Turkish Central Bank Keeps Policy Rate On Hold

At its June rate-setting meeting, the CBT remained on hold with the policy rate (1-week repo rate) unchanged at 24%, in line with consensus.

In its statement, the CBT acknowledged improving price pressures after a downside surprise in May, noting “developments in domestic demand conditions and the tight monetary policy” as the monthly reading pulled annual inflation down to 18.7%, from 19.5% a month ago. This was thanks to lower-than-expected food, clothing, and home appliance inflation. On the flipside, and despite easing in the headline and in the core, inflation dynamics have remained difficult with annual services inflation unchanged in May at 15.15%. This is close to the highest level reached for the first time since early 2004, reflecting inertia and relatively high-cost factors and notwithstanding the weakening in growth momentum. The bank remains cautious, avoiding premature easing “…in order to contain the risks to the pricing behavior and to reinforce the disinflation process…”. So, we can assert that the CBT is still concerned by the risk of further currency weakening and has maintained its focus on building credibility.

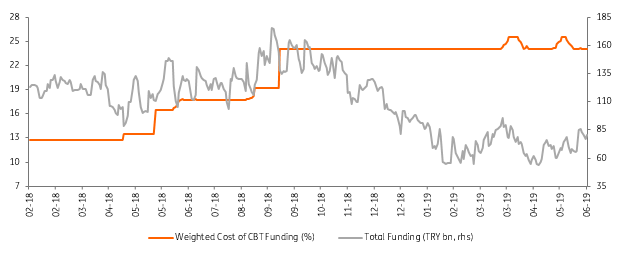

Central Bank Funding

(Click on image to enlarge)

Source: CBT, ING Bank

The remainder of the statement was unchanged. The CBT again noted that (a) the rebalancing trend in the economy continues, (b) external demand maintains its relative strength, (c) domestic activity is at a slow pace, partly attributable to tight financial conditions, and finally (d) the current account balance is expected to maintain its recovery trend.

We continue to expect the CBT to remain cautious on signaling any rate cuts. So, despite improving pricing pressures and recent TRY strength, the CBT will likely maintain its current policy stance in the near term in order to achieve price stability and to support financial stability. We still expect the CBT to start a gradual cutting cycle in September, with the one-week repo rate reaching 22% at the end of this year. Continuation of a supportive global backdrop together with more accommodative central banks globally would increase the possibility of an earlier easing move. Any reviving currency volatility impacting the disinflation trend remains a key variable for the CBT in policy implementation.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more