The downtrend in annual inflation continued in May as widely expected, falling to 39.6%. This was due to strong base effects and natural gas subsidies provided by the government.

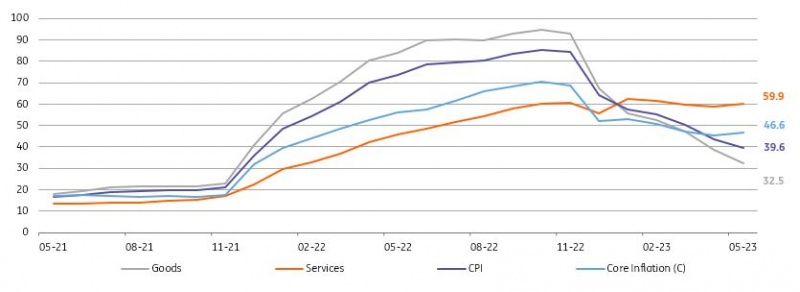

The annual inflation rate has remained on a downward path with another drop in May to 39.6% from 43.4%, even though the monthly reading of 0.04% turned out to be slightly higher than the consensus (at -0.2%). The continuation of the downtrend last month was attributable to: i) TurkStat's implementation of the "zero price" method for natural gas subsidies. Accordingly, the natural gas sub-group saw a monthly price decline of 100%. And ii) the 2003-based index average for May in the last five years was at +1.6%, pointing to a favourable base effect for this year. With the May data, cumulative inflation in the first five months has already reached 15.3% (vs the Central Bank of Turkey's forecast of 22.3% for the whole year in the April inflation report).

Core inflation (CPI-C) came in at 4.25% month-on-month, rising to 46.6% on an annual basis. This suggests that the exchange rate and commodity price-driven improvements in core inflation indicators in recent months seem to have come to an end. The underlying trend (as measured by 3- month moving average, annualised percentage change, based on seasonally adjusted series) for the headline rate markedly recovered in comparison to the last month thanks to goods inflation, while the services group has maintained the elevated trend given continuing pressures in rent, catering and telecommunication services.

PPI inflation recorded another sharp fall, to 40.8% YoY, the lowest reading since May-2021, from 52.1% YoY a month ago, implying improving cost-push pressures in recent months. While the monthly reading was at 0.65%, with support from price drops in heavy-weight utilities and petroleum products, the base effects have remained the key determinant of the decline in annual inflation.

Inflation outlook (%)

TurkStat, ING

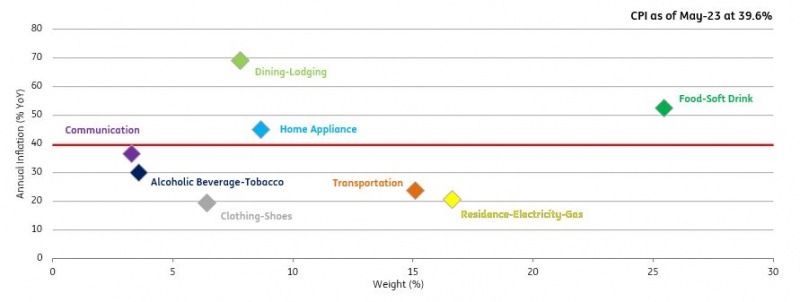

In the breakdown of the main expenditure groups, catering turned out to be the major contributor to the headline rate, adding 61bp, reflecting the impact of food prices, higher costs and buoyant domestic demand. This group was followed by clothing, pulling the headline up by 54bp, due to strong seasonality which was more impactful than it was in the last year. Transportation was the third major driver, with a 28bp contribution, thanks to higher automotive and transportation services prices, though annual inflation in this group declined mainly due to base effects. Annual inflation in the food group, on the other hand, continued to decline to 52.5% thanks again to a favorable base, though the monthly figure was above the long-term May average, pulling the headline up by 19bp. On the flip side, housing was the major determinant of the monthly figure, with a -2.09ppt impact. This is because TurkStat said it would reflect the impact of the government’s decision to provide natural gas free of charge to households in May in its inflation calculations. TurkStat’s practice is in line with EuroStat guidelines, according to its statement.

As a result, goods inflation moderated to 32.5% YoY, a level seen before the Dec-21 volatility, while annual inflation in services was 59.95% YoY, close to the peak of the current inflation series. This was significantly affected by domestic demand and minimum wage increases and hence accelerated significantly due to rents, restaurants and hotels, communication services and other services in recent months.

Annual inflation in expenditure groups

TurkStat, ING

Even though the elections are now behind us, at this stage, uncertainty about exchange rates and interest rates persists, as it is expected that the new economy management, led by Mehmet Simsek, will bring about significant changes in the CBT and the monetary and exchange rate policy to be implemented in the short term. Accordingly, a lira adjustment post-election and potential adjustments in wages and administered prices are likely to weigh on inflation momentum, while the new equilibrium in rates will be key to return to disinflation.

More By This Author:

FX Daily: Trading The 50-50 RiskKey Events In Developed Markets For The Week Ahead

Asia Week Ahead: Reserve Bank Of Australia To Decide On Policy Rate

Comments

Log in or sign up to join the conversation.