Friday, September 17, 2021 9:00 PM EDT

Key policy rate decisions in the US, Sweden, Norway, and Switzerland dominate this week’s calendar. Most developed markets are expected to hold off on any tightening until long-term inflation figures are significantly higher.

Source: Shutterstock

US: Federal funds target rate to remain the same

This coming week’s highlight will be the Federal Reserve monetary policy decision. A no change decision is widely expected with asset purchases maintained at $120bn per month despite decent activity data and elevated inflation readings that are currently running at double the Fed’s 2% target. Instead, the Fed is likely to retain a cautious stance with the resurgence of Covid a clear concern while Fed Chair Jerome Powell has made it clear he wants to see more progress on the employment aspect of their mandate.

At the Jackson Hole Symposium he argued that “we have much ground to cover to reach maximum employment” and with August payrolls clearly disappointing (235k versus the 733k consensus) he is going to be minded to delay the taper decision until there is better news. We think this announcement will come in November, but for now the most we can expect is cautious optimism with a bit more explicit support for tapering this year. Nonetheless, it should be emphasised that this decision is completely separate from any decision to hike rates – there is no automatic path to higher interest rates.

New forecasts will show a slight growth downward revision with an upward inflation revision. The big story could be the Fed individual dot forecasts for interest rate increases. Currently 7 out of 18 officials are going for 2022 as the starting point for increases and we could conceivably see one or two more bring their forecast forward to 2022. We suspect the median stays at 2023 for now, but it will be a close call.

The data calendar is centred on housing figures, which are set to stabilise after a slight pick-up in mortgage approvals for home purchases in recent weeks.

In Canada, the Federal election results will be of huge significance. Prime Minister Justin Trudeau called a snap election in order to try and take advantage of strong poll numbers and gain an outright majority in parliament. However, things do not appear to be going to plan with Trudeau’s Liberal Party now neck-and-neck in opinion polls with the opposition Conservatives. This means that the New Democratic party could hold the balance of power, which would imply a higher chance of increased taxes and spending.

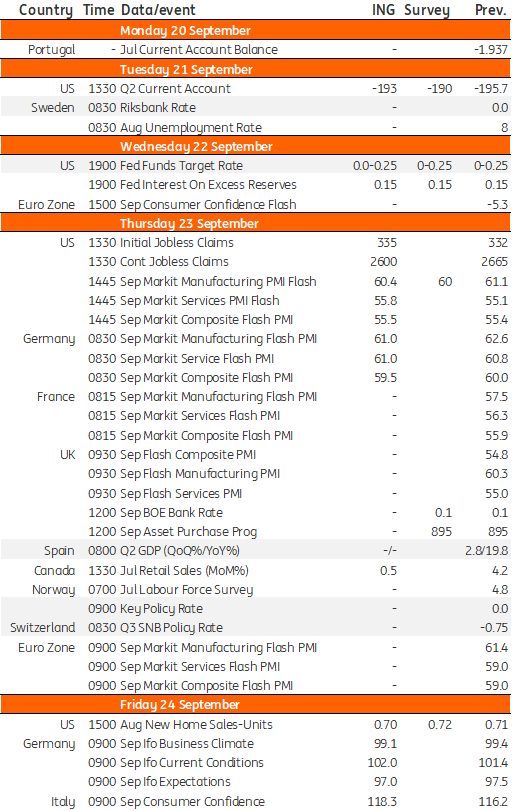

Developed Markets Economic Calendar

Source: Refinitiv, ING, *GMT

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.