Market Briefing For Monday, June 13th

Deflationary sentiment amidst inflation is an odd characteristic of this Bear; and although everyone is told there's not an 'official' recession; it feels like it for vast numbers of people who have to contend with significantly higher costs of everything, even if their wages or income is stable or stronger.

I have commented for some time that we are already 'in' a recession; and that by the time it's officially confirmed; it will be about time to anticipate recovery. I see lots of value in the debris of the present market; but only suggest light nibbling (and not particularly in big techs or big caps in general); though value is being re-established by virtue of the purge.

However, as often noted, the S&P and NDX were priced for an era that ended some time ago; and that includes the global growth picture; which continues a contraction, not expansion. And that's even aside impacts from Russia's war.

Perhaps Defense Secretary Austin just today having his 1st conversation with his CCP (Mainland China) counterpart, and their sort of aggravated exchange according to sources, implies that by no means is the world really focused on economic well-being or growth, although it can be suggested they should be.

Meanwhile everything is knee-jerk reacting to numbers; they probably will also freak at a sharp increase in the Funds rate; and I understand the viewpoint of a Fed moving 100 basis points all at once, to 'get it over with'. Again; extreme.

And there is inflation in the pipeline anyway; not to mention the war's impact.. which of course has contributed to Oil and Food costs. More inflation coming still; but some areas are peaking; others will from 'demand destruction', and of course the big factor will be an end or at least a ceasefire in the Ukraine war.

In sum: economic conditions 'trail' this slide in financial conditions. Even data freaking everyone now is 'trailing'; although changes are, as noted yesterday, minimal (hence inflationary factors generally have not mitigated in key areas).

To wit: if we're going to have a more significant recession beyond that implied by the ongoing stagflation (in my view); companies will adjust, spend less and that is also why I suggested Housing and hiring will both be constrained.

This is a complicated situation and has been; with the Fed being tasked with a fairly impossible assignment: containing things beyond their realm. That gives us a risk debated by everyone, as to how much the FOMC hikes next week.

To that end, there are a number of economists and pundits calling for the Fed to 'hit inflation hard and get this over'; with typically a 1% Funds rate hike. So maybe we get 75 basis points. If so it shows hubris on the FOMC's part; since choking-off growth is not in-itself the entire solution; due to extraneous events that impacted prices, starting of course with Oil. And then later came the war.

There were few if any silver linings in Friday's inflation data; and because this geopolitical influence makes it so hard for the Fed to get 'in-front' of inflation if it's even possible; I question why so many (including current or former FOMC members) think they alone have the capability to contain this.

I have not thought there was much upside potential as we meander through a rough Summer (markets, weather, war and inflation). However I've thought at least the majority of additional vulnerability was (and is with interim bounces) in the mega-cap dominated S&P and NDX/QQQ. It's all a process and history also shows how markets (and policies) will wear investors out before turning in a sustainable way. Although today was headline-based and there's nothing showing-up yet that's dis-inflationary, and we've made that point before.

True that if the Fed doesn't hike solidly here they will have an even harder go of it; or at least that the general hawkish view. The Fed is impatient; so is the market's crowd calling for 'let's just get there' as for higher rates. Problem will be in Moscow, who must be laughing at all this; since Russia just 'cut' rates as they are making plenty of money from Oil sales (yes they are) and might just be moving ships to the Med to protect/escort tankers violating the sanctions.

Reality checks would suggest the equity arena eventually stabilizes and then rebounds generally about the time a textbook definition of 'recession' officially is provided. However, again that's traditional and this Bear is nontraditional. It's really well over a year old internally; bifurcated as I noted again via video.

A lot next week might depend on whether the Fed gives a pre-announcement (by front-loading the hikes) that suggests 75 or 100 rather than 50 bp coming next. Again, my concern is that we are already in stagflation and in-recession already (and have been) and the Fed can't readily fix this. But Putin could and he knows that. It's a disincentive for ceasefire negotiations; but it's truly evil as by continuing the brutality he also prolongs the suffering of third-world nations so dependent on Russia and Ukraine for food.

A broader risk this year still is 'pestilence, war and famine'. Sorry to wrap-it-up on a sour note; but isn't that what the equity market has been telegraphing for months? And if these global factors gel in a way that results in 'peak inflation' (concurrent with war resolution?); then you get the Fed reversing direction; Oil drops to only high supports (like the 80's); and the Fed realizes it's not entirely dependent on them.

When the war started I opined that we couldn't entirely or naively get through this without pain beyond the 'theater of action', and sadly that's the case. For the latter part of this year (and next), S&P's storm coming for sure has arrived and is buffeting stocks (and barely Housing... so far); with bounces that swing but can't yet change the outcome.

