Turkey’s Economy Rebounds And The Fourth Quarter Looks Bright

Turkey's economy is rebounding strongly from recession thanks to supportive policies and a weak base from last year. Recent high frequency indicators suggest further momentum in the last quarter of 2019.

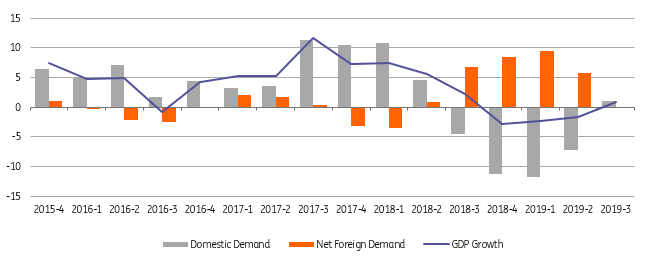

Economic growth turned positive in the third quarter after three quarters of contraction. The year-on-year rate came in at 0.9%, close to market consensus at +1.0% YoY, though higher than our call of +0.5% YoY. The data confirms that the Turkish economy has rebounded strongly from recession, supported by the weak base last year, while the recent high frequency indicators suggest further momentum in the last quarter of the year.

In seasonal and calendar adjusted terms (SA), economic activity continued its recovery, albeit at a relatively slower pace, recording 0.4% quarter-on-quarter growth in the last quarter, after rising by 1.7% QoQ and 1.0% QoQ in 1Q and 2Q, respectively. TurkStat made some minor revisions to the headline GDP data in the first quarter (from -2.4% YoY to -2.3% YoY) and the second quarter (from -1.5% YoY to -1.6% YoY).

Quarterly Growth (%, YoY)

Source: TurkStat, ING

Spending breakdown

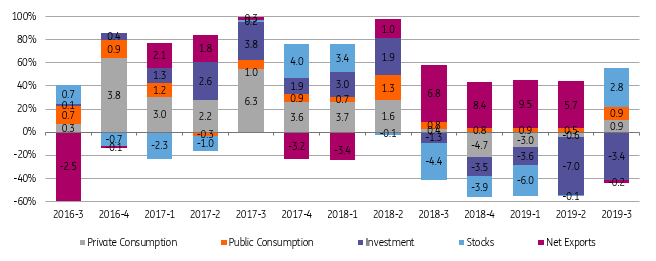

Private consumption, which has the highest share in GDP, turned positive in 3Q at 1.5% YoY amid continuous improvement in the first half. This contributed 0.9 percentage points to growth. Despite the expiry of tax cuts in June, consumption appetite recovered in the third quarter due to the central bank's regulatory move linking reserve requirement ratios to loan growth. The bank is seeking to support activity through faster lending and significant easing is reducing yields and making it more affordable to borrow. The end of the election cycle and resultant fall in political uncertainty as well as an improvement in US-Turkey relations have also helped to boost sentiment and hence private consumption.

Public consumption, which has positively contributed to growth since the second quarter of 2017 continued to do so, with a 7.0% YoY increase, lifting 3Q growth by 0.9ppt. This was reflected in a rise in the annual budget deficit to 2.5% of GDP at end-September from 2.0% at the same period of 2018. Still, a significant increase in non-tax revenues largely from CBT transfers limited the widening in the deficit.

Gross fixed capital formation was down by 12.6% YoY in 3Q, following negative readings in the previous four quarters, pulling headline growth down by 3.4ppt. Accordingly, weak capitalspending remained a major drag on growth, given high corporate sector indebtedness and still subdued capital flows. On a positive note, quarterly growth was roughly flat following large contractions in the previous four quarters. This indicates that in the last quarter we will likely see a positive figure amid a stronger credit impulse and lower bank lending rates.

After large positive contributions in the previous five quarters, the contribution from net trade turned negative, at 0.2ppt. Exports rose 5.1% YoY thanks to improving price competitiveness and strong tourism revenues but imports also rose, by 7.6% YoY. The contribution from inventory was positive, at 2.8ppt, after five consecutive negative readings, meaning that companies have started to build inventories.

Drivers of the growth (ppt contribution)

Source: TurkStat, ING

Sector breakdown

Construction stood out with a negative contribution of 0.6ppt, the only negative number among sectors, while agriculture and industry were among the high contributors, at 0.5ppt and 0.3ppt, respectively. The data confirms that the recovery process has been broadening out among sectors.

Overall, the GDP data shows that there has been a gradual shift in the growth mix from net exports towards domestic demand, driven by private consumption, government spending and inventory building, though investments have remained a drag. Looking ahead, activity will likely gain further momentum thanks to a normalisation in financial conditions. This has been helped by a deep easing cycle, an improving credit impulse from the CBT’s macro prudential move, and supportive base effects from last year.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more