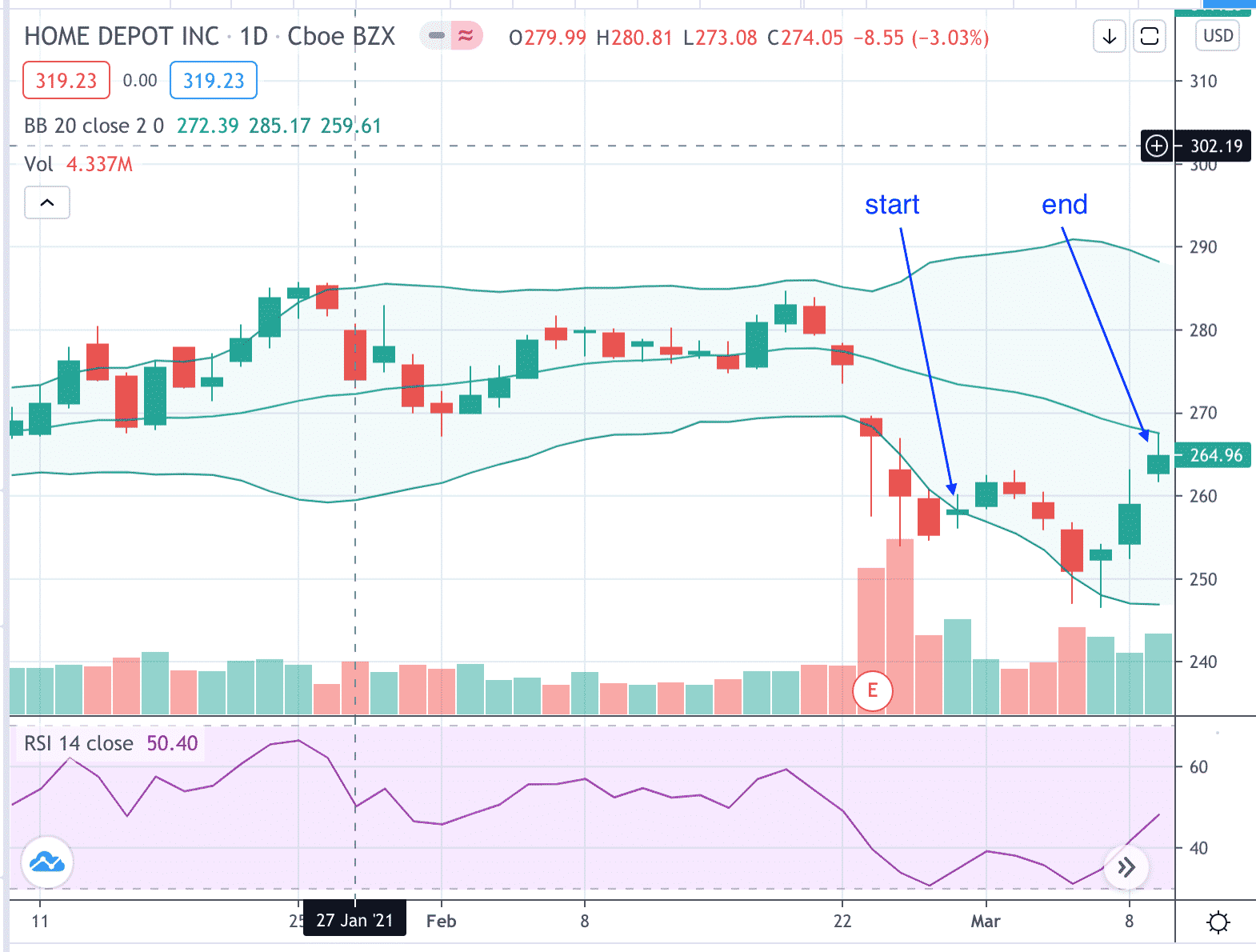

When The Selloff Stops

In the latter half of February 2021, Home Depot (HD) started on a steep selloff. When the investor sees that RSI bounces up from 30 putting in a Doji candle, the investor assumes that the selloff has stopped and initiates an unbalanced butterfly, taking advantage of the heightened implied volatility due to the selloff.

- Date: Feb. 26, 2021.

- Price: $258.34.

- Buy: One Apr. 1 HD $265 call @ $5.225.

- Sell: Three Apr. 1 HD $255 call @ $10.05.

- Buy: Two Apr. 1 HD $245 call @ $17.20.

- Debit: $947.50.

The Greeks:

- Delta: 12.07.

- Theta: 2.41.

- Vega: -10.23.

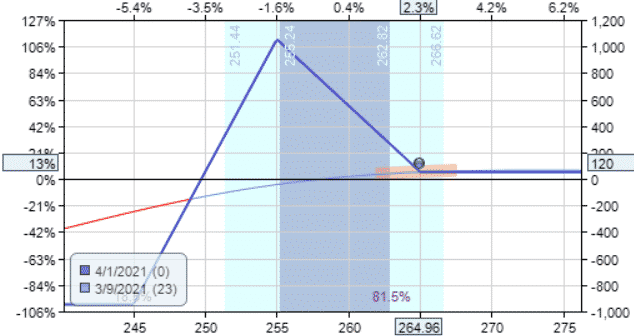

On March 9, the trade exited with a profit of $120, or 13% of the initial debit.

Conclusion

If you can find situations where a stock trades sideways while implied volatility drops, then the unbalanced butterfly can take advantage of theta decay. The exciting thing about the unbalanced butterfly is that we are buying the butterfly with a debit. Yet, we are net sellers of time value.