Market Briefing For Wednesday, August 12

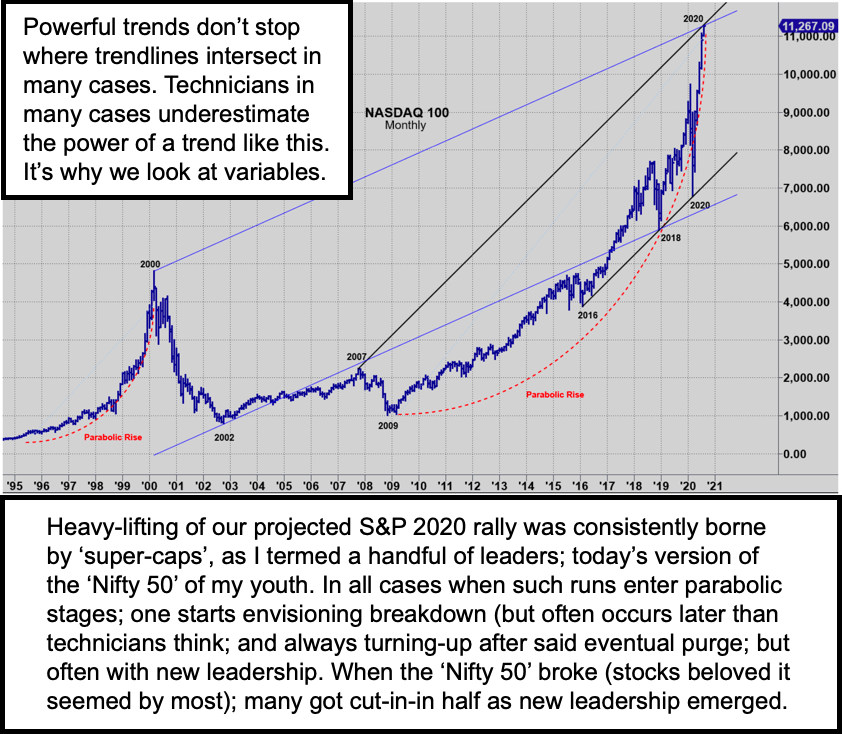

(Today's NDX shakeout also occurred at the obvious noted intersection. That's one reason for those comfortable with the downside to be surprised if we get a rebound, as I suspect is coming, even if it's part of a swansong of 'super-caps' just for now.)

~

The 'political talks stalemate' Senator McConnell referred to mid-afternoon didn't help at all, and at that point the overall S&P (SPX) and DJI (DIA) turned down to join essentially all-day pressure on the Nasdaq (QQQ), NDX (NDX) and Semiconductors (SMH). Was it a definitive session?

