Investors Dilemma: Pavlov’s Dogs & The Ringing Of The Bell

Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g. food) is paired with a previously neutral stimulus (e.g. a bell). What Pavlov discovered is that when the neutral stimulus was introduced, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.

What does this have to do with investing. Let’s start with a tweet I got recently in response to the article “Fed Trapped In A Rate Cutting Box.”

This is a great example of “classical conditioning” with respect to investing.

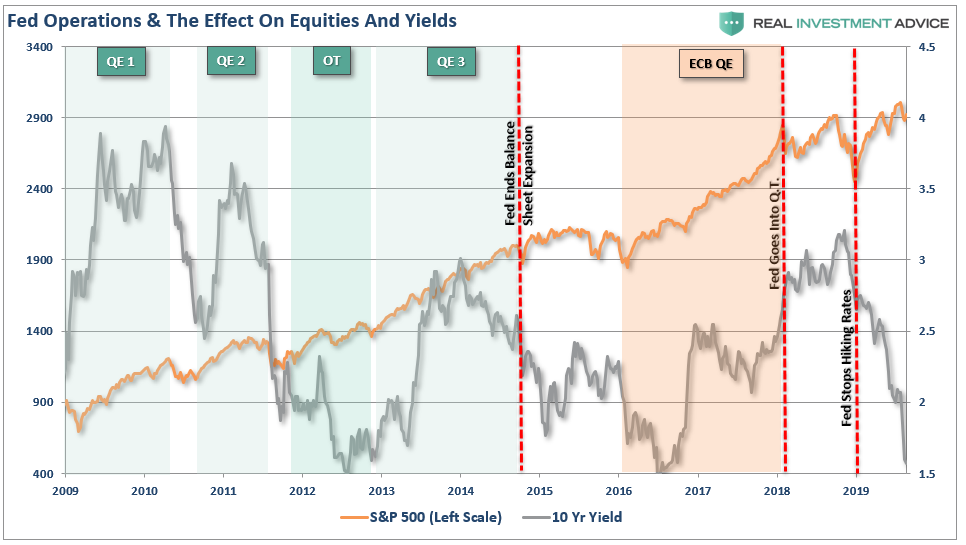

In 2010, then Fed Chairman Ben Bernanke introduced the “neutral stimulus” to the financial markets by adding a “third mandate” to the Fed’s responsibilities – the creation of the “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

– Ben Bernanke, Washington Post Op-Ed, November, 2010.

Importantly, for conditioning to work, the “neutral stimulus,” when introduced, must be followed by the “potent stimulus,” for the “pairing” to be completed. For investors, as each round of “Quantitative Easing” was introduced, the “neutral stimulus,” the stock market rose, the “potent stimulus.”

More than 10-years, and 300% gains later, the “pairing” has been completed.

The brutal lessons taught to investors in 2008, the last time the Fed cut rates, has been replaced by the “salivary response” to the “Fed ringing the bell.”

“Markets, as would be expected, tend to rally after rate cuts, because those policy actions translate into lower borrowing costs for individuals and corporations and tend to support higher moves for stocks.” – MarketWatch

Not surprisingly, the markets jumped on Monday and Wednesday as Trump, and the Fed once again rang “Pavlov’s bell.”

.....The Fed Rate, over a fairly short period of time, should be reduced by at least 100 basis points, with perhaps some quantitative easing as well. If that happened, our Economy would be even better, and the World Economy would be greatly and quickly enhanced-good for everyone!

— Donald J. Trump (@realDonaldTrump) August 19, 2019

Ring the bell. Investors salivate with anticipation.

However, let’s review why the Fed is implementing “emergency measures.”

In 2010, when Bernanke made his now-famous statement, the economy was on the brink of potentially slipping back into recession. The Fed’s goal was simple, ignite investors “animal spirits.”

“Animal spirits” came from the Latin term “spiritus animalis” which means the breath that awakens the human mind. Its use can be traced back as far as 300BC where the term was used in human anatomy and physiology in medicine. It referred to the fluid or spirit, that was responsible for sensory activities and nerves in the brain. Besides the technical meaning in medicine, animal spirits were also used in literary culture and referred to states of physical courage, gaiety, and exuberance.

