Market Briefing For Wednesday, April 22

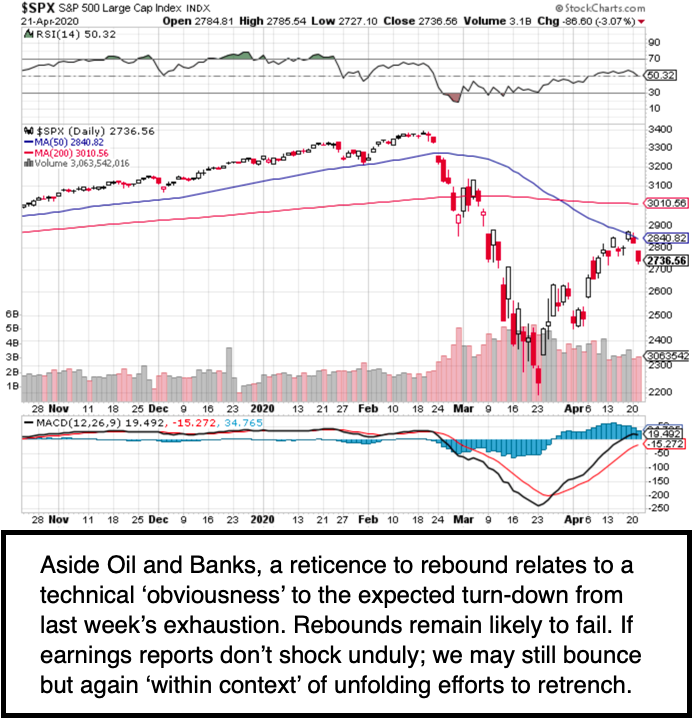

Sketchy factors dominate the backdrop for this stock market, as it sure did make an 'exhaustion' peak last week as outlined; and makes that very clear by its difficulty executing even a fairly normal post-shakeout rebound, of course as part of a process of working lower. And the S&P rebuff of the 50-Day Moving Average is pretty clear.

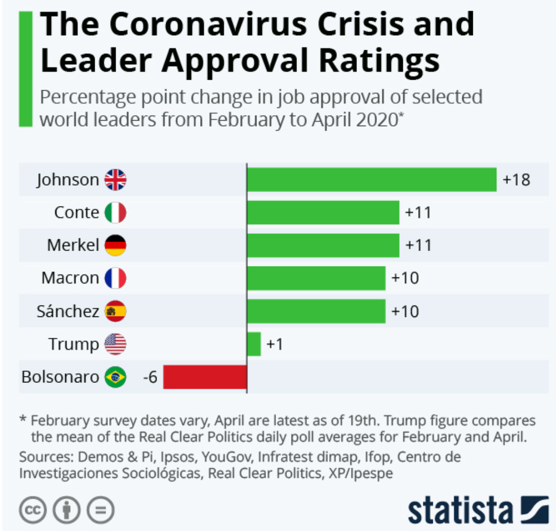

These are time of higher S&P volatility in every way (both directions, often alternating) and we think dice-rolling with regard to economic opening up. I hope the U.S. can do it more like Denmark than Sweden, but both jumped on it earlier, and even now they don't permit massages or tattoos (no idea what's gotten into Georgia's mind on that), but we all hope it goes well. As 'hope is not a strategy' I thought the White House too, diplomatic on this.

Nearly everything at this point comes-back, directly or indirectly to Covid-19.

Executive summary:

- President Trump is eager to reopen the U.S. economy and save it from a crushing Depression, hence his slightly contradictory reactions with regard to his own guidelines versus 'opening up' fast ('we get it')

- That's likely why he pressed AG Barr to start 'leaning-on' Governors who fail to reopen states in-presence of 'reduced' Covid-19 cases (a story in today's stream of events that's barely noticed)

- Senate approves new $484 Billion package to help businesses

- The danger of reviving the economy too soon is that it could spark a second wave of coronavirus of course, so this is controversial and actually unknown, as we all want the economy safely functioning

- Takeshi Kasai, the WHO regional director for the Western Pacific, said lifting lock-down measures too quickly will leave countries vulnerable to new surges of infection, which is sort of stating the obvious

- On-behalf of WHO, he urges adjusting to new lifestyles until a vaccine, or a 'very effective treatment' is found (I favor an oral pill solution), I'm in-doubt lifestyle change works for Americans whose impatience is evident, so we do need to be careful about this reopening saga

