Rates Strategy: It’s A Camel!

EU leaders reached a deal on the recovery fund that broadly follows the outlines of the compromise that had taken shape over the past few days. We see the path cleared for the 10Y Italy-German spread to go through our 150bp target this summer. Thanks to reassurance from the ECB, demand for carry trades should remain healthy over the summer months.

EU deal on recovery fund clears path towards tighter spreads over the summer

EU leaders reached a deal on the recovery fund this morning. The overall size remains at €750bn of which €390bn will be disbursed as grants and €360bn as loans. 70% of the funds will be disbursed in the first two years according to the key proposed by the EU commission. An agreement has also been reached on the next multiannual budget for 2021-2027 of €1,074bn.

The agreement on the recovery fund largely follows the compromise that had already shaped over the past days, and which had already been received positively by markets, that is if we take the performance of government bond spreads as an indicator. With drawn-out negotiations having been avoided, we see the path cleared for the 10Y Italy-German spread going through our 150bp target this summer. As we have outlined before, the carry benefit of peripheral debt, and lower prospective volatility thanks to the ECB intervention, make it a superior alternative to core bonds, in our view.

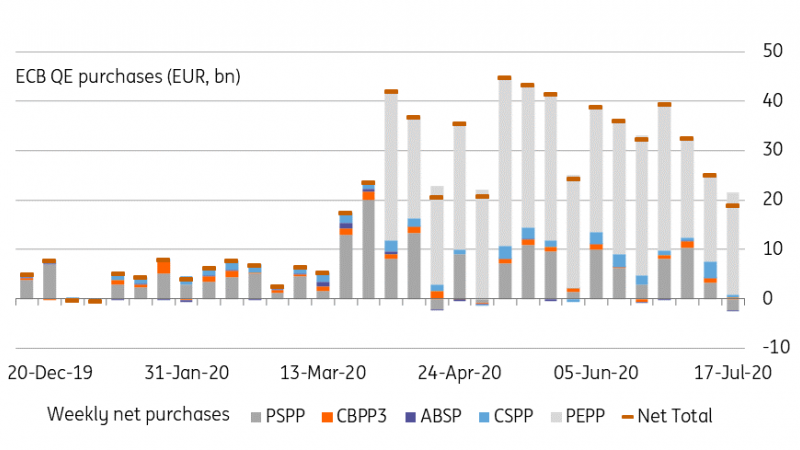

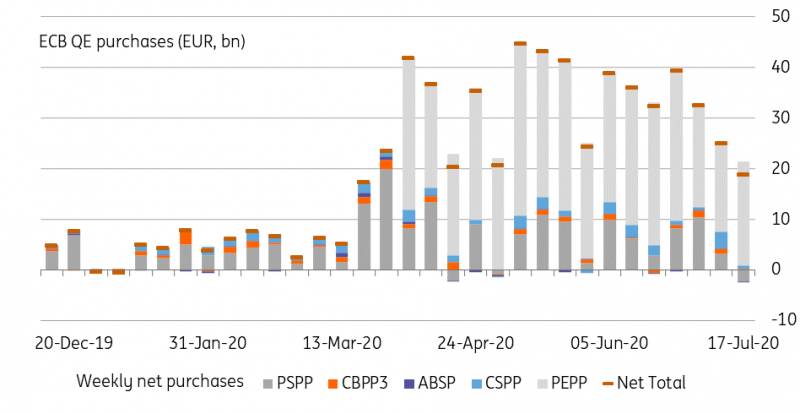

ECB net purchases slow further

Total ECB net asset purchases in the week ending on 17 July fell to €19bn, marking the lowest weekly volume since purchases were ramped up in March as a reaction to the Covid-19 crisis. But markets have been on the mend since then and the ECB will be taking a step back over the summer weeks as usual. Last week’s net figure will also have been skewed lower by sizeable government bond redemptions from the public sector purchase programme (PSPP) portfolio, which saw a net decline. Net purchases via the pandemic emergency programme amounted to €20.6bn.

But as the ECB's Schnabel has cautioned in a recent interview, one should not read too much into the slowing purchases. Reiterating that, President Lagarde stated that in the ECB's economic baseline scenario that the PEPP envelope would be spent in full, adding that the risks to the scenario are currently still tilted to the downside.

Lowest overall weekly net QE volume since PEPP became active

Source: ECB, ING

Today's events: Schatz auction and ECB speakers

In primary markets Germany will reopen its 2Y benchmark bond for €5bn.

An otherwise quiet day will see attention shifting to comments by the ECB’s VP de Guindos and Greek central bank governor Stournaras.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more