It’s modern usage came about in John Maynard Keynes’ 1936 publication, “The General Theory of Employment, Interest, and Money,” wherein he used the term to describe the human emotions driving consumer confidence. Ultimately, the “breath that awakens the human mind,” was adopted by the financial markets to describe the psychological factors which drive investors to take action in the financial markets.

The 2008 financial crisis revived the interest in the role that “animal spirits” could play in both the economy and the financial markets. The Federal Reserve, then under the direction of Ben Bernanke, believed it to be necessary to inject liquidity into the financial system to lift asset prices to “revive” the confidence of consumers. The result of which would evolve into a self-sustaining environment of economic growth.

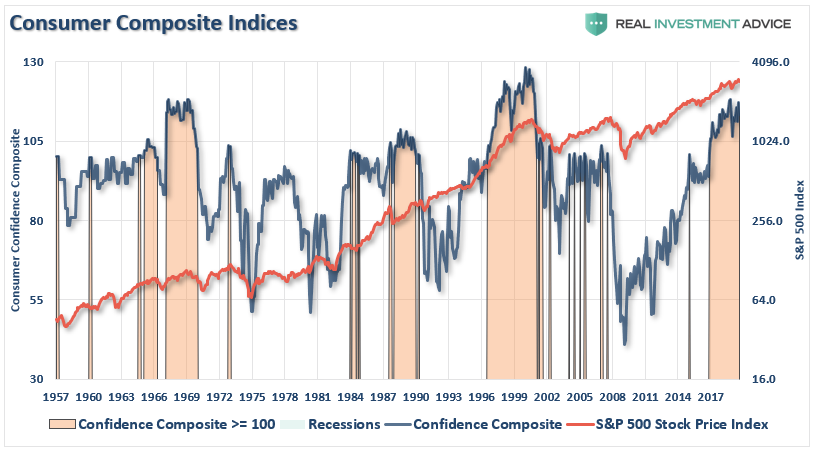

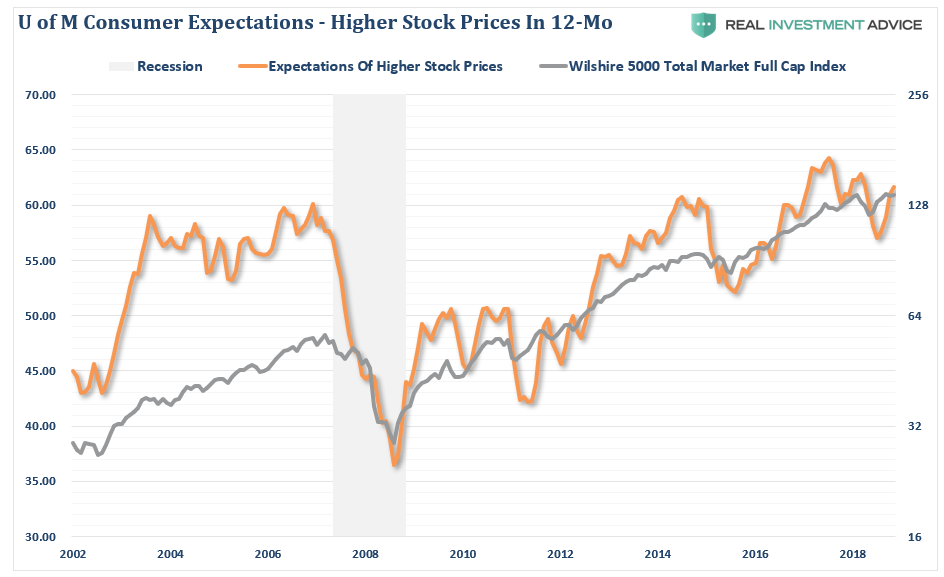

“Bernanke & Co.” were indeed successful in fostering a massive lift to equity prices which, in turn, did correspond to a lift in the confidence of consumers. (The chart below shows the composite index of both the University of Michigan and Conference Board surveys. Shaded areas are when the index is above 100)

