|

Executive summary:

- One member called this a paper-mache market, a good way to describe what for months I've termed an internally-correcting declined 'masked' by the big-cap (FANG type) stocks, as gave an illusion of market strength.

- That's also why I've suggested again for weeks, a serious correction for S&P, but not so much for those sectors already eroding for months.

- So now it all collides with the already anxious pre-Election market, delusional denials about the situation by some, overly negative prospects by others, and in-reality a market that is catching-down with reality.

- It's all about 'tech' to a degree, because that's what drove the market. .

- My intention is to shorten these significantly ahead, as we do navigate unprecedented backdrops of politics and COVID as best we can.

- A solution to COVID amidst a contested Election drawn-out for a long time would probably be the worst case for the S&P to envision ahead, I doubt we'll get that combination however.

- The 'safety-net' has been withdrawn surrounding COVID stimulus, while it is obvious that business is taking, and will continue to take, a serious hit, in-part not 'cushioned' by funding to help business and people survive.

- It's the collision of COVID stimulus inaction, along with spreading disease, that transcends the market's already-anxious mood around 'politics'.

- Without the support for small business, any Fed action won't help either, which is my point about how negative rates in Europe weren't relevant.

- And big companies have been able to sustain because the majority of a pandemic lifestyle is deeply involved with big-cap stocks, not local shops.

- In Europe the focus is much more on family and small businesses, hence you have different types of public protests against lockdowns, from these small businesses and their workers.

- That's a slightly different social issue vs. here, where we have mobilized cities now to contend with rooters and riots, not peaceful protest marches increasingly, and states like Texas calling-out the Guard for Elections.

- Dynamics here reflect a lot of companies that were beneficiaries of COVID, and without stimulus (or believing business retreats without stimulus), lots of those companies are also feeling pressure.

- S&P and big-tech: for now sideways at best, lower at worst, based on the October narrative we have anticipated the market would be dealing with.

- Bounces will be sensitive however to news developments on COVID more than politics, and of course post-Election stimulus would smooth things.

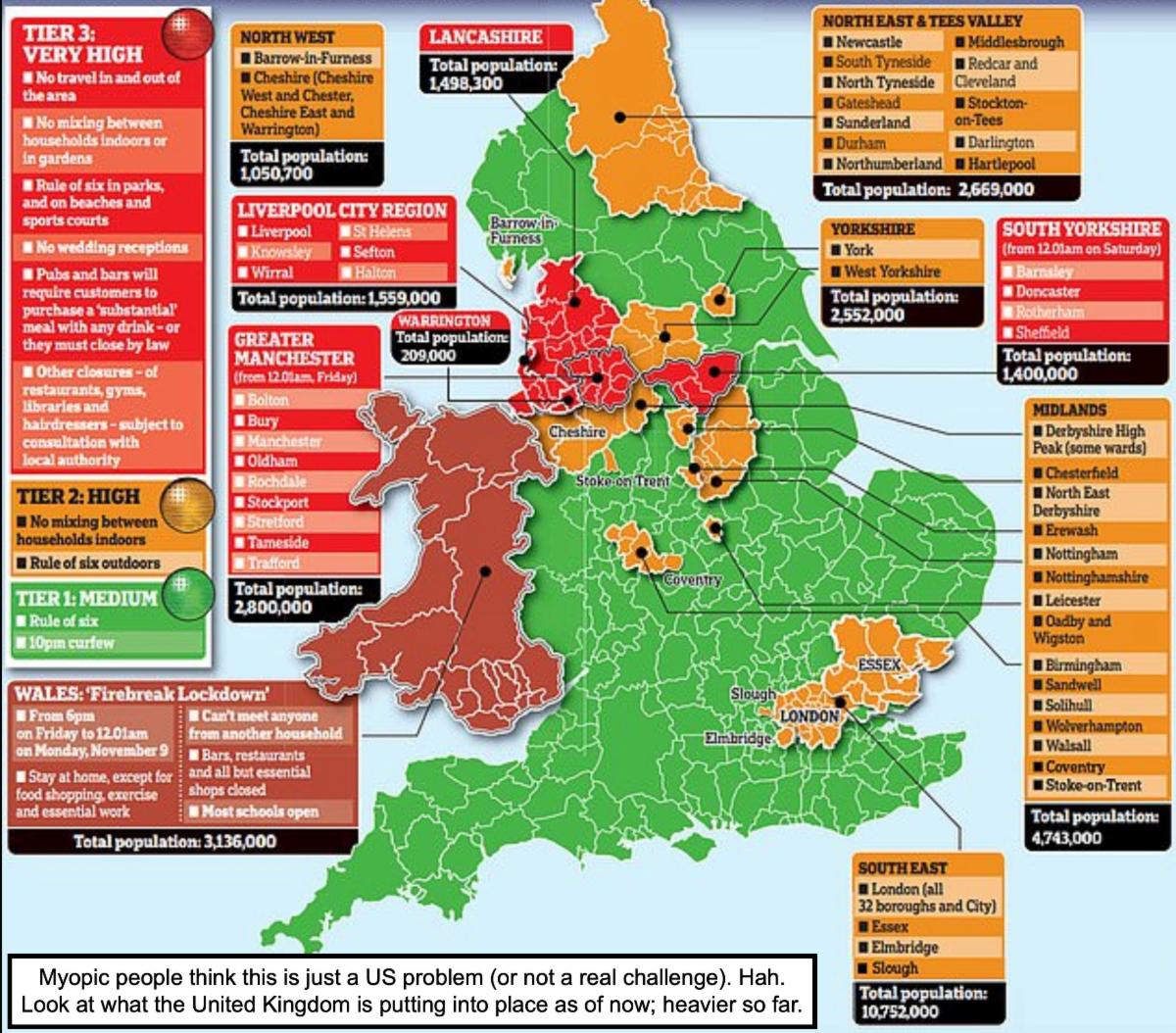

- As to COVID, while there are variations in resurgence in some states, that in-itself is not going to negate need for sensible measures, even while the draconian measures (such as New York State's) may go a bit too far.

