Turkey: Recovery Accelerates

The Turkish economy, which has rebounded strongly from recession, continues to recover at an accelerating pace.

People walking on the famous Istiklal Street, Istanbul

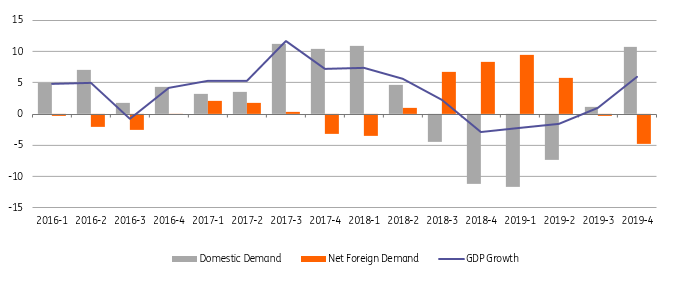

Fourth-quarter GDP growth was better than expected at 6.0% year-on-year vs the market consensus at 5.0%, gaining further momentum after turning positive in the third quarter. The data, supported by a weak base in 2018, confirms a strong rebound from recession. Recent high-frequency indicators suggest this performance should continue in the first quarter of 2020.

GDP growth was in positive territory last year, at 0.9%, down from 2.8% a year earlier but higher than the government’s 0.5% projection, according to the New Economic Programme announced in September 2019.

In seasonal and calendar-adjusted terms (SA), economic activity recorded 1.9% growth quarter-on-quarter in the final three months of the year, after rising by 1.1% and 0.8% in the second and third quarters, respectively, thanks to various stimulus measures and an accommodative policy stance.

Quarterly Growth (%, YoY)

(Click on image to enlarge)

Source: TurkStat, ING

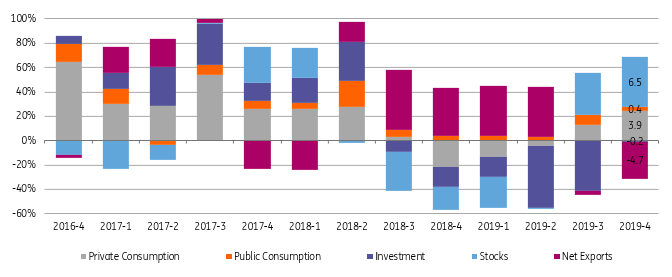

Spending breakdown

Private consumption, which has the highest share in GDP, has remained the major driver of growth, providing a 3.9ppt contribution. A further recovery in consumption appetite in the last quarter was due to significant consumer credit momentum, with the central bank's macro-prudential move linking RRRs to loan growth, as well as deep easing, which pulled down yields and supported borrowing affordability.

Public consumption, which has lifted growth continuously since early 2017, maintained a positive contribution at 0.4ppt in the last quarter of 2019. This was reflected in the annual budget deficit widening to 2.8% of GDP in 2019 from 1.9% in 2018, despite the limiting effect of non-tax revenues largely driven by transfers from the Central Bank of Turkey.

Gross fixed capital formation remained negative at -0.6% YoY but has shown significant improvement over the previous quarters since the August 2018 shock. This is due to ongoing strength in the credit impulse and lower bank lending rates. The recovery is mainly attributable to accelerating machinery investment, which has grown 11.7% YoY, while construction investment has dragged down the headline, although the pace of contraction has slowed to -8.9% YoY from double digits in previous quarters.

After turning negative in the third quarter with the end of external rebalancing, the growth contribution of net exports provided the largest dampening effect on the headline rate since the second quarter of 2011, at -4.7ppt. This is attributable to reviving import demand, which rose 29.3% YoY while export growth remained modest at 4.4% YoY.

Finally, the contribution from inventories was another major driver of fourth-quarter growth with a +6.5pp contribution. This followed the first positive reading in the third quarter, which came after five consecutive negative prints. This means that companies accelerated inventory build-up amid an improving outlook.

Drivers of the growth (ppt contribution)

(Click on image to enlarge)

Source: TurkStat, ING

Sector breakdown

In the sector breakdown, with the exception of construction, all sectors lifted the headline number, while services and industry were among the biggest contributors, at 1.8ppt and 1.2ppt, respectively. The data confirms that the recovery process has been widening among sectors.

Overall, the GDP recovery has been accelerating on the back of supportive policies and a weak base, with a changing composition in favor of domestic demand. This is because 1) private consumption is stronger despite still low consumer confidence 2) investment has been catching up with the acceleration in machinery investment while construction investment has lagged. Looking ahead, activity will likely get stronger thanks to the normalization in financial conditions, and an acceleration in lending, while the impact of robust consumption and improving investment will be dragged down by declining net external demand.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more