|

Executive summary:

- I checked back: Chief of Staff Meadows did 'not' say we're not trying to control it (COVID), he said 'we're not able to control it', that's quite a big difference and I think media and markets missed that nuance.

- Chief of Staff Meadows essentially meant (I think) that the virus cannot be shutdown or seriously controlled by reasonable measure (at this point), I think that's worrisome and everyone can debate how we got here.

- So it simply recognizes reality, rekindles all the arguments about making it to the time when 'therapeutic antibodies' and/or vaccines arrive.

- Despite being an observation (not a policy), media treated it 'as if policy', and that contributed to (as was obvious immediately) market risk.

- Hence some media comments were 'they're giving up' which is not what he said, as sadly coronavirus globally does defy containment efforts.

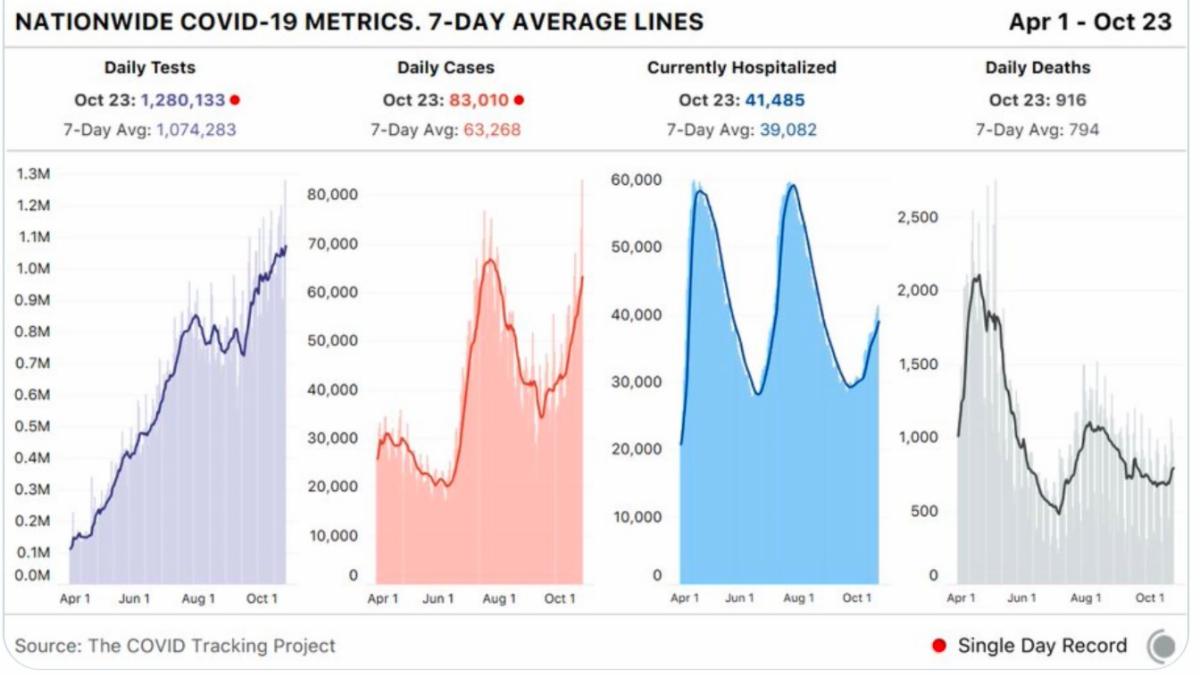

- Regardless, lack of control, whether trying or not, leaves uncontained rise of cases and hospitalizations, and that's a real-world worry markets note, even though things like mortality data are challenged once again (hoping they are lower and not about to surge in the weeks ahead).

- Clearly clarifying what Chief of Staff Meadows 'actually said' doesn't get into the debate about how everything was handled (isn't intended too).

- (Hard to thread the needle of COVID being politicized), but regardless this week involves not just COVID fatigue, not just regulatory risks next year, but angina rising beyond the 2020 Vote (much is behind already given the historic levels of early and mail-in voting).

- To the concerns out there, it's fear of uncertainty in the wake of elections too, both legally and conceivably in-term of public disruptions, and while that's possibly a factor in current moods, civility is tough to diagnose.

