Labor Market Tightness

The interesting part of the inflation debate is the question of labor market tightness. If we are looking at the CPI, what we see is that many components hit high rates of inflation. This means that we need similar gains in 2022 to keep the CPI from dropping back towards 2% or whatever. The more interesting issue is whether strong wage gains will continue, as that increased purchasing power would give a lift to demand and increase purchasing power across all sectors.

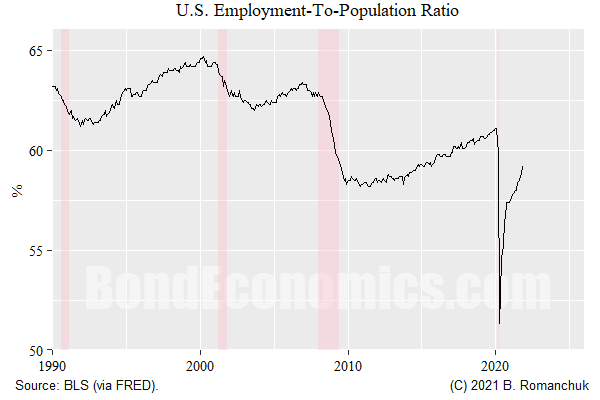

The latest U.S. labor market data dump was consistent with continued improvement in the labor market, with the broad employment-to-population ratio rising to 59.2% (figure above). That is well above the lows and returned to the values seen in the middle of the last cycle.

My not very useful observation is that hourly earnings is perkier than would be justified by historical rules of thumb based on macro data. Potential explanations appear to be as follows.

- One explanation I have seen is that wage growth may be more sensitive to the rate of job creation, rather than levels, as is conventionally assumed. (I saw the analysis on the EmployAmerica website, but I cannot remember which blog/report contained it.) Since a good portion of job gains are firms getting back to work after shutdowns, employment growth rates will presumably burn out relatively soon.

- Policies that paid people not to work obviously help tilt bargaining power towards workers. I am unsure as to how much of this effect remains.

- Have workers dropped out of the workforce due to health concerns? This is the story being pushed by the hawks. It is unclear to me how sustainable such a strategy is for workers.

- On a related point, day care employment has not fully recovered, and so workers are effectively locked out of the job market.

- The changing consumption patterns of consumers has invalidated certain modes of operation for firms. So firms could theoretically have the same number of employees, yet need a different mix of workers. This would cause “skills bottlenecks,” even in the absence of net employment growth.

- Certain firms and industries feasted on unsustainable labor practices — being able to call in workers effectively on demand, for example. Even a slight amount of labor market tightening would squeeze out such practices. Meanwhile, there are industries reliant upon pushing capital expenditures to “contractors”: trucking and ride-sharing. Sooner or later, the supply of suckers who don’t understand depreciation would dry up.

Projecting high wage growth on a multi-year horizon appears to be reliant on the premise that firms and workers cannot adapt to the realities of a world with COVID-19.

Peak Oil

One of the other issues with the inflation outlook is the question of oil prices. At the moment, wholesale energy prices have undergone a correction, which will blow a hole in the rate-of-change of the energy component of the CPI. On a longer horizon, we might need to be cautious.

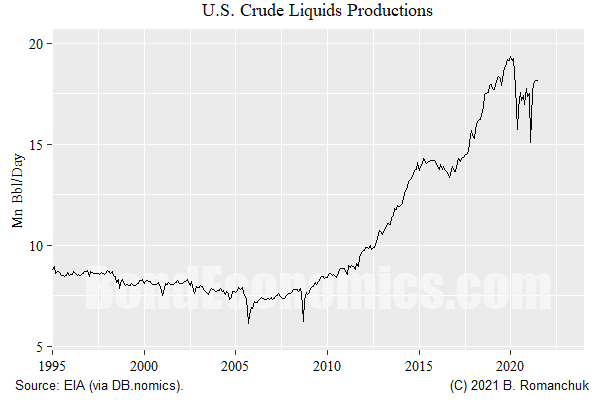

As seen in the chart above, “liquid” production has peaked in the United States (right about when one of the more reliable contrary indicators on Twitter was laughing about Peak Oil). This was somewhat predictable: fracking generates output quickly, but the depletion rate is also rapid. The industry was unable to keep up the frenetic pace of drilling since it was not economic.

Admittedly, high oil prices could generate another burst of fracking activity. However, the reality is that the fracking needs to move towards more marginal sites, and depletion gets worse as conventional oil production continues its secular decline.

There are of course other sources of hydrocarbons. However, the United States was the epicentre of fracking triumphalism, and the most that oil production bulls can hope for is that the same script plays out elsewhere (horrifying anyone worried about climate change).

Disclaimer: This article contains general discussions of economic and financial market trends for a general audience. These are not investment recommendations tailored to the particular needs of an ...

more