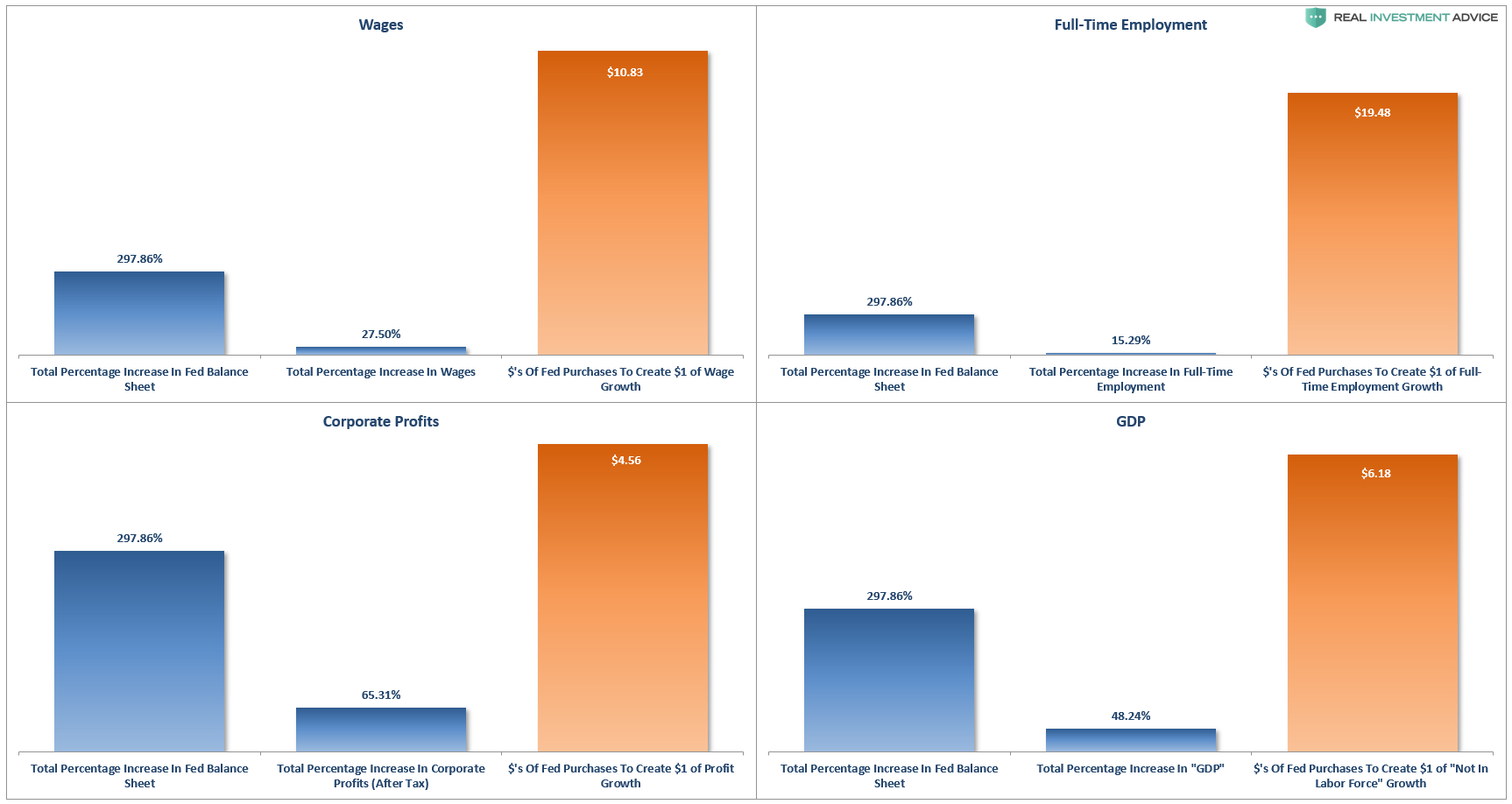

Unfortunately, despite the massive expansion of the Fed’s balance sheet and the surge in asset prices, there was relatively little translation into wages, full-time employment, or corporate profits after tax, which ultimately triggered very little economic growth.