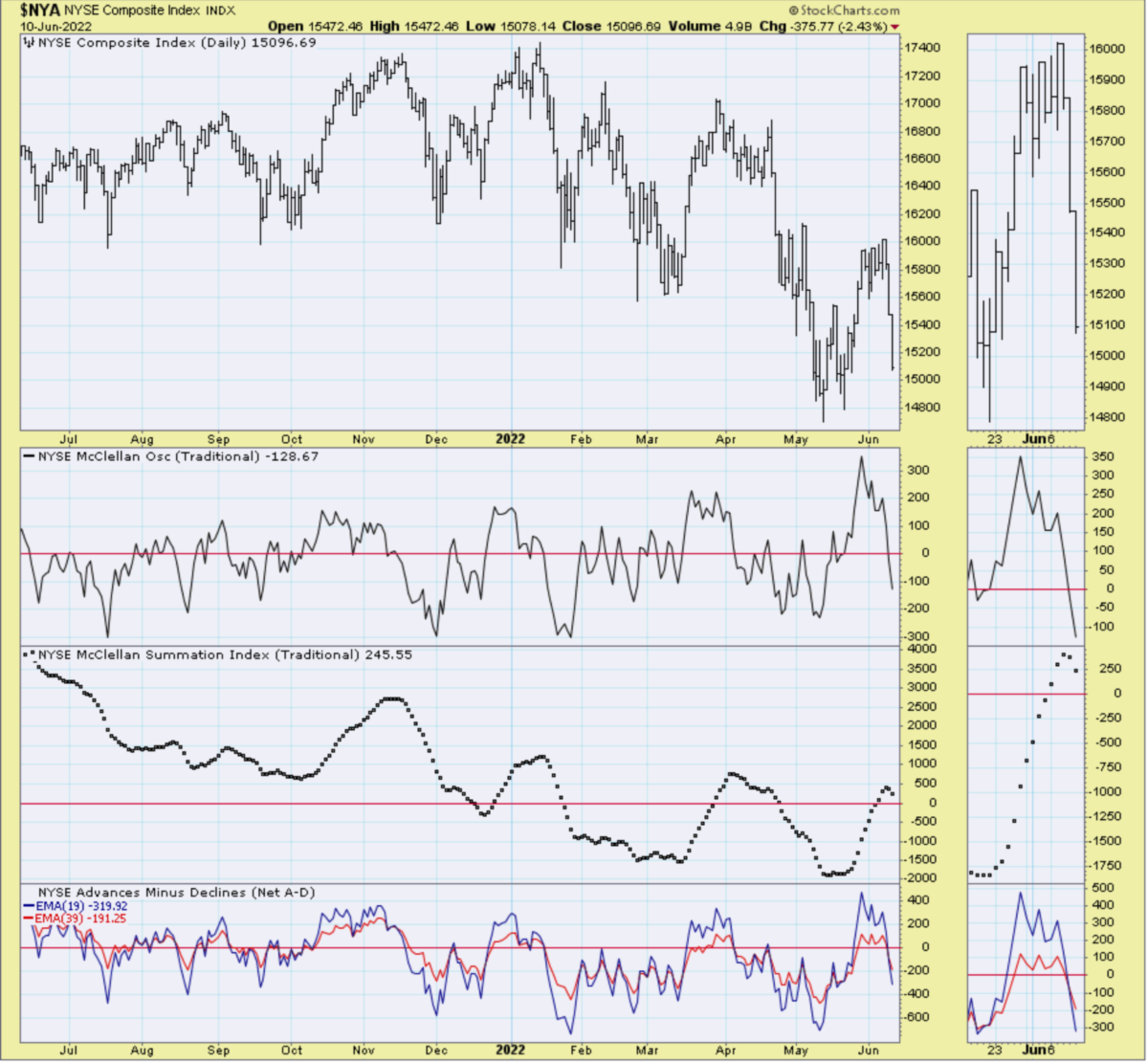

Note S&P has yet to break the recent lows; and as that occurs (especially on a solid FOMC hike) you likely washout again and set-up another bounce, but all within the process barring peace breaking out. Again; primarily watch Oil.

Bottom line: a perception is the Fed 'needs to do more'. And maybe that will appease market fears. But my concern is it breaks the economy, which really is hanging-on by a thread; primarily because of a tough macro 'core' inflation number, not ex 'food and energy' as that really dominates the rest of it.

Traders are fairly flat; didn't expect much of a recovery and didn't get one into the finale Friday. That's because it's not only a military weekend; but loads of apprehension about the upcoming FOMC meeting. Low unemployment rates give a different facade to this economy; but you have fewer willing to work for anything other than high pay (if they can't do so remotely); and you have cost of money notably higher as the high-yield market reveals; as does Fed QT.

Will the FOMC slam-on-the brakes big time? That's the question of the day of course; but oddly 'if' they do it's probably not going to change the global issue but might washout and trigger a rebound rally again; as some will perceive the drama as being just what the doctor ordered. (And it may induce more ulcers than it cures; because it won't impact the war; but will hurt business, Housing and general liquidity needs that ensue; as has already been suggested.)

This is an excerpt from Gene Inger's Daily Briefing, which typically includes one or two videos as well as more charts and analyses. You can subscribe for more