Turkey: Further Frontloading By The Central Bank

The Central Bank of Turkey remains confident about the strength of the ongoing disinflation trend and has again frontloaded the easing cycle with another large 325 basis point cut.

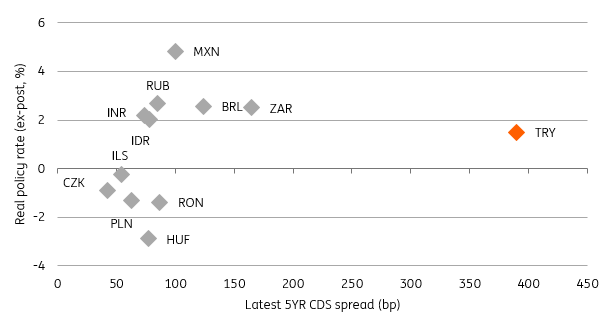

With another frontloading move at the September rate-setting meeting, the Central Bank of Turkey (CBT) announced a deeper than expected policy easing by cutting the policy rate (one-week repo rate) by 325bp to 16.5% vs the market consensus at 250bp (and our call at 175bp). Given the CBT objective of “a reasonable rate of real return”, the ex-post real policy rate dropped to 150bp from 470bp before vs the average ex-post policy rate for major emerging market peers around 200-300bp, while the ex-ante policy rate stands slightly above 425bp after the decision.

The variables that determine the CBT’s reasonable real return objective are:

- Global pricing (i.e. real interest rates of other peer countries). This has gradually improved since the July rate-setting meeting, as also indicated by the CBT’s latest statement that “advanced economy central banks have started to adopt more expansionary policies….support(ing) the demand for emerging market assets and the risk appetite…”

- The inflation path. This surprised to the downside for the fifth consecutive month in August thanks to still weak domestic demand, relative strength in the Turkish lira, gradually improving inflation expectations, a plunge in unprocessed food prices and downward pressure in energy prices. This came despite some one-off factors like tax and administrative price adjustments. Although the CBT’s expectations survey shows a 13.96% inflation rate for end-2019 (12.21% for the next 12 months), expectations could go down further in the coming months, though the TRY performance will be key to the evolution of inflation. Helped by a supportive global backdrop as well as a faster than expected recovery in the inflation outlook and ongoing improvement in inflation expectations, the CBT used its “room to maneuver “ to overdeliver.

Real Policy Rate vs CDS premium (%)

Source: TurkStat, CBT, ING

In its accompanying statement, the CBT seemed confident about its move as “the current monetary policy stance, to a large part, is considered to be consistent with the projected disinflation path”. Regarding guidance for monetary policy, the CBT reiterated that 1) "keeping the disinflation process on track with the targeted path requires the continuation of a cautious monetary stance" and 2) "the extent of the monetary tightness will be determined by considering the indicators of the underlying inflation trend to ensure the continuation of the disinflation process".

Given increasing references to growth in the governor’s early remarks and in the MPC statements, it's clear that activity is a key determinant of policy, in addition to inflation. In its September note, which also summarised the growth outlook in the first half, the bank portrayed a relatively better picture, as “leading indicators point to a partial improvement in the sectoral diffusion of economic activity”. It also noted the improvement in financial conditions (removing “partial” in the phrase) and the disinflation trend as factors supporting a recovery.

Given the surprisingly positive inflation releases and helped by a supportive global backdrop, the CBT felt more confident about the strength of the ongoing disinflation trend and delivered a significant cut. Going forward, the CBT should be cautious given that 1) inflation expectations are still not well anchored and there is high inertia especially in services inflation 2) there is economic policy uncertainty in the global environment due to the likely impact of trade tensions on growth prospects, despite a projected easing in global financial conditions 3) geopolitical risks continue and risk premiums are still high 4) there is ongoing high dollarisation and a subdued capital flow outlook.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more