Tourism And Transport Lead To Turkish Current Account Deterioration

The current account deficit continued to widen in October, on the back of a deteriorating goods balance and a plunge in services balance too given the collapse in tourism and transportation revenues.

Source: Shutterstock

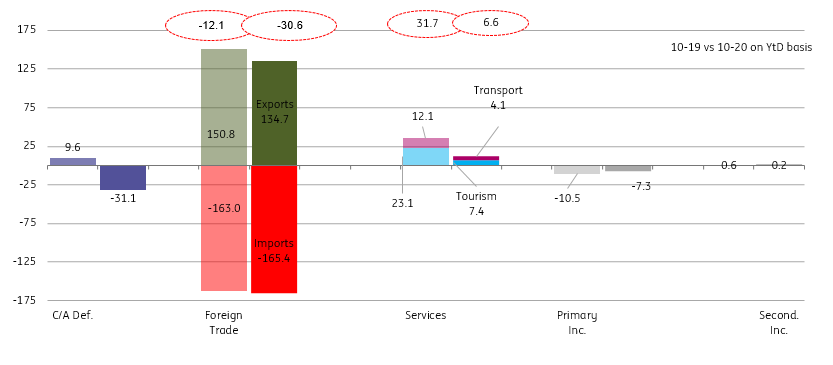

The current account posted a deficit of US$0.3 bn in October, which compares unfavorably to the US$2.7 bn surplus seen in the same month of 2019. As a result, the 12-month rolling current account deficit widened further to US$33.8 bn (4.7% of GDP) from 4.2% of GDP in September.

While primary income roughly offset US$0.5 rise in the trade deficit, the major item that contributed to the widening in the monthly current account deficit was a plunge in services income with continuing weakness in tourism and transportation revenues.

The breakdown of foreign trade shows that gold imports remained high reflecting significant demand by locals, though the rate of growth over the same month of the last year was relatively small. Excluding net gold imports and tourism and transportation revenues, external balances have been roughly stable in comparison to end-2019, showing the extent of impact from the Covid-19 environment.

Breakdown of current account (US$ bn, YtD)

Source: CBT, ING

Capital account turns positive