- Notable: contradicting some of the optimism; CDC Director says that possible second wave of infections will be likely worse, good point is that the CDC hasn't been providing their direct interviews as before

- I have no idea if 'reality' puts Dr. Redfield in conflict with the President; at the same time it is likely just a reminder to take things responsibly

- CDC comment states the obvious risk that exists without mitigation as (by Fall) an effective antiviral drug (oral ideally) could address,

- Rick Bright, Director of Agency in-charge of antiviral efforts (BARDA) oversight, has resigned his position and moving elsewhere at NIH, it may be part of the conflict within Government about this issue

- My view continues: that S&P soars from any level, at the point of an FDA recognition of a safe & effective 'oral' treatment, as is needed to allow prescribing on early Covid symptoms, before hospitalization, it's also why combination 'immediate' tests are absolutely essential

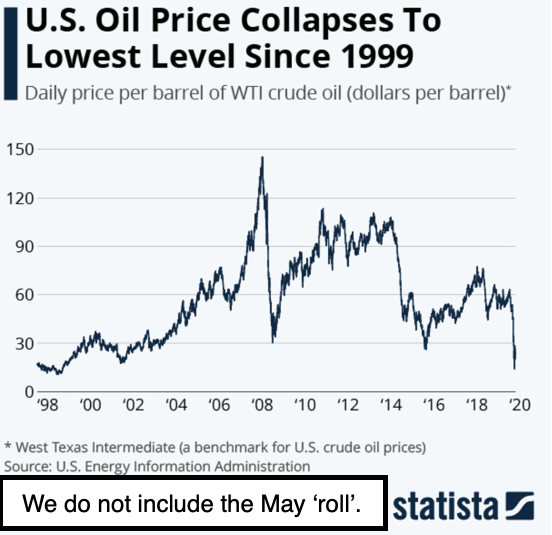

- Trump asks 'Energy Dept.' to make a 'plan' to protect US oil industry; but dynamics haven't changed, as oil markets say what we all know as June WTI tanks in-the-wake of May, as speculated to likely follow

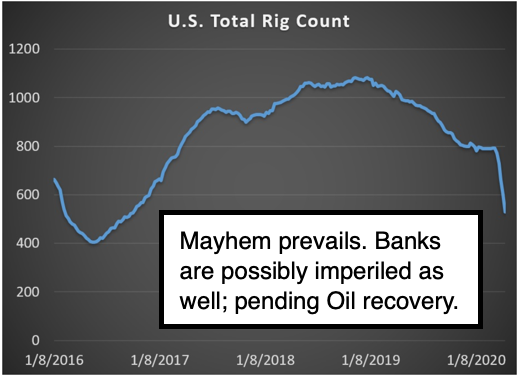

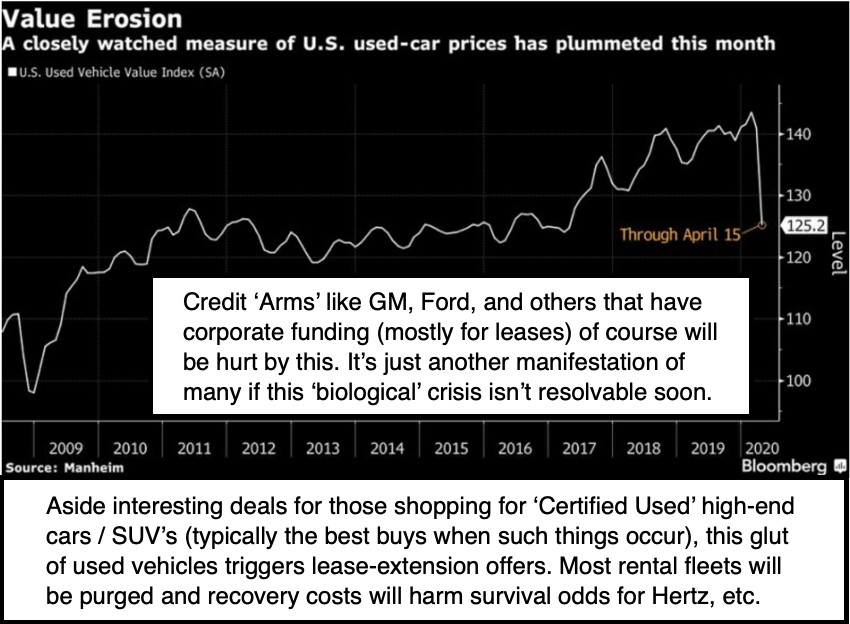

- This is uncharted territory especially as relates to banks, and also I suspect to gold, which may rally anew 'if' banking woes perceived, and if you want an argument for downside it's coming back to bank loan-loss reserves likely inadequate as I pointed-out a while ago

