Gundlach’s Remarks Mean It’s Time To Check Your Allocation

“This is a capital preservation market.” So says Jeffrey Gundlach who can’t argue with anyone who wants to invest in the 2-Year U.S. Treasury, currently yielding around 2.7%. If you choose the 10-year, by contrast, and saddle yourself with 8 more years, you get less than 20 basis points of extra yield.

Gundlach is one of the world’s best investors, especially when it comes to bonds, And that means investors can’t always follow him literally because they’re not paying attention to global markets the way he is and can’t move as adroitly has he can.

Still, his remarks, delivered in a CNBC interview yesterday, are a warning for investors to check their allocations. Most investors shouldn’t try to time stock markets to the extent of being all out of or all in stocks with their long term money. But it’s a good time to check your allocation and see if it lines up with where you decided you wanted it when you started investing.

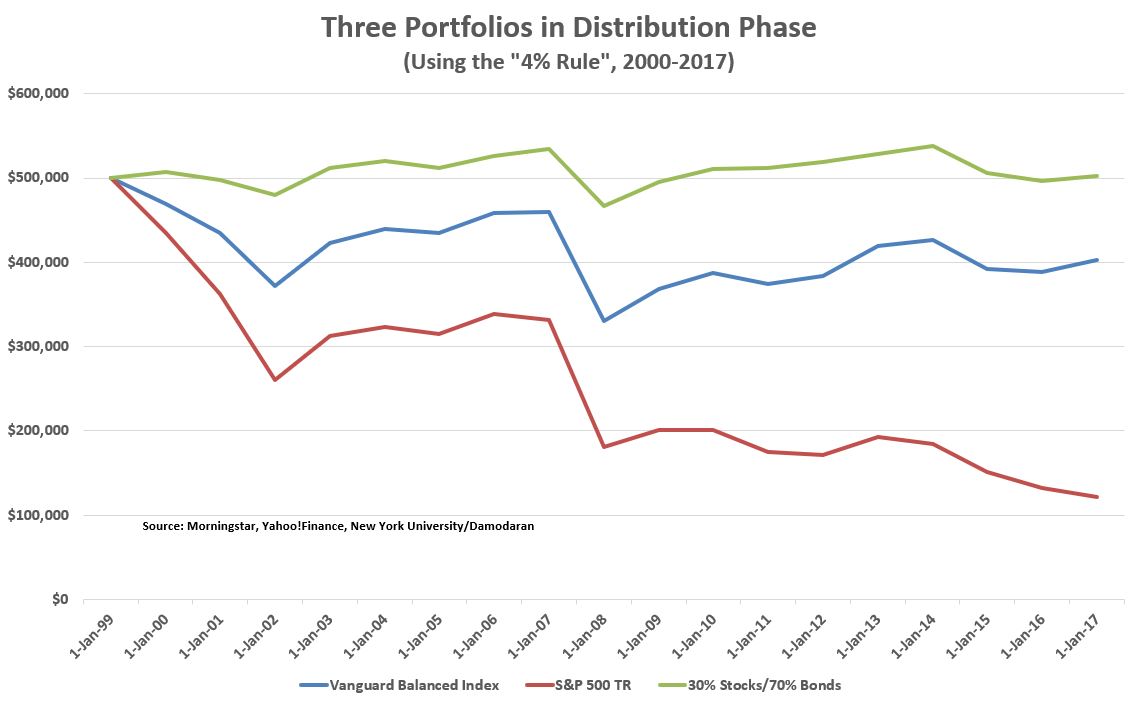

If you want to alter that allocation, and you watch the markets carefully, you can cheat a little with some extra cash. In fact, I think anyone about to embark on retirement and planning to use something like the “4% rule” (taking 4% of your assets the first year of retirement, and then increasing that initial dollar distribution by 4% every year thereafter) should have around 30% in stocks right now.

That kind of conservative portfolio will be able to withstand stock market declines if they occur while distributions are also depleting a portfolio. At least it has since 2000 when stock markets were wildly overpriced and subsequently delivered a 5.4% annualized return for the next 18 years. Retirees should think hard about revising the “4% rule” to the “3% rule,” however, given how low bond yields are now.

(Click on image to enlarge)

Novice investors should also understand that Gundlach isn’t making a prognostication out of thin air. The U.S. markets have been up for nearly a decade without a meaningful interruption. In 2017, U.S. stocks were up every month, which is the only time in history that has happened. Also, the best valuation indicators such as the Shiller PE and Tobin’s Q are forecasting low returns for the next decade. That doesn’t mean a crash will happen tomorrow; no valuation indicator is any good at predicting that. But it means stocks will have to remain at nosebleed prices relative to earnings, sales, and book value to produce returns that can beat inflation by 4 or 5 percentage points. The S&P 500 Index is now yielding a little less than 2%. Another 4% or 5% earnings per share growth annually for the next decade will produce a 6% or 7% annualized return, which sounds good. But stocks must remain at current prices relative to earnings (currently 30 or so on the Shiller scale) in order to pocket those returns. That’s unlikely. A “valuation reversion” or investors deciding that they should pay less for earnings will detract from that 6% or 7% annualized return — possibly in a significant way.

If you’ve been invested in stocks for the past decade, you’ve been given a gift. But the market can take that gift away if investors decide they want to pay lower prices for earnings than they have over the last decade.

Investors should do three things (at least), andone of them won’t be possible to accomplish immediately — 1. Study market history and cycles 2. Check your allocation 3. Find an advisor who can help you.