Market Briefing For May 14

Unintended consequences . . of Federal Reserve actions (or pressure on the Fed to venture into dangerous 'going Japanese' negative rate territory), all suggest something 'gone awry'. It would just affirm long-held opposition to 'negative rates', and impact on banks, lack of growth, and benefits only certain major companies, but not good for any but 'super-cap' and maybe utility stocks, or handful of others with superior sustainable dividends that.

Also credit becomes more difficult in such a backdrop, so neither banks nor business can actually operate well with NIRP.

This dominates much of debate about this market now, even though we've already seen in Japan and Europe how corrosive (not constructive) NIRP policies are. Yes it pushes the bond market, and yes TINA prevails (that is the 'there is no alternative' to stocks idea). But look at Japan and look at U.S. banks. The President pushing this should view empirical results. The weakness in Financials along with relative strength in Technology is not new, really throughout all the movements from the projected March lows to the April-May 'S&P peaking range', that indeed was expected to not result in further meaningful gains.

Many implications of the divergence noted, suggest problems persist going forward, but that Fed intervention is also why HYG hasn't collapsed further. Too many bears 'were' citing the bursting bond bubble and missed the rally entirely. We caught it, but our point throughout the past weeks distribution, has been that we get to a point that an S&P correction (hopefully not more) presents itself during parts of May, with risk varying depending on business opening (and the outcome of containing the logical increase in viral activity mostly everyone expects), drug progression, and oddly.. foreign fund flows that nobody talks about and I thought was a big part of pre-WuFlu gains.

Executive Summary (a few key points beyond most media):

- Late-breaking: Wisconsin Supreme Court overturned 'stay-at-home' state order, ruling it unlawful and unenforceable, the Governor slams the decision as a GOP power-grab "exploiting a global pandemic to undermine the will of the people", promises controversy elsewhere

- Fed Chairman Powell stating the obvious regarding further economic 'support' being needed, is blamed for decline, reality is he's reflecting a point made throughout this drama, after 2-3 months of time bought, it becomes a financial (not just biological) crisis after that (without drugs proven effective, until we get to a vaccine later-on)

- Norway's Sovereign Wealth Fund (world's largest) is rumored about to dump up to 40 billion of equities on the market, another warning, but is not necessarily something other than chatter (unless or until)

- Prohibition of a U.S. fund buying Chinese securities may be logical of course, however a quid-pro-quo retribution risk as 'their' response by increasing liquidation of American assets (would loom as tit-for-tat)

- Domestic concerns about 'disease' trends are becoming alarmist and that's even when there is nothing happening that's unanticipated (aside the situation of the inflammatory disease attacking children), as with a continued variably-high infection rate, there's a clear demographic as well as perhaps appalling trade-off debate (lives vs. economy)

- It's the possible uptick (not yet) in hospitalizations and/or deaths that's a more adequate track of how Covid is trending, as increased testing 'of course' results in higher 'case numbers', alone reveals too little

- Speaking of testing; it turns out (though they deny it); that the Abbott (ABT) test (being used at The White House) has little better than 50/50 odds of being accurate (ridiculous for approved tests), also means VP Pence and President Trump may or may not be 'really' negative on any given day (this is being widely reported, but worth noting)

- Tomorrow pushed-out BARDA Director Bright warns of 'darkest Winter' ahead if we don't get an effective therapeutic and/or vaccine, I concur, which is both why I've said speed is of the essence, and really expect a worthy therapeutic before Fall (and the school year for most?)

- NOT widely reported (if at all) is a geopolitical stunner, although most of my generation already suspected this: Saudi coordination between their Washington Embassy and the hijackers in Los Angeles (you may recall years ago I mentioned the FBI determined their Ambassador to the US had funded one of the flight school terrorist's tuition, and from his personal bank account no less), so what's new there

- New: the FBI inadvertently released (had tried keeping it out of filings to 9/11 survivor litigants against Saudi government officials) names linked to specifically hijackers of Flight 77 flown into the Pentagon (a friend was (Lt. Cmdr. USNR) Captain Burlingame, AA Capt. of Flt. 77)

- This creates a new challenge for Washington's always-suspicious ties to the Saudi's, ergo, did Saudi Arabia attack the USA, then over time manipulate the US to attack Saudi enemies in the Middle East(?), not sure about the extent, but implications could be significant (no wonder: it may have been confronted already, and hence arms or investment deals resulted... but I'm glad the Victim Survivor investigative team found this, and have thought the Saudi leadership culpable all along)

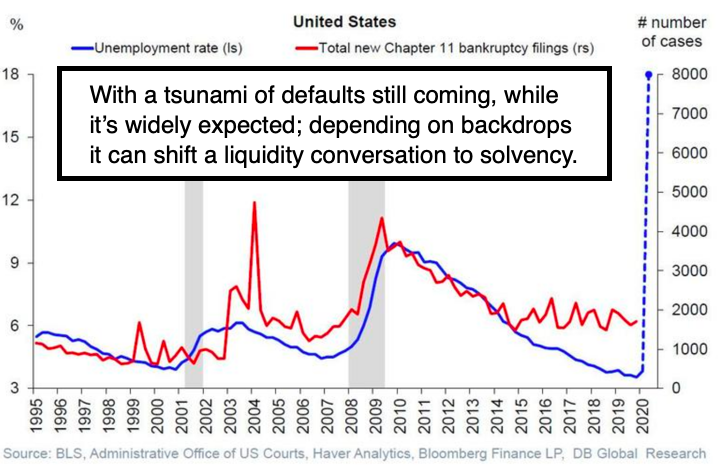

- Commercial Real Estate continues to implode as forewarned long ago, and over time this can become part of the impetus (any time really) as everyone is aware but few focus on threat posed from nonperforming loans and the tsunami of defaults and bankruptcies poised to hit (I'm thinking the Federal efforts just kept zombie businesses afloat in-part, rather than reinforcing the bankruptcy processes which some will find themselves in regardless, and I'm thinking travel and tourism too)

Meanwhile . . in the short-run, the cyclical and 'old' consumer discretionary stocks were missing elements as secular growth names were continuously relied-on for the 'heavy lifting' by the S&P, NASDAQ and of course NDX. If we get some 'life' in the economically sensitive suppressed stocks (energy and Oil for-instance), not to mention Banks (which remain totally dormant), there's an argument for upside of note (down the road), otherwise (for now) it's increasingly a tough proposition to envision meaningfully higher prices.

What's good news is those that have the least trouble recovering earnings, after this corrective phase; as some aren't rock-solid as analysts believe. Also, consumer demand are essential components that can roil that 'growth argument', if a broad cross-section of the population is unable to spend, as we're on the edge of that or really already there (higher savings rates too).

That's part of the disconnect of how the Fed Put helped levitate the leaders as well the (sort of snobbish) ignoring of what happens if you don't get such broad recovery in the general population, so that they indeed 'can' spend.

I also had this feeling (data supports it) that technology was increasingly fully-priced, supporting my idea they were heavy-lifting leaders and should face contraction before moving higher 'later on'. So pretty negative with the exception of a handful of specialty stocks just now starting to benefit from the 'new normal' in the ongoing and the post-Covid world.