Here’s The Painful Irony Of The FIRE Early-Retirement Movement

Over the past few years, a new movement has become popular with millennials: the Financial Independence/Retire Early, or FIRE, movement. Those who follow the FIRE lifestyle aspire to escape the soul-crushing rat race of debt, unfulfilling jobs, consumerism, and keeping up with the Joneses. FIRE movement members aim to achieve their goals through a combination of regular salaries, building additional entrepreneurial income streams, extreme frugality, and investing in the stock market. Considering the challenges we millennials have faced in the past decade due to the Great Recession and the increasing difficulty of attaining comfortable middle-class lives, it’s not hard to understand the appeal of the FIRE philosophy. Unfortunately, there is a major blind spot in most FIRE disciples’ plans that will prove to be their undoing: the penny wise, pound foolishness of extreme frugality while investing in the extremely overvalued stock market.

Here are some of the central tenets of the FIRE movement according to MoneyStir.com:

Save 40%-70% of your after-tax income.

Quit your full-time job after ten years or so, usually in your 30’s or 40’s. Few have achieved this in their 20’s.

Learning to avoid revolving credit card debt.

The focus is on the short-term sacrifice to achieve the goal as fast as possible, which usually means being frugal and reducing expenses.

Pay off your mortgage, or end up downsizing to a smaller/cheaper house.

Invest in low-fee investments, like index funds.

Drive used cars, and if possible downsize to one or zero cars.

Many use the 4% rule to determine when they can retire. The idea is that pulling out 4% per year from your investment “should” mean your investments continue to grow and you don’t need to live off of the principle. So having $1,000,000 invested, you could live off of $40,000/year.

Many blogs are trying to re-wire the standard definition of FIRE by focusing on financial independence.

Having financial independence is usually defined as having a net worth of 25x your expenses.

The definition of “retirement” is used loosely. The goal is not necessarily to quit your job but having the flexibility in how/when you work.

Increasing income helps to achieve financial independence faster.

It is about hacking life to pursue your goals.

FIRE movement members are known for their extreme frugality that practically borders on asceticism. FIRE members often cut out vacations, don’t eat out, quit their daily coffee habit, grow or raise their own food, choose to live in RVs instead of apartments or houses, use bicycles instead of automobiles, become extreme couponers and DIYers, and so on. To put it simply, FIRE movement members make heavy sacrifices and radical life changes in hope of achieving their dream.

While their intentions are certainly admirable, FIRE movement members who make radical sacrifices to literally save a dime here and a nickle there only to invest that hard-won savings in the extremely overpriced stock market (via low-cost index funds) are naive and missing the forest for the trees. The painful irony is that FIRE movement members who pursue this approach are frugal with their high-frequency small-scale purchases but are spendthrift high-rollers with their largest purchase. It’s almost like being a miser for many years so that you can pay $100,000 for a car…except that car is really worth $25,000 or even less.

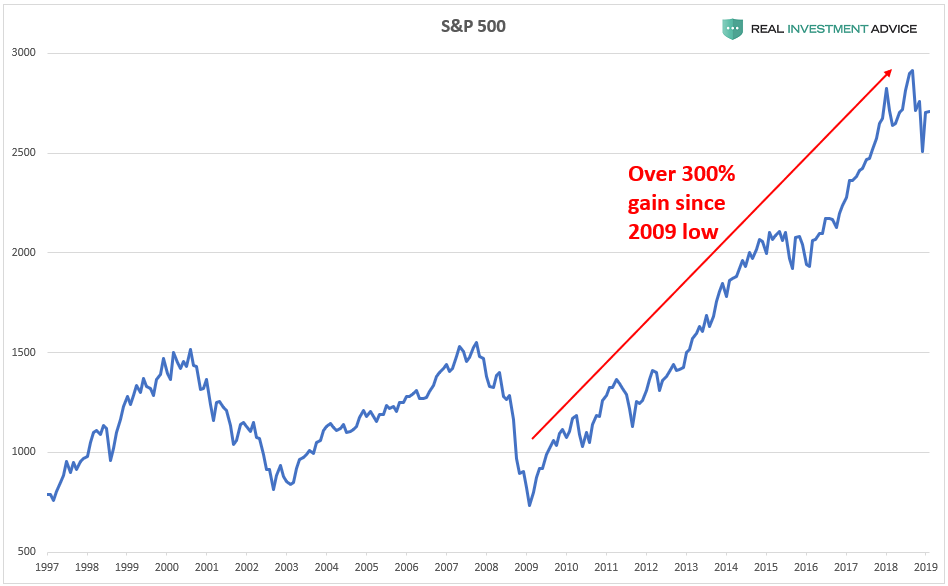

Anyone who is investing in the U.S. stock market now (and it makes zero difference if it’s via low-cost index funds) is investing in an artificial market that is up more than 300% since its Great Recession lows. There is only one reason for this: the Federal Reserve inflated a massive stock market bubble (see my explanation in this piece), which is no different than the housing bubble that they also inflated in the mid-2000s.

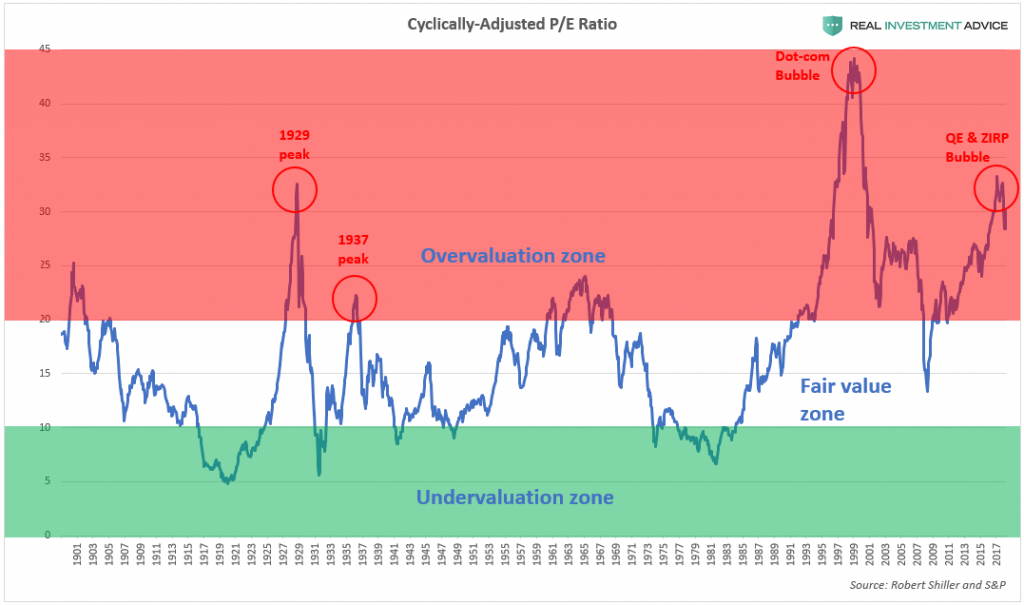

The U.S. stock market surge of the past decade is not driven by fundamentals such as earnings, which is the reason why today’s market is extremely overvalued (aka “overpriced” for the penny pinchers) relative to its earnings. For example, the cyclically-adjusted price-to-earnings ratio is near the same levels as it was in 1929 before the stock market crash and the Great Depression. The chart below shows how infrequently the market has traded at these nosebleed levels in the past 120 years. When the market is overvalued, it eventually reverts back to the mean, which implies a painful bear market that brings stocks back to more reasonable levels.

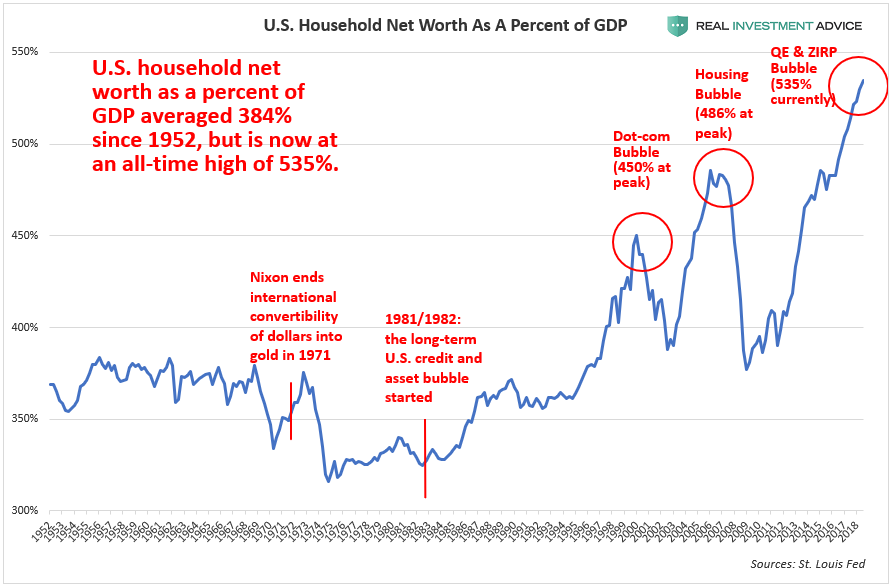

The chart of U.S. household wealth as a percent of GDP shows just how inflated asset prices (primarily stocks and bonds) have become relative to the underlying economy. Household wealth surged during the dot-com bubbles and housing bubbles, only to come crashing down again. Our current Fed-driven bubble blows the last two out of the water, and the coming bust will be proportional to the surge (which is a very scary thought).

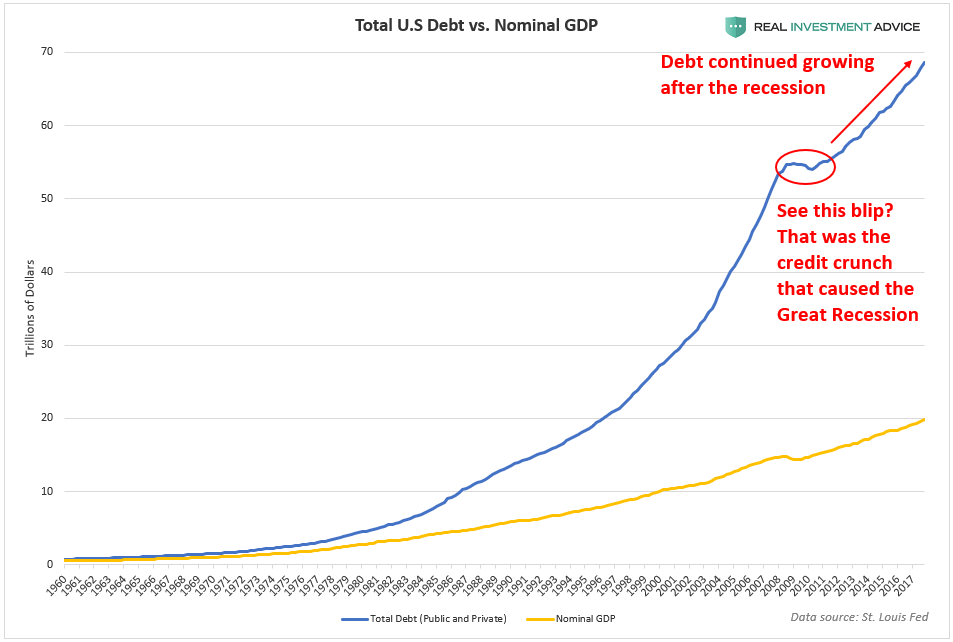

Undoubtedly, at this point, many optimistic readers are thinking “I’m not worried about the market dropping – it’ll go back up like it always does! Plus, I’m in it for the long haul!” Unfortunately, that is a very naive way of thinking and it doesn’t account for the fact that were are not experiencing a normal boom and bust cycle, but an unsustainable debt-driven system that is completely shaking itself to pieces. As I recently wrote, the only reason why the U.S. and the global economy has continued to grow after the Great Recession was because we are taking on more debt and inflating new bubbles – we’re basically on the same path that we were on before 2008.

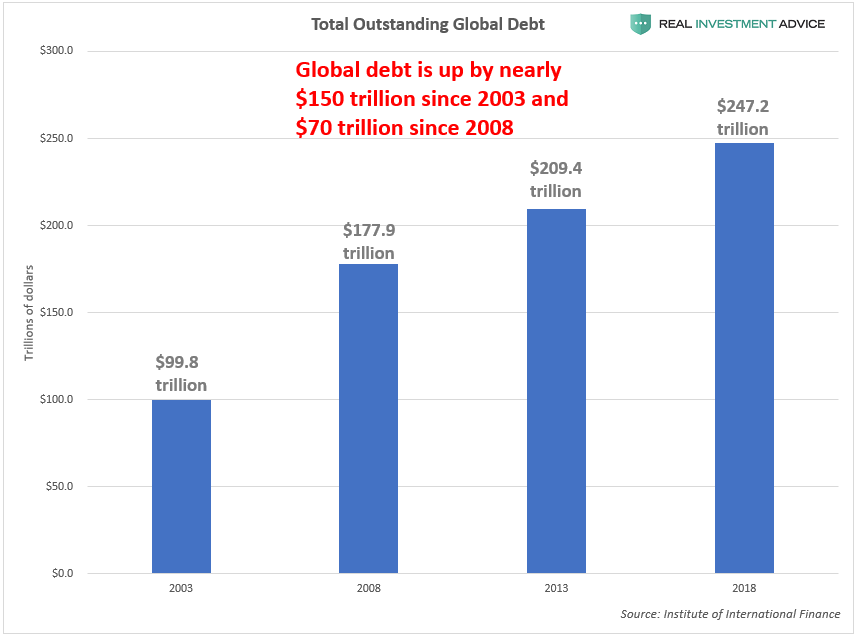

To further outline how unhealthy of a situation we are in, global debt is up by nearly $150 trillion in the past 15 years and up $70 trillion since 2008:

For those who think that the market always goes back up, my response is “don’t be so quick to assume that.” As my boss Lance Roberts has explained many times, secular bear markets that occur after major historic market peaks typically last about three decades. In addition, the markets spend approximately 95% of their time making up for previous losses. Most people only realistically have a few decades to save and invest enough for retirement, so a 30, 40, or 50-something who invests heavily in today’s overvalued stock market is likely to have their retirement plans ruined.

Even if the Fed becomes increasingly desperate to keep driving the market higher by printing more money, the Dow at 40,000 or 50,000 won’t be any consolation when the dollar experiences a dramatic loss of purchasing power. To be successful, FIRE movement members should look at the big picture and avoid being penny wise, but pound foolish. In this overvalued market, I favor having a mix of cash (for liquidity and “dry powder”), some precious metals (as a monetary crisis hedge), and some short-term U.S. Treasuries (for those who need income).

For the author's full disclosure policy, click here.