- Super-cap-led (mostly tech) break is a jarring event pending for awhile, and as I'll note momentarily, I suspect the SAP story was misinterpreted.

- S&P (SPY) and Nasdaq (QQQ) primarily hit by liquidation of those FANG types we warned of for weeks, so while some of the backdrop is unfortunate, what more can one say other than some sort of shakeout like this was coming.

- Exponential growth in COVID cases without meaningful containment in many areas (here and abroad) is suppressive and concerning.

- Election uncertainty and COVID-fatigue combined to allow this purge.

- IF Biden wins, the Democrats are believed 'coming for' big technology, if so it's problematic even if targeted stimulus is a plus for smaller firms.

- This focus on smaller rather than larger business is part of our outlook, to some degree that's bipartisan because of scrutiny of antitrust aspects with some bipartisan support.

- If it's not clear, multiple compression is still likely on almost any Election outcome, as relates to the FANG-type super-caps, not the broader list.

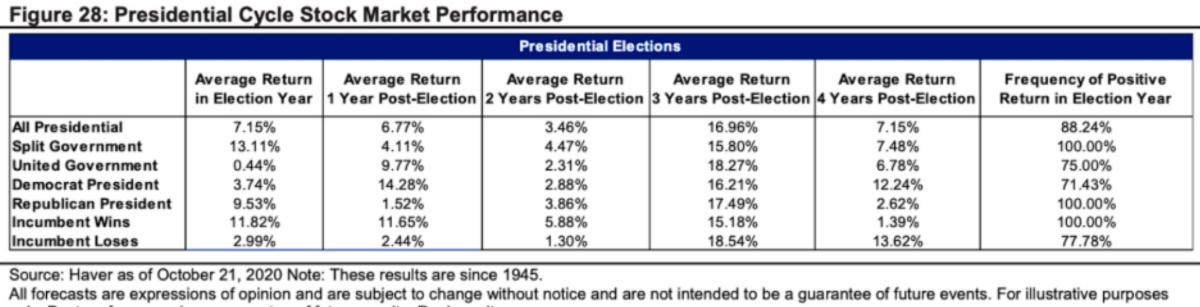

- A decisive victory by either candidate would bring a sigh-of-relief just as the clarity alone would allow Stimulus for optimistic economic recovery.

- Obviously we don't know that a decisive Election would clear-the-paths, but I suspect if we don't have Stimulus sooner it would.

- What it will also clear, is whether or not to expect more Capital Gains or long-term pressures, which would be more likely should Biden win.

- Pressures (or surges) in sectors, will vary in this Election cycle as well, while biotech will depend very much on approvals, rejections, funding, and other aspects on this key area during the perpetual pandemic.

- Lots of 50-Day Moving Averages came out and that accelerated selling technically, but this is more sort of 'prioritizing' reality over politics, that technical washout should lead to a rebound even if lower later.

- A quick uncontested Election (either ticket by a landslide) would, from the stock market's perspective, be the best way to proceed, that's especially because there's a segment of the population that might not accept the winner on any relatively narrow outcome.

