Hyperinflation Seldom Occurs But Can With Rapid Speed

A Wheelbarrow Of Money Can Be Worth Little

Life is full of facts we don't know or have simply forgotten. In a comment, a writer recently encouraged the curious to search "hyperinflation during the Weimar Republic." Some of what I discovered was surprising. Germany had come out of the first World War with most of its industrial power intact, the speed at which inflation suddenly destroyed the currency dovetails with some of my thoughts on currency trading today. It confirmed that inflation can stem from a growing lack of faith in a currency, or all currencies, rather than just a lack of available goods. As inflation takes root the goods available for sale often contracts as sellers retreat from the market awaiting higher prices which creates a self-feeding loop.

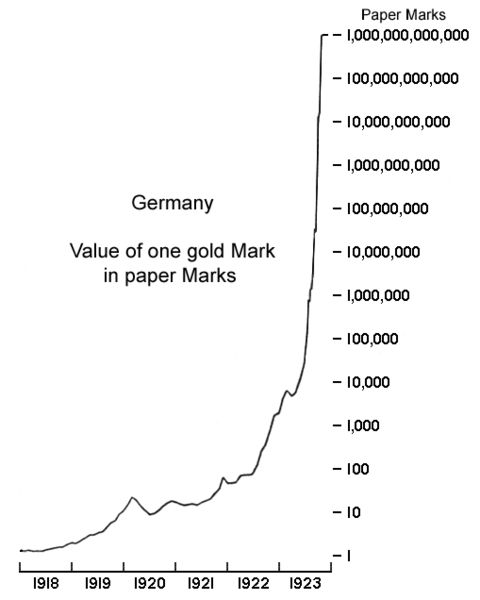

Hyperinflation Hit At A Startling Pace

It was amazing how quickly inflation took root in Germany during the 1920s, we must consider how fast it could happen now that we live in an age of instant communication. History shows the German currency was relatively stable at about 60 Marks per US Dollar during the first half of 1921. But the demands in May 1921 for reparations in gold or foreign currency to be paid in annual installments of 2 billion gold-marks plus 26 percent of the value of Germany's exports was crushing. The first payment was paid when due in June 1921. That was the beginning of an increasingly rapid devaluation of the Mark which fell by November 1921 to approximately 330 Marks per US Dollar. The total reparations demanded was 132 billion gold-marks which were far more than the total German gold and foreign exchange.

In August 1921, Germany began to buy foreign currency with Marks, this increased the decline, the lower the mark sank in international markets, the more marks were required to buy the foreign currency demanded by the Reparations Commission. During the first half of 1922, the Mark stabilized at about 320 Marks per Dollar because of international reparations conferences, including one organized by U.S. investment banker J. P. Morgan. After these meetings produced no workable solution, the inflation shifted to hyperinflation and the Mark fell to 8000 Marks per Dollar by December 1922. The cost of living index increased more than 15 times in just six months.

(Click on image to enlarge)

In today's world, many people have developed a false belief in financial stability because of claims by central bankers they have "controlled" inflation to where the economy will grow at a managed pace. A recent article on this site explored how the manageable inflation goal of 2%. has become the "holy-grail" of central bankers but this target central banks have deemed optimum is not economically valid and is "based only on their opinion" of what conditions will best allow the economy to flourish. For a long time, the ECB and other central banks have claimed deflation drives or allows their QE policy to remain and is central to their ability to stimulate. The moment inflation begins to take root and become solidly entrenched to where it becomes a self-feeding loop the flexibility of central bank policy is lost.

What makes this debate over future inflation very relevant is that the average American has witnessed in the last 30 years, a growing gap between government reporting of inflation, as measured by the consumer price index (CPI), and the actual cost of living. What the central bankers have conveniently brushed aside is that the formula that generates the numbers governments pump out was skewed in the 1990s when political Washington moved to change the nature of the CPI in an effort to reduce the federal deficit so nobody in Congress would have to register a vote that would harm the image of Social Security. For proof as to the real cost of inflation just look at the surging replacement cost resulting from recent storms and natural disasters. I contend that inflation would be much greater if more money had flowed into tangible goods rather than paper investments and promises over the last several decades and this has masked the rate central banks have debased our currency.

It might be wise not to become too trusting or complacent to the idea that inflation can be contained at 2% especially while deficits explode, debt builds, and central banks continue to stimulate the economy by printing money or that the economy looks good for the next year or so. In the past, I have put forth the theory that inflation could rule the day even if central banks are unable to keep the wheels on the bus and the economy suddenly collapses which is in truth beyond their control. If inflation does not become the flavor of the day it is also very possible the future may unleash, its sister, the powerful force known as stagflation.which is also a threat to the average citizen and will devastate those improperly invested for its arrival.

The mindset of investors and of the "money people" often shifts into overdrive when opportunities for speculation arise. The distortion caused by easy money from Federal Reserve policy coupled with political and social compassion for affordable housing, medical care, has obvious implications as debt and promises continue to rise. Most economists agree the Central Banks are not in a position to tighten the money supply at this time. Remember, so many of the things we invest in such as pensions and stocks are merely paper promises but hard assets are rare. A word of caution, while hyperinflation does not often occur, when it hits, and the speed at which it can hit is a massive game changer that can make bonds and many other investments nearly worthless.

-------

Note: This is the first of a two-part series, the next part will be published within a few days.