May 2021 Empire State Manufacturing Index Declines

The Empire State Manufacturing Survey index marginally declined but remained in expansion.

Analyst Opinion of Empire State Manufacturing Survey

Key elements are in positive territory and all improved. This report is considered about the same as last month.

Econintersect reminds you that this is a survey (a quantification of opinion). Please see the caveats at the end of this post. However, sometimes it is better not to look too deeply into the details of a noisy survey as just the overview is all you need to know

- Expectations from Econoday were between 20.0 to 30.0 (consensus +25.0) versus the 24.3 reported. Any value above zero shows expansion for the New York area manufacturers.

- New orders sub-index of the Empire State Manufacturing improved and remains in expansion, whilst the unfilled orders improved and remains in expansion

- This noisy index has moved from -48.5 (May 2020), -0.2 (June), 17.2 (July), 3.7 (August), 17.0 (September), 10.5 (October), 6.3 (November), 4.9 (December), 3.5 (January 2021), 12.1 (February), 17.4 (March) , 26.3 (April) - and now 24.3

Business activity continued to grow at a solid clip in New York State, according to firms responding to the May 2021 Empire State Manufacturing Survey. The headline general business conditions index was little changed at 24.3. New orders and shipments continued to expand strongly, and unfilled orders increased. Delivery times lengthened significantly, and inventories moved somewhat higher. Employment levels grew modestly, and the average workweek increased. Both input prices and selling prices rose at a record-setting pace. Looking ahead, firms remained optimistic that conditions would improve over the next six months, and expected significant increases in employment and prices.

ACTIVITY REMAINS VIGOROUS

As occurred last month, manufacturing activity grew at a sturdy pace in New York State in May. The general business conditions index edged down two points to 24.3. Thirty-seven percent of respondents reported that conditions had improved over the month, while 13 percent reported that conditions had worsened. The new orders index moved up two points to 28.9, a multi-year high, and the shipments index climbed five points to 29.7, pointing to another month of strong gains in orders and shipments. Unfilled orders increased. The delivery times index moved down five points, but at 23.6, it held near its record high from last month, pointing to significantly longer delivery times. Inventories moved somewhat higher.

The above graphic shows that when the index is in negative territory that it is not a signal of a recession - of 8 times in negative territory (since the Great Recession and before the COVID recession) - no recession occurred. Conversely, a positive number is likely to be indicating economic expansion. Historically, when it does make a correct negative prediction it can be timely - this index was only two months late in going negative after what was eventually determined to be the start of the 2007 recession.

This survey has a lot of extra bells and whistles which take attention away from the core questions: (1) are orders and (2) are unfilled orders (backlog) improving? - and the answer is that the key internals are in positive territory but new orders marginally declined.

Unfilled order contraction can be a signal for a recession.

Summary of all Federal Reserve Districts Manufacturing:

Richmond Fed (hyperlink to reports):

Kansas Fed (hyperlink to reports):

Dallas Fed (hyperlink to reports):

Philly Fed (hyperlink to reports):

New York Fed (hyperlink to reports):

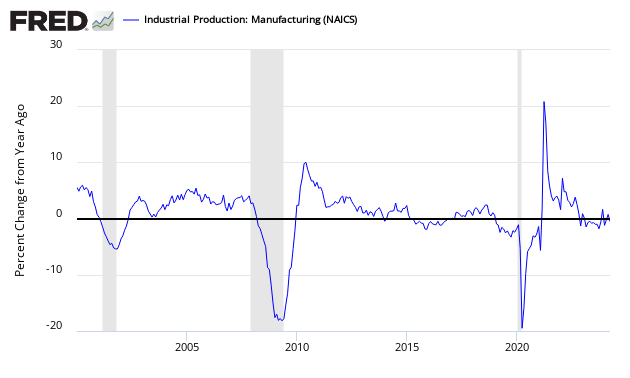

Federal Reserve Industrial Production - Actual Data (hyperlink to report):

Holding this and other survey's Econintersect follows accountable for their predictions, the following graph compares the hard data from Industrial Products manufacturing subindex (dark blue bar) and US Census manufacturing shipments (red bar) to the New York Fed survey (green bar).

In the above graphic, hard data is the long bars, and surveys are the short bars. The arrows on the left side are the key to growth or contraction.

Caveats on the use of the Empire State Manufacturing Survey:

This is a survey, a quantification of opinion - not facts and data. Surveys lead hard data by weeks to months and can provide early insight into changing conditions. Econintersect finds they do not necessarily end up being consistent compared to hard economic data that comes later, and can miss economic turning points.

According to Econoday:

The New York Fed conducts this monthly survey of manufacturers in New York State. Participants from across the state represent a variety of industries. On the first of each month, the same pool of roughly 175 manufacturing executives (usually the CEO or the president) is sent a questionnaire to report the change in an assortment of indicators from the previous month. Respondents also give their views about the likely direction of these same indicators six months ahead.

This Empire State Survey is very noisy - and has shown recessionary conditions throughout the second half of 2011 - and no recession resulted. Overall, since the end of the 2007 recession - this index has indicated two false recession warnings.

No survey is accurate in projecting employment - and the Empire State Manufacturing Survey is no exception. Although there is some general correlation in trends, month-to-month movements have not correlated with the BLS Service Sector Employment data.

Over time, there is a general correlation with real manufacturing data - but month-to-month conflicts are frequent.

Disclaimer: No content is to be construed as investment advise and all content is provided for informational purposes only.The reader is solely responsible for determining whether any investment, ...

more