Turkey: Inflation Remains On An Upward Path

Turkish inflation maintained its uptrend in February reflecting still strong cost-push factors, sticky services inflation, and elevated inflation expectations.

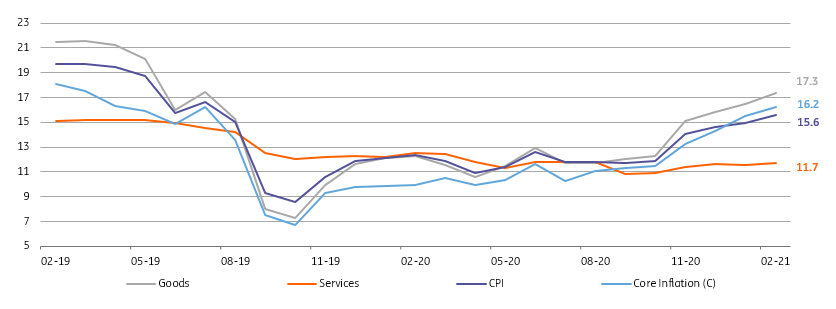

Evolution of Annual Inflation (%)

Core = CPI excluding energy, food & drinks, alcoholic beverages, tobacco, gold

Source: TurkStat, ING

With another higher than expected reading of 0.91%, annual CPI inflation in February maintained its uptrend, reaching 15.6% (consensus: 15.4% and our call: 15.2%) from 15.0% a month ago. The latest data, which includes a further rise in the core rate to 16.2%, confirms that the inflation dynamics affected by demand conditions, elevated services inflation, the recent uptrend in commodity prices and supply constraints during the pandemic, remain challenging.

In the breakdown, we see 1) goods inflation at 17.3%, the highest since mid-2019, up from 16.5% a month ago attributable especially to processed food and clothing along with base effects from the last year 2) services inflation inching up further to 11.7%, driven by rent as well as catering and transportation services.

The Domestic Producer Price Index (D-PPI) exceeded 27% having seen a sharp uptrend since last May on the back of exchange rate developments but also recent pressure on commodity prices and strong base effects. The outlook indicates significant producer price-driven cost pressures on the inflation outlook.

Annual inflation in Expenditure Groups

Source:TurkStat, ING

Regarding the main expenditure groups:

- Food has remained the biggest contributor to the headline rate, adding 67bp, due to processed foods - the monthly reading in this group was the highest February figure in the current inflation series. This is attributable to ongoing increases in global food prices despite TRY appreciation mitigating some of the adverse effects. Unprocessed foods, on the other hand, were relatively benign, at close to the February average in the past. Accordingly, we saw an increase in annual inflation in this group to 18.4% (vs the Central Bank of Turkey's 11.5% call for end-2021).

- The second highest contributor was health, adding 10bp, on the back of exchange rate adjustments in the pricing of medicines.

- The monthly contribution from housing of 9bp was due to rent, and hikes in water fees was another driver of February inflation. Restaurants-hotels added 8bp due to catering services and the increases in food prices.

- On the flip side, clothing prices dragged down the headline rate by 5bp, reflecting seasonal patterns, though the supportive impact was more subdued this year.

Overall, the higher-than-expected change in inflation last month and continuing pricing pressures reflect still strong cost-push factors, sticky services inflation, and elevated inflation expectations. Inflation will likely peak in April though upside risks continue given the likely recovery in demand conditions in certain groups, the impact of rising international commodity prices, the possibility of tax adjustments and still high inflation expectations.

Given this backdrop, the CBT will remain cautious in the near term given not only inflationary pressures, but also concern about the level and composition of reserves, high dollarization and the need to maintain capital flows.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does ...

more