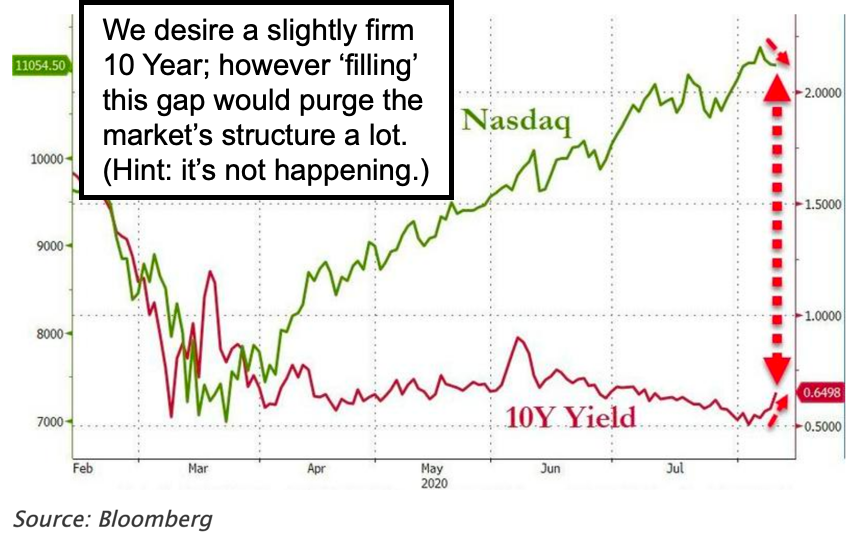

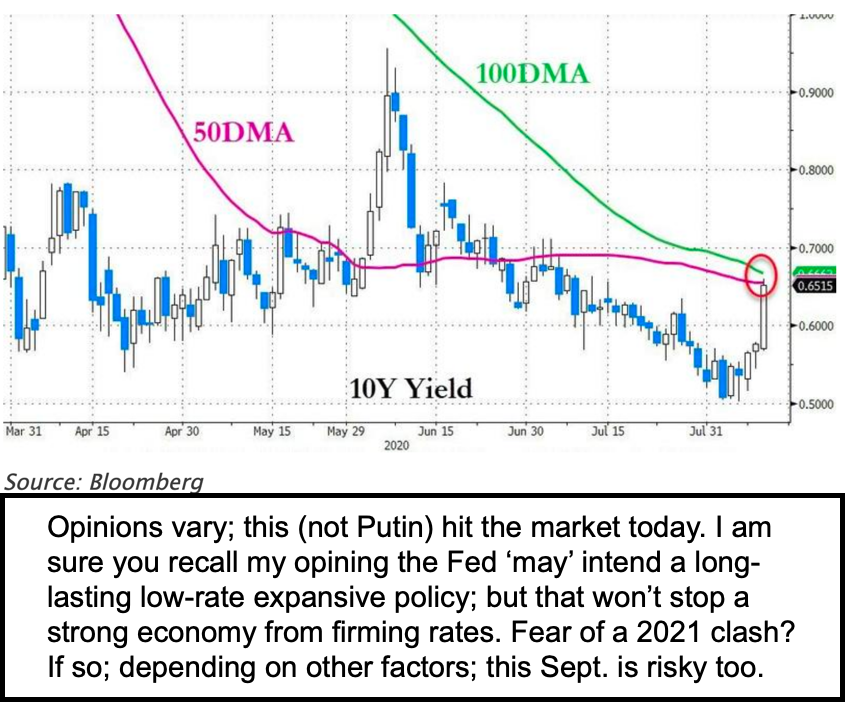

Of course that depends on follow-through, and given that much of this might attribute to the 10-year Treasury (SPTL) rally (more so than the Nasdaq break), as well as how that hit Gold & Silver, (GLD, SLV) there might be sobering aspect to this, noting that recovery boosts rates even if this is just a preview, and that can be regardless of Fed desires to hold down rates. And immediately it might be enough to get DC politicians to finally meet and arbitrate their differences regarding emergency needs.

Executive summary:

- Breadth shifted (and even stayed positive), but that's because it moved further into a broad variety of industrial and economically suppressed issues.

- As frequently noted, while the broadening-out is welcomed (even essential) to get things going, the basic stocks couldn't offset pressure on 'super-caps'.

- Oddly, the jobs numbers were starting to sway some politicians that less was needed on the stimulus front, so now the pressures on equities (and concerns about reliability of vaccines as well as lack of serious antiviral treatments) might actually serve to push the politicians back to finally making a deal.

- Biden's choice of Kamala Harris as his running mate is surprising to some, but not to me, she has depth and legal knowledge, but isn't liked by some, notable in his criticism is that Trump had donated $6000 to a prior election campaign of hers (of course Trump was a Democrat for many years, don't remind him, lol).

- Also Harris isn't lumped in the radical left crowd, so perhaps that's a plus too. Trump already criticizing the Senator on taxes and questioning during hearings, but guess what, that's typical politics, and since she and Biden sparred, maybe the reality she is not part of a 'Squad new deal' crowd, got her the nomination.

- Enterprise value of many stocks trying to bottom now is questionable, given the borrowings and overall Debt situation, but the market is probing structure for a post-Covid era, that if we keep calm with China, might be a global resurgence.

- No doubt a market shakeout (even correction) has been due and overdue for some time (mentioned for over a month as coming, not not yet (now was likely a preview of 'yet'), and we are in a sensitive seasonal time, aside politics.