- Texas Railroad Commission met today and was reluctant to dial-back oil production..so instead is 'researching', which means nothing, or it may be irrelevant because 'price' has triggered wide shut-downs

- Remember oil projects are generally lender-financed and bank loan reserve provisions likely do not account for this collapse, so it's thus another way that side-effects of a biological crisis become financial

- Hence the banks will be in 'earnings hell' more so than simply due to the mitigating factor of the pandemic or income from loan originations (as they get paid a fee to handle processing the PPP and SBA loans, even if recipients don't pay a fee or interest)

- The larger banks are more resilient only because most oil producers in shale or so on are smaller operators typically utilizing regional banks, most of those are on NASDAQ, not NYSE, so may be defensive

- North Korea: unclear if Little Rocket Man Kim is alive or not, sources on the Peninsula claim that he is just recuperating from CVD surgery

- United Airlines (UAL) announced a 29 million share secondary offering, that would be from 1-3 billion depending on price, and shares are softer, it may be the first of several airlines to go for dilutive financing

- Netflix (NFLX) added lots of subscribers; sort of missed earnings; admits viewership and revenue 'may' decline as world emerges from virus, it is seemingly a bit tired, and might have real competition showing-up a few weeks from now; as HBO Max rolls-out and has millions of homes from the get-go, how AT&T (T) characterizes that tomorrow matters (if it is successful the mixed platforms of 'T', along with high yield, are fairly unique and could enhance total return over a period of time)

- Texas Instruments (TXN) made their numbers and gave wide variable forward guidance, which probably characterizes most tech for now

- Finally, AT&T reports tomorrow and has a quite different profile now than their industry peers (see my remarks within Netflix, as I suspect the shuffling of personnel and inclusion for of HBO Max for most of the higher-end AT&T wireless customers gets it off to a strong start).

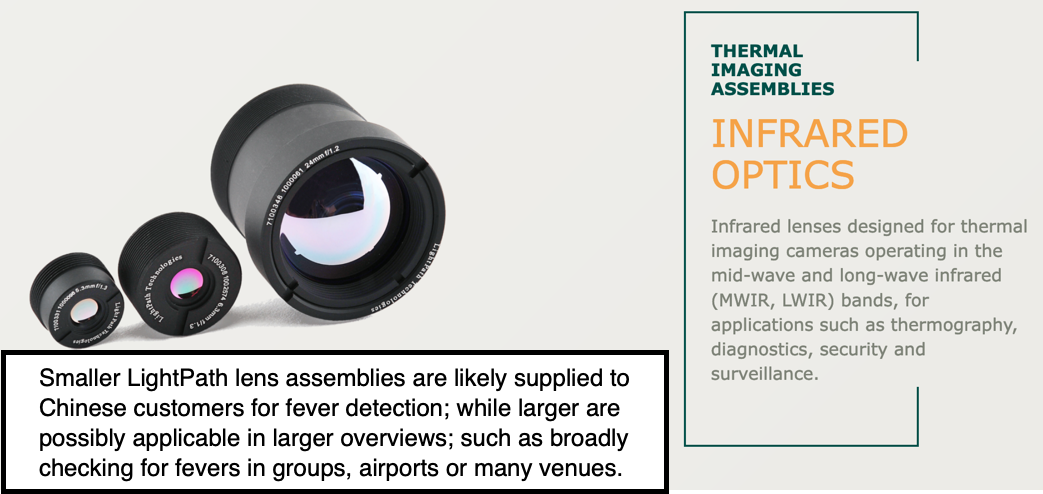

Meanwhile . . . we depart pure viral discussions as relate to markets for a rare glance at one stock that is alternatively a blessing and a curse over the years,depending on your timing. So, about 3 months ago I returned LightPath Technologies (LPTH) from the back-burner (former stock of interest) to front-burner (newly focused-upon) status.

The speculative small-cap stock at the time doubled from sad times near around $.70 (risking de-listing so that needed changing) to near $1.60, and then the 'crash' of the market plunged it back down (along with others) as it reached $.80 or so, with nothing changed other than market liquidation of basically everything, due to the projected decline and coronavirus crash. I viewed that as a second shot at an already-known turnaround, so said it.

