UK Retail Sales Dip, But It’s Too Early To Blame The Virus

We're not convinced July's fall in UK retail sales can be put down to the rapid spread of the Delta variant. Social spending is a better place to look for that impact, and so far it appears smaller than might have been expected. Instead, retail's latest fall may be down to a rebalancing towards services after lockdowns.

We’ve not had all that much so-called ‘hard data’ since the Delta variant really took off in the UK during July. So it’s tempting to take last month’s unexpectedly sharp 2.5% fall in retail sales as a sign that the virus was starting to have a noticeable impact. We’re not convinced, and think there are three reasons why retail probably isn’t currently the best place to look when gauging the impact of the recent virus flareup.

Firstly, the dip in retail sales through July probably marks something of a correction after a bit of initial buzz when shops reopened (see chart below). And keeping things in context, retail spending is still over 6% above pre-virus levels, something which isn’t true of much else in the UK economy right now.

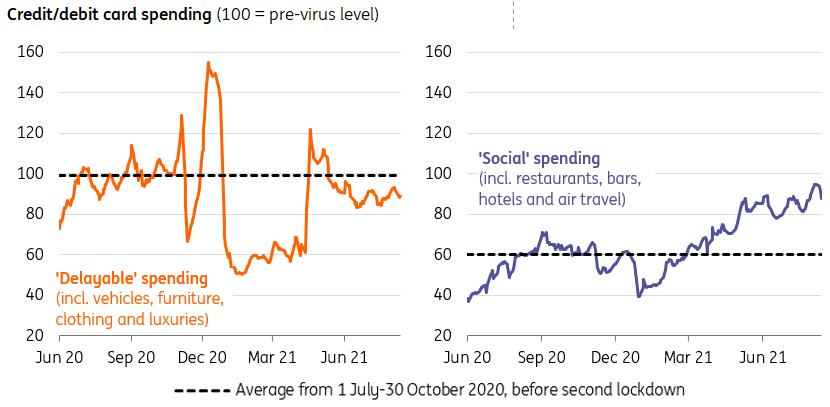

Secondly, spending on goods was always going to come under pressure once services reopened. That is pretty much what we see in the Bank of England’s debit/credit card data. ‘Delayable’ spending, which is primarily goods, is below last summer’s average and has slipped over recent weeks. Social spending, by contrast, recently recorded another post-March 2020 high.

Social spending has been resilient as Covid-19 cases have risen

Source: ONS/Bank of England CHAPs data, ING

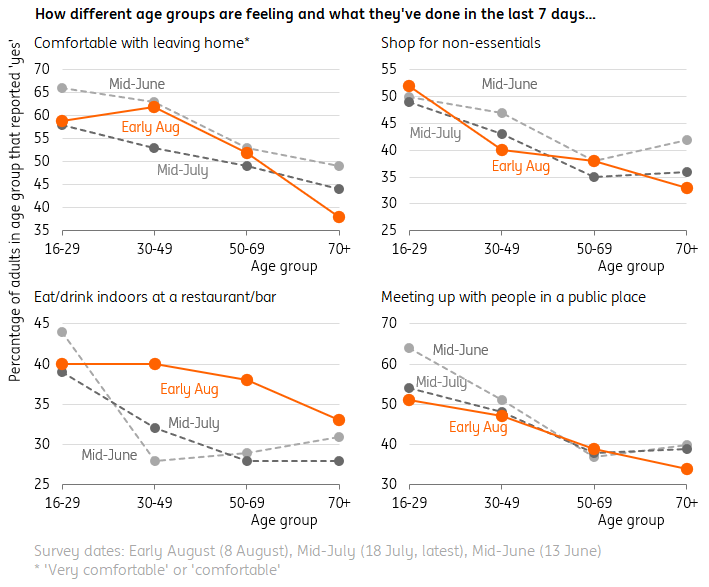

And in fact, we’ve seen no discernible fall in spending at hospitality venues recently, despite hundreds of thousands of people having to self-isolate each week in July. Indeed, according to the ONS’ weekly survey of the virus’ social impacts, the proportion of people visiting an indoor bar/restaurant is currently slightly higher than was in June or July for most age groups.

That suggests Delta hasn’t triggered a major shift in consumer appetite to socialize so far, though we suspect this may become more noticeable over the winter. Even if lockdowns are avoided, which seems likely, increasing NHS pressure over the coming months may see some renewed caution creep in. The fall in the percentage of over-70s saying they are comfortable leaving home recently may be an early sign of this.

In short, further gains in retail sales are going to be hard to achieve over the autumn/winter, even if the wider consumer spending story remains relatively solid.

How consumers are feeling about Covid-19

Source: ONS Coronavirus and the social impacts on Great Britain, ING

Survey dates: Early August (8 August), Mid-July (18 July, latest), Mid-June (13 June). * 'Very comfortable' or 'comfortable'

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more