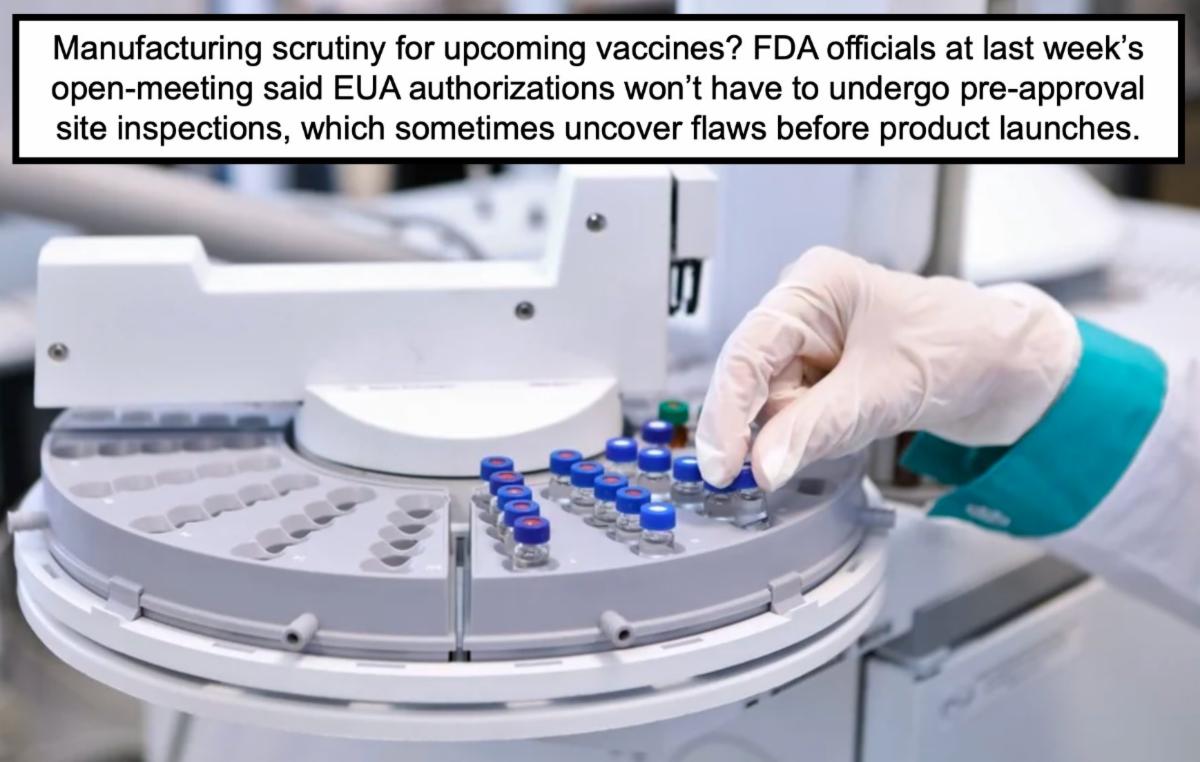

- It's basically wishful thinking to expect a breakthrough vaccine or drug of known efficacy suddenly emerging, but favorable news of a therapeutic or similar trial would likely spark a rally from any level, and if it's rapid testing simplified, more likely a modest overall rally aside for the stock involved.

- Again not expressing bias, just believing that markets will be choppy or have a tendency to trend lower overall until clarity prevails, uncertainty of this magnitude is anathema to market stability and challenges strategies.

- Regeneron (REGN) can't readily mass-produce their MAB (monoclonal antibody as we now call MAB), Lilly's trial of theirs is halted for now, as Sorrento (SRNE) is pending possibly early results from Brazil or perhaps Philadelphia.

- NIH sees no benefit of therapy with the Lilly (LLY) MAB in hospitalized patients but it may be helpful in earlier stage patients, interesting in-that Sorrento is trialing it initially in sicker hospitalized patients .. gets very interesting if Sorrento's works and the others don't do much or are too hard to make, a couple more bearish views on Sorrento are out there, without any basis, while it seems stock offered for sale is readily absorbed, speculative.

- Trends toward online gambling 'might' indicate it's a long time before Las Vegas recovers, hence Adelson's move to sell the properties (?), hard to say given his age so possible desires beyond Las Vegas Sands (LVS) price.

- One more thing: Release 16 of 5G (for networks), supports integrated access and backhaul, meaning that telecom operators can add mmWave base stations without need to run a cable to a cell site, just electricity.

- Instead, they can use wireless frequencies to provide both consumer and network backhaul (and essentially 'fronthaul'), which should cut both time and costs of rolling out more stations and help boost existing coverage.

- We don't know exactly who customers are, but little Cerragon (CRNT) (the Israeli typically boring stock) happens to offer just that wireless capability, they have Vodaphone India (VODPF) as their largest customer, but have something with both T-Mobile (TMUS) and AT&T (T) in the U.S. and/or Latin America.

- IF we emerge from a decisive Election, get COVID 'relief' (stimulus, plus medical solutions), then the market's 'reflation trade' rapidly finds a path to resume, so maybe the rhetoric will calm down a bit too.

|

|