On the day of S&P max-fear lows, it was among a handful of issues, that aside normal rebound expectations, for an AMD or AT&T, I singled-out as a potential beneficiary of a 'new normal' world of enhanced security, fever detection, by general visible and infrared monitoring of.. everything. I had already noted (a month or more earlier) it as a speculative buy under $1 as a bit more than a 'shot' because of the financial improvements, the new CEO, sizeable contracts and backlog, without heavy debt encumbrance, and permission to keep their Chinese plants open; because of.. infrared.

(I shared this in mid-February; but it makes the point of their focus now.)

From that 'max-fear' panic day in March, I called for LightPath to gradually increase towards that $1.80 high and ideally take-it-out and move to $2.00 or higher, and noted that it was at a very low multiple (of revenues or various metrics) compared to peers in general fields, even in these tough times. It matters now, because that price level is achieved, but there's little urgency to sell, merely watching daily action (over 1 million shares today, high by a factor of 10 or more compared its average daily trading volume).

So I'm not getting excited now; just pleased it's all working-out well. Also it is not impossible it's borderline 'in-play' for the first time since basically it was restructured with regard to operations, plus the accidental sudden rise in business that (I suspect) relates to product demand due to Covid-19. It matters a lot what they have to say about this at a quarterly call soon. No smoke & mirrors or promises they can't deliver, just transparent reality.

I upgraded it below $1.00, primarily because LightPath, under former CEO for some years Gaynor, had eliminated cash-drain from their ISP Optics New York operations (wholly-owned subsidiary consolidated to Florida and also a plant in Riga Latvia), were growing in infrared lenses (more important now for security, defense and military than the much talked-of, oft-delayed elusive autonomous; or other futuristic endeavors that will be there some day), and with hiring Sam Rubin as President and CEO (effective as of early March), bringing a newfound chutzpah (old Irish expression) onboard as speculated below $1.00 / share. LPTH already appeared to have turned around favorably. It was just before the coronarivus catastrophe compelled an even faster ramp-up of production capacity and apparent demand.

The emergency authorization for LightPath's two plants in China to resume and/or continue production, was indicative of the need for more IR lenses, even if these are low margin, thus volumes were what was needed. At the same time a large domestic contract for a vendor on behalf of US Marines required all modules/lenses be made in the USA, hence more business for Orlando, which apparently has seen a couple rounds of expansion lately.

In-sum: I speculated in comments LPTH backlog may be around $18 million, holding backlog even while revenues grow, sounded fairly robust, even if the CEO's preliminary report tried to sound a conservative tone.

The new CEO Rubin was formerly General Manager of Thorlabs, a techie privately-owned (but far larger) customer of LightPath's for years. There is scuttlebutt, of which I know nothing, that integration or partnership might occur between the two, I have no idea. But I do know (similar to Luminar with which they have a relationship but is also privately held) that any such company, should they join LightPath, like ISP Optics did a few years ago, might find it a method to grow and to go public, through sort of a backdoor way, without the costs or time consumed in doing an IPO.

I do not know if anything like that is up; but I suspect Chairman Bob Ripp is interested in his near-million-share ownership working-out well. So are all shareholders, and the new CEO Rubin has a good managerial record at Thorlabs, and knows this business. We suspect someone or entities continues absorbing shares on each pullback with higher expectations. At this time there is no 2020 NASDAQ institutional update information as yet, thus no way to really know who has been doing off of the buying. Actually I might sense a hint, noting that a 13F filing on Dec. 31st showed RZH (a substantial Connecticut advisor) acquired over 750,000 shares, with none held before that last Quarter. There are no 2020 Filings required..yet. The only reason I note that group is that they show no prior LPTH activity.

Realize the (expected) improved financial picture and new CEO were all this year as part of the turnaround; so I remain curious as to what changes and progress have evolved, for sure beyond their statement of quarterly pre-release information which was favorable but sort of .. bland.

So we're holding with cautious optimism as LightPath continues executing well; and belief that (intentionally or accidentally) they have the right lens and module products at a horrible time for the world; which must focus on need for a level of security monitoring that has never existed before. With new highs for the 52 week highs, it's virtually impossible to measure any target beyond this minimal goal (yes 2 was our minimum) but pretty clear that it's shining for now, and you don't need a diamond-turned BD6 lens to clearly see the volume and absorption on every little pullback. Trend: up. I continue following as I have for 3 months again, and see if they deliver.