The problem is the “transmission system” of monetary policy collapsed following the financial crisis.

Instead of the liquidity flowing through the system, it remained bottled up within institutions, and the ultra-wealthy, who had “investible wealth.” However, those programs failed to deliver a boost to the bottom 90% of American’s who continue to live paycheck-to-paycheck.

The failure of the flush of liquidity to translate into economic growth can be seen in the chart below. While the stock market returned in excess of 100% since the 2007 peak, that increase in asset prices was nearly 5x the growth in real GDP, and roughly 3x the growth in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not as subject to manipulation.)

Given that asset prices should be a reflection of economic and revenue growth, the deviation is evidence of a more systemic problem.

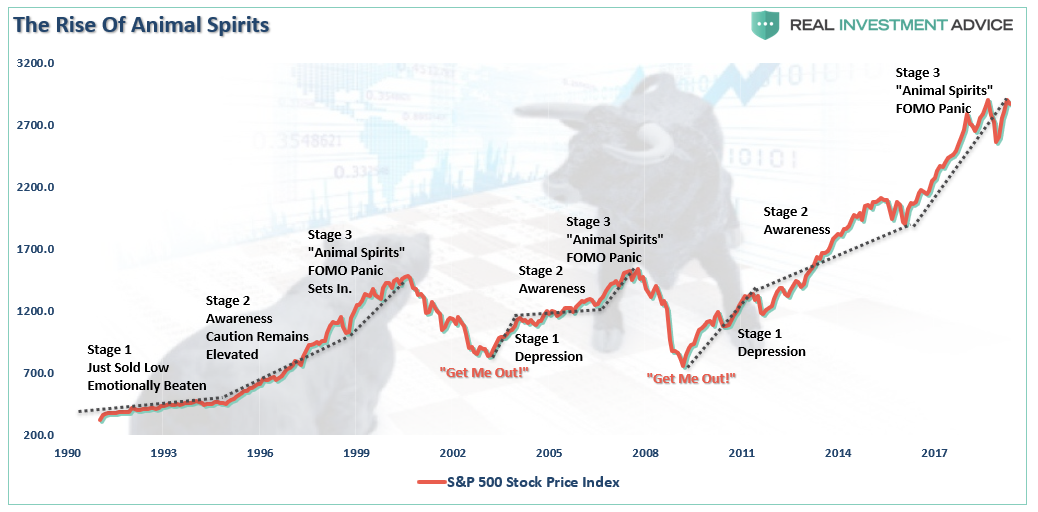

The Ringing Of The Bell

In reality, “Animal Spirits” is simply another name for “Irrational Exuberance.” The chart below shows the stages of the previous bull markets and the inflection points of the appearance of “Animal Spirits.”

Not surprisingly, the appearance of “animal spirits” has always coincided with the latter stages of a bull market advance and is always coupled with overvaluation, high levels of complacency, and high levels of equity ownership.

There is a difference this time.

There is an old Wall Street adage:

“No one rings the bell at the top.”

Consider this. What if the “bell” that is ringing isn’t the Fed’s “Q.E. bell?”

As I noted last week, the Fed is cutting interest rates as concerns over economic growth are rising. The push to cut rates is also occurring at a time when the yield curve is “inverted.” Historically speaking, this is the “bell ringing at the top.”

Interestingly, instead of investors being concerned about the level of “equity risk” they are currently exposed to, they are instead “salivating” at the possibility of more “neutral stimulus” (QE and lower rates.)

This is an interesting conundrum for investors.

The “ringing of the bell” over the last decade has trained investors to rush into equity-related risk. However, as I noted previously, the economic and fundamental backdrop is vastly different today than what it was then.

Again, what if the “the bell” investors are hearing isn’t the one they think it is?

