House Down Payments Soar To 20 Year High As Banks Crack Down On New Loans

American homebuyers have to pony up even greater amounts of money for a down payment due to tightening credit standards and skyrocketing home prices.

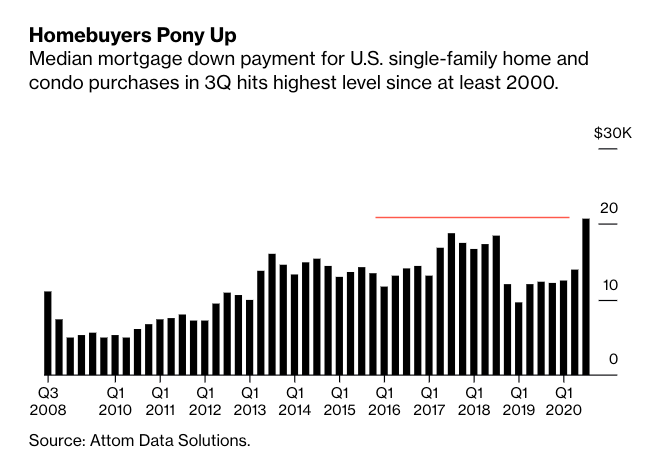

According to Bloomberg, citing a new report from Attom Data Solutions, the median down payment for a single-family home is $20,775 for the third quarter, the most in at least two decades and up more than 69% from $12,325 a year earlier. Over the last year, the jump in the down payment cost outlines how lenders have become more cautious in these uncertain economic times.

It was also noted borrowers paid 6.6% of the median sale price of homes financed over the quarter, up from 4.7% a year earlier and the highest level since 2018. On average, borrowers were loaned around $275,000, the highest since 2000, up 24% from last year's third quarter.

Todd Teta, chief product officer at ATTOM Data Solutions, said, "down payments are rising at a time when lenders are tightening their guidelines."

(Click on image to enlarge)

Teta continued: "Lenders have grown more cautious to protect themselves from more delinquencies."

A combination of outbound migration flows from cities and a record low 30-year mortgage rate below 3% ignited home prices in rural communities.

Bloomberg noted, "mortgage companies are raking in cash amid the pandemic, earning hefty margins. At the same time, consumers flood in to buy homes or refinance existing loans to take advantage of record-low mortgage rates."

A senior loan officer at Freedom Mortgage, Lewis Sogge, said, "2020 has been a record-breaking year for the volume of new loans and refinances as consumers take advantage of record-low mortgage rates."

Lenders are becoming increasingly worried about borrowers as the virus pandemic's reemergence has resulted in states and cities reimposing strict social distancing measures. What this means is that economic growth will likely slump in the fourth quarter and into early 2021.

Worried about delinquencies and a possible double-dip recession that would result in job loss, lenders at JPMorgan Chase & Co. have tightened terms for borrowers. Loan officers at the bank were recently put on notice to limit jumbo loans to 70% of the sale price for co-ops and condos in Manhattan.

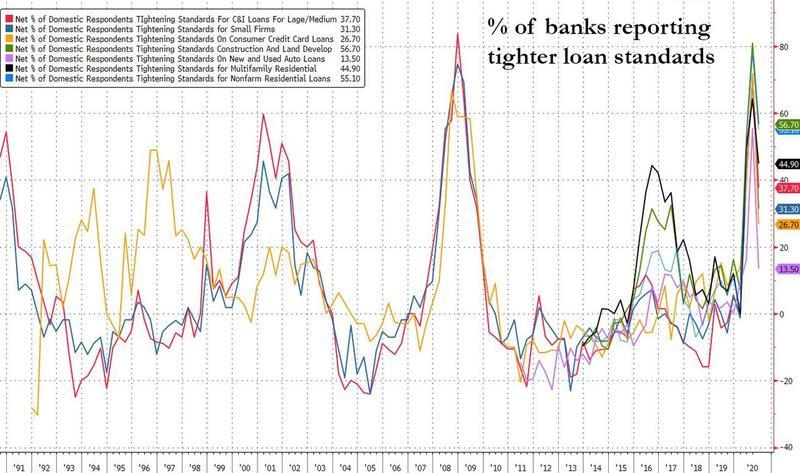

Besides real estate, a similar picture was seen for tightening credit standards of consumer loans.

(Click on image to enlarge)

And while lending standards have eased somewhat, down from levels over the summer that made it nearly impossible to get a bank loan - the ability for average folks to buy a home is becoming harder and harder.

Disclaimer: Copyright ©2009-2020 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies every time ...

more