- The mix increasingly becomes unstable, if not toxic, and is why even while saying nothing catastrophic looming, we shouldn't expect much for S&P's and also allow generally for a retrenchment.

- Even the stable Dollar, combined with slightly firmer rates, to break Gold a bit, in a mixture that has what some see as 'greedy sentiment' sobered generally.

- August's 2nd half is sensitive, as many are aware that September is often a poor if not negative month, and if not then October, but usually not both months.

- The S&P is dominated by the narrow-universe big-caps and its sensitivity sort of spilled-over into this so-called 'value replacing growth' as the focus, pattern for 2021, a year in which stabilization may do more for the economy, than big-caps.

In-sum: A day of some drama, culminating with a sense of relief among many folks, as regards market implications of political prospects that are a choice between Team Trump and a Democratic slightly left of center ticket, but not revolutionary radical in any way. It suggests, that if The White House turns over, it's not a major impediment for the market and economic progress, although the focus will change somewhat.

We haven't said much about Covid-19 tonight, I think everyone knows the higher rate of death in Florida (worst day ever) and varied situation nationally and globally. As a frustrated Dr. Fauci has noted, we'll be buying advance doses of vaccine that may or may not be effective, but that's the decision made. Again today was a Treasury rate response more than reaction to Russia's vaccine, which everyone is critical of, but at the same time I hope it is safe and works, because it's a different design that newer approaches here, but it if works and can protect millions, we'll applaud it.

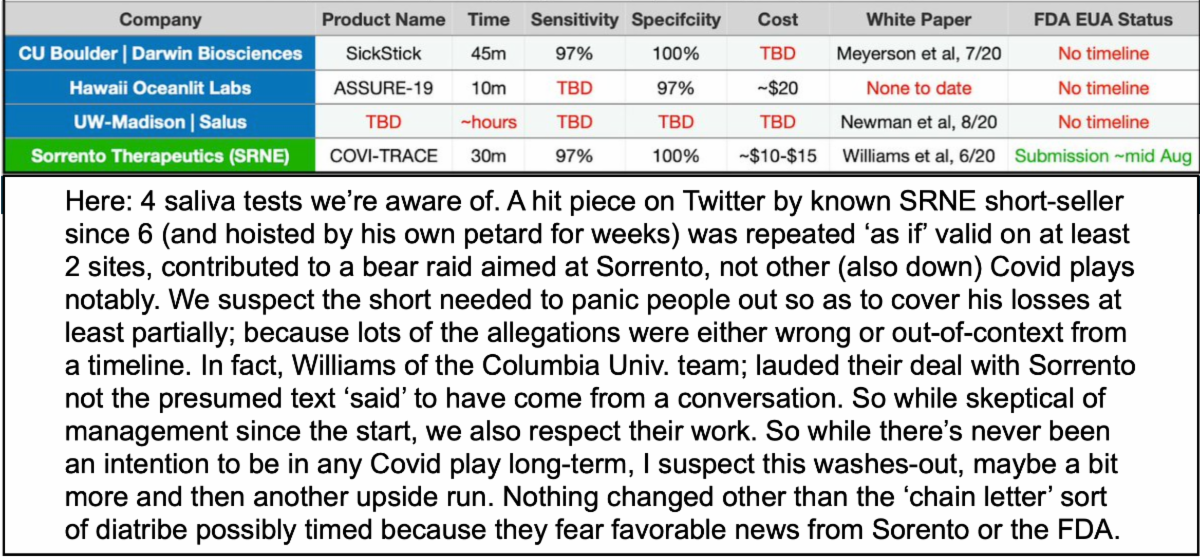

No way to know if Putin expedited a vaccine for first-mover advantage, but everyone is short-cutting all kinds of normally-painstaking tests to get a solution. We still count on therapeutic drugs, if it comes to that for anyone this year. And preferably even an upcoming prophylactic approach, which a few companies are working on; including Sorrento (SRNE) and Merck (MRK). Of course that's distinct from the many variations of on-site tests rolling-out soon, in some cases from biotech's working on multiple solutions.