As David Einhorn once stated:

“There was no catalyst that we knew of that burst the dot-com bubble in March 2000, and we don’t have a particular catalyst in mind here. That said, the top will be the top, and it’s hard to predict when it will happen.”

This is a crucially important point.

Currently, investors are as hopeful about the future of the equity market as they have ever been.

Why shouldn’t they be with the S&P 500 within a few percentage points of all-time highs?

However, once you start looking beyond the “mega-cap driven” S&P 500 index, a more worrisome picture emerges. Small and Mid-Capitalization stocks are significantly off their peak. Since small and mid-cap companies are more affected by changes in the domestic economy (and aren’t big stock repurchasers)such suggests there is cause for concern.

The same holds for rest of the world as well.

Besides the stock market, economically sensitive commodities also have a tendency to signal changes to the overall trend of the economy given their direct input into both the production and demand sides of the economic equation.

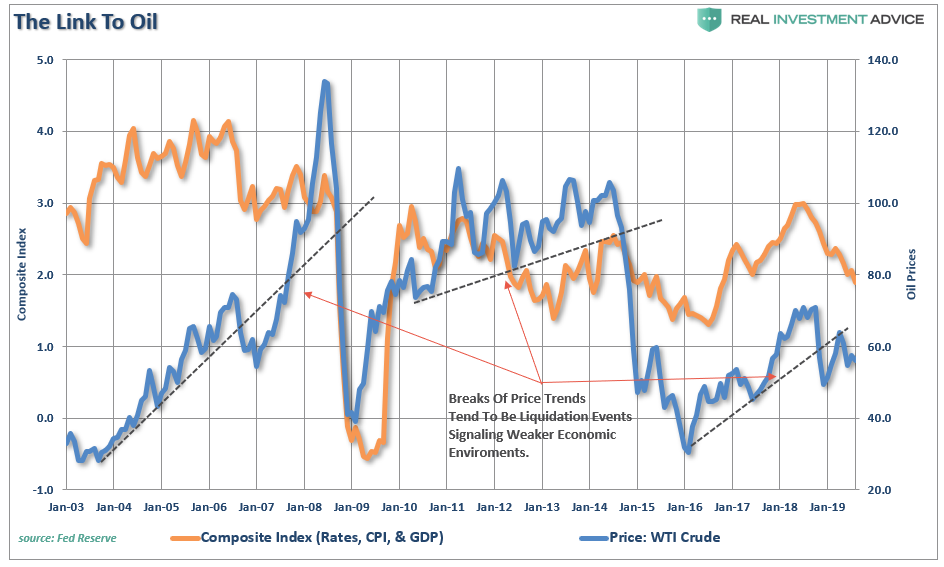

Oil is a highly sensitive indicator relative to the expansion or contraction of the economy. Given that oil is consumed in virtually every aspect of our lives, from the food we eat to the products and services we buy, the demand side of the equation is a tell-tale sign of economic strength or weakness. The chart below shows oil prices relative to economic growth, inflation, and interest rates (combined into a composite index.)

One important note is that oil tends to trade along a well-defined trend until it doesn’t. Given that the oil industry is very manufacturing and production intensive, breaks of price trends tend to be liquidation events which have a negative impact on the manufacturing and CapEx spending inputs into the GDP calculation.

As such, it is not surprising that sharp declines in oil prices have been coincident with downturns in economic activity, a drop in inflation, and a subsequent decline in interest rates. The drop in oil prices is also confirming the message being sent by the broader market as well.

The rise in the dollar over the last several weeks already suggests that foreign capital is flowing into the U.S. dollar for safety as the rest of the globe slows. This will accelerate as global markets decline, and foreign capital seeks “safety” in U.S. Treasuries (the global storehouse for reserve currencies).

The surge in “negative rates” globally is another warning sign that something has broken economically. As the economy slips into the next recession, domestic interest rates will continue to fall as “safety” becomes the priority over returns.

From the equity perspective, this is a time to consider reducing risk.

The evidence continues to mount the “bell has been rung.”

It just isn’t the “bell” that most investors are salivating for.

Disclaimer: Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with more than $800 million under management. As a team of certified and ...

more