- I'm actually thinking there is a spike of COVID in New Jersey so anyone in New York who thinks they've dodged this are mistaken.

- For now, even if we get stimulus and favorable Fed action, a look at how negative rates have 'not' helped Europe, show that this is more about the evolution (or solution) for the virus, not merely monetary or fiscal policy.

- We have learned about to have something of a more-normal life dealing with the virus, but despite U.S. resilience it's a pretty dire global picture.

- If a serious resurgence occurs in Asia, global despair will deepen.

- Statistically probable market outcomes don't work so well when metrics are dramatically offset.

- Yes we're optimistic further-out, this is not a change of what we've already said, simply being realistic about where fundamentals are and 'risk' levels.

- In this environment most investors are potential 'buyers in the closet', with no desire to venture-in significantly until they see 'other-side' visibility.

- Other-side visibility on COVID 'and/or' politics can be clouded by tax-sales that have already occurred or vary depending on the vote's outcome.

- From the political side, the worst-case would be a dragged-out process which even ends-up in the Courts (aka: Bush vs. Gore years ago).

- Civil strife is a concern, that's what Philadelphia shows, and what Texas National Guard mobilization (minimized in the media) already fears.

- What is sad is overreach by States, California restricting limited opening of Disneyland (when Disneyworld was opened so responsibly if boringly), is economically depriving to Anaheim/Orange County, and excessive (DIS).

- The point is not 'living with the virus' or 'dying from the virus', but adjusting to a reasonable effort that keeps the core of the economic functioning in as many sectors as possible, clearly not so much tourism or travel.

- The prospect of Europe's new lockdowns should be sobering to all of our domestic myopic players who fail to grasp intertwined global economics.

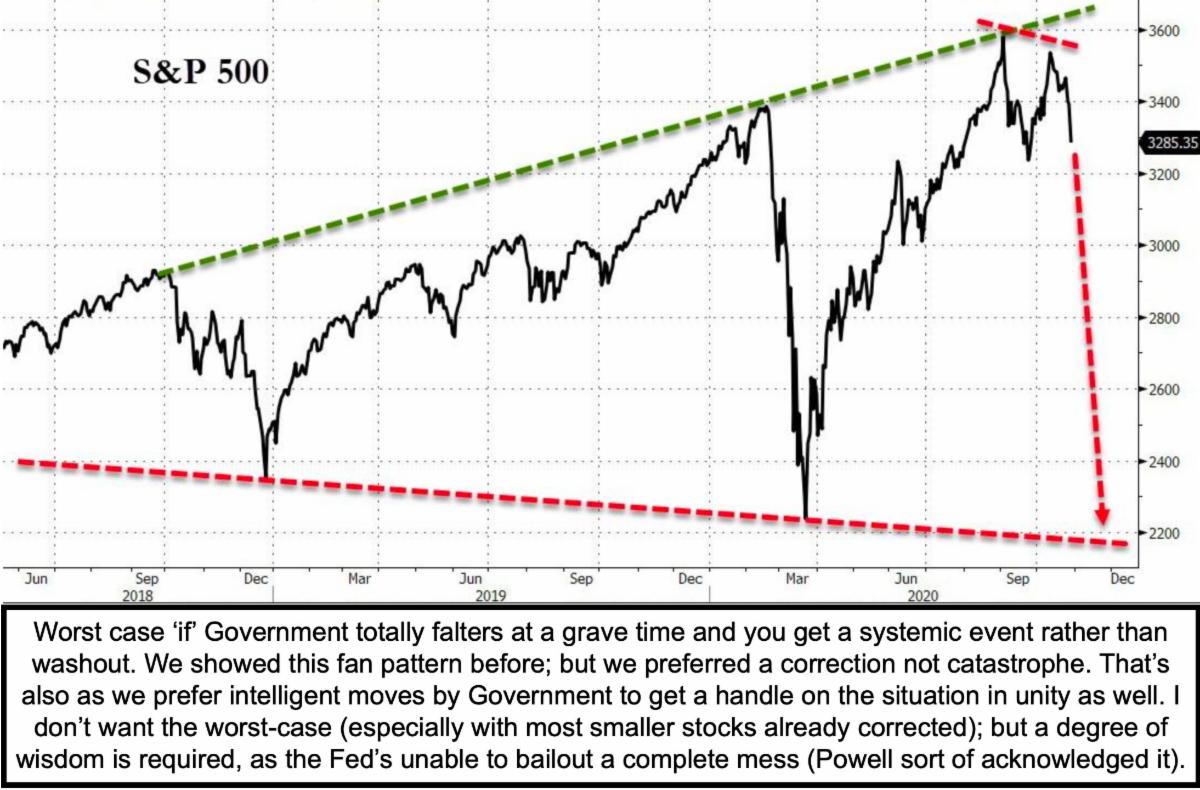

- It is all part of the same defensive pattern, related to technicals outlined already (break of S&P's 50-Day, rebound tries, and then likely lower), we envision a continuing evolving decline for now.

|

|