Hedge Fund Blowup And Rotation Shift To Value

We saw a little bit of volatility the last few days, as an overleveraged hedge fund blew up spectacularly. It was one of the largest blowups in history (over $50 billion) and despite owning some pretty good positions, being leveraged 5-1 almost always assures disaster at some point, unless you are exceptionally lucky, and this fund’s luck ran out. A few banks that we didn’t own had some exposure, but it doesn’t look like it will cause losses of any size to the U.S. banks, which are likely to report phenomenal 1st quarter earnings in a few weeks. We have taken advantage of the volatility to add some attractive positions, we couldn’t have gotten into before this occurred, so barring some massive contagion, which looks unlikely, I don’t see it being too big of a deal for us at least.

Stock returns are highly cyclical, but because most market participants tend to focus on the recent past, this fact is often forgotten. From 2010 to 2021, stocks returned an annualized 11.3% after inflation, which is simply spectacular. Most have now forgotten that the previous decade from 2000 to 2010, U.S. equities lost an annualized 2.3% after inflation. The big thing that drives future returns is starting valuations. From there, aspects such as earnings growth and interest rate trends also can be significant factors. As we’ve written before, current market valuations have only been topped in the Tech Bubble, so 100% long-only index and mutual funds should expect a far more challenging next decade, probably more similar to 2000 to 2010.

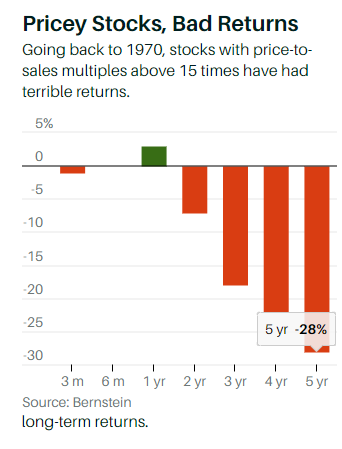

From 1970 to 1920, stocks trading at 15 times sales or more, spent the next three- and five-year periods, with average relative returns of minus 18% and minus 28%, respectively. At 20 times sales, the three- and five-year returns are even worse. According to Tech analyst Tony Sacconaghi, there are currently 366 tech stocks meeting the 15-plus sales-multiple criteria, up from 25 in 2017. It’s the highest total since 2000 when the Nasdaq proceeded to drop by 80% over the next few years. The signs of bubbles are numerous, which is why we are laser-focused on deeply undervalued securities, and we are also utilizing conservative income-generating options strategies to maximize income and reduce risk further. We’re conservatively positioned, with many of our cash-secured put options trading deep out of the money, and many of our long positions have covered calls that provide a further cash cushion. Basically, what this means is that even if our stocks close at these current prices upon option expiration (mostly in January of next year) our accounts would be meaningfully higher. It also means that we have large cushions before we would take losses as long as we let the options expire, as in the short-term volatility can play a big factor, but volatility goes to zero at expiration.

Most of our large positions actually trade at deep discounts to a conservative estimate of liquidation value, pay above-market dividends, and trade at low multiples to normalized earnings, despite strong growth prospects upon reopening. Within a few weeks, every adult in the country that wants to be vaccinated will be able to be, as supply has really ramped up and we are doing between 2-3MM a day. It isn’t a coincidence that value started outperforming ever since the Pfizer vaccine was approved on an emergency basis in early November. Our investments benefit from a reasonably healthy global economy, not some dystopian work exclusively from home one like we saw last year, which favored those companies that benefited from those trends, irrespective of valuations. Last year the most expensive stocks got more expensive, while the cheapest got cheaper, which created a huge runway for value to go on a run, which hopefully can last 3-5 years at least.

Many of the worst-performing stocks last year are the best-performing stocks this year and the same goes for factor strategies such as momentum versus value. Energy and Financials were the worst sectors last year, and they are the best performing sectors this year, while still being among the cheapest areas of the market. Many stocks have gotten absolutely crushed over the last few weeks, despite the market hanging on pretty well. Stocks in the Russell 2000 are down an average of 22.3% from their 52-week highs, and nearly 200 are down over 50%. This is why you never want to just blindly chase performance. It almost always results in selling low and buying high. Many strategies can work as long as they are well thought out, but switching back and forth is usually not very successful.

Here is a great article by Charlie Bilello that goes into more detail, which I’d highly recommend reviewing for more insights on an important shift occurring in the markets, which we expect to continue moving forward: Link to Article