Turkey: Recovery At Full Speed

As evidenced by early indicators including industrial production and retail trade, GDP rebounded strongly in the third quarter driven by private consumption, gross fixed capital formation, and inventory build-up, while the contribution of net exports remained in negative territory.

Source: Flickr

GDP Growth (%, YoY)

Source: TurkStat

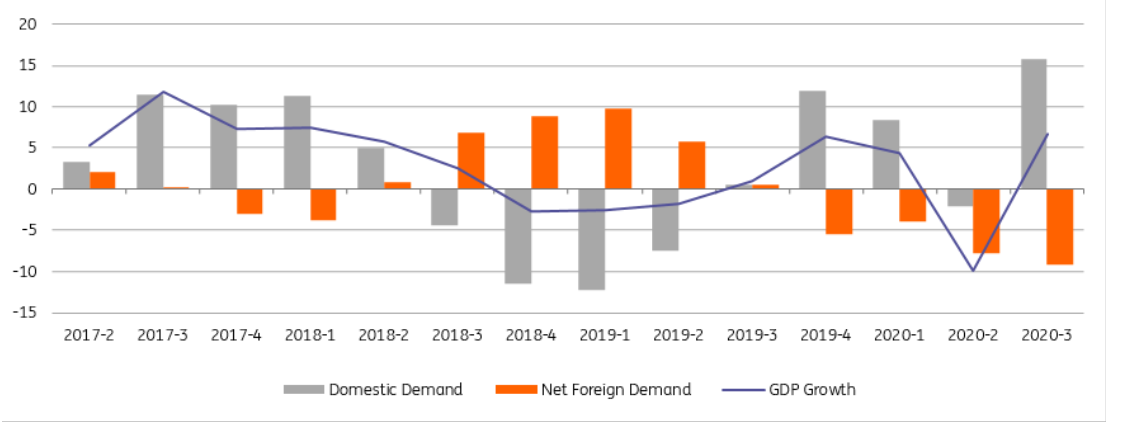

Following a better than expected performance in the second quarter, the Turkish economy recovered at full speed in the third quarter, rising 6.7% year-on-year vs the consensus estimate of 4.8% (and our call of 4.5%). In seasonal and calendar-adjusted terms (SA), the economy expanded by 15.6% on a quarterly basis, the highest ever quarterly change in the current GDP series, after a 10.8% contraction in the previous quarter due to the impact of the pandemic. The quarterly performance is driven by private consumption and investment.

Looking at the spending breakdown:

- Private consumption rebounded by 9.2% YoY and was one of the major drivers, with a +5.4ppt contribution to growth in the third quarter. Significant momentum in consumer credit and other domestic policy impulses is likely to be behind the recovery, despite gradually intensifying efforts to unwind them.

- Thanks to a favorable base, investment spending skyrocketed by 22.5% YoY, the highest since 2011, translating into a 5.2% contribution to the headline rate, as companies in a large number of sectors restored production capacity, with utilization rates rising to pre-pandemic levels. While construction spending increased, as home sales surged on the back of attractive mortgage rates, machinery & equipment investment recorded a strong 24%, the fourth positive quarterly reading in a row. However, the indebtedness of the corporate sector will remain an important drag on new investment given the recent weakness in the currency.

- With the countercyclical policies adopted, public consumption has been lifting GDP every quarter since the second half of 2017 with the exception of the second quarter. In 3Q, we saw a slight positive contribution.

- We also saw a contribution from inventory drawdowns (+5.1ppt). These contributions, which have been largely positive for the last five quarters, likely reflect some measurement problems.

- On the flip side, net exports were a drag, reducing the headline growth rate by another 9.1ppt in the third quarter. This is attributable to a drop in exports of 6% YoY while imports rose by 3.1% YoY. This is not surprising given the widening in the external deficit.

In the sectoral breakdown all sectors, with the exception of professional and administrative services, have lifted the headline growth rate, showing a broad-based recovery. Among positive drivers, industry and financial services have been the biggest contributors, pulling the third quarter performance up by 1.5ppt each.

Overall, as already evidenced by early indicators including industrial production and retail trade, GDP rebounded strongly in the third quarter, driven by private consumption, gross fixed capital formation, and inventory build-up, while the contribution of net exports remained in negative territory. Some indicators for the fourth quarter show the strong momentum has continued although the pace of activity will decelerate given recent moves by the Banking Regulation and Supervision Authority and the Central Bank of Turkey. Also, downside risks are also increasing for the period ahead given the rise in Covid-19 cases and intensifying efforts to get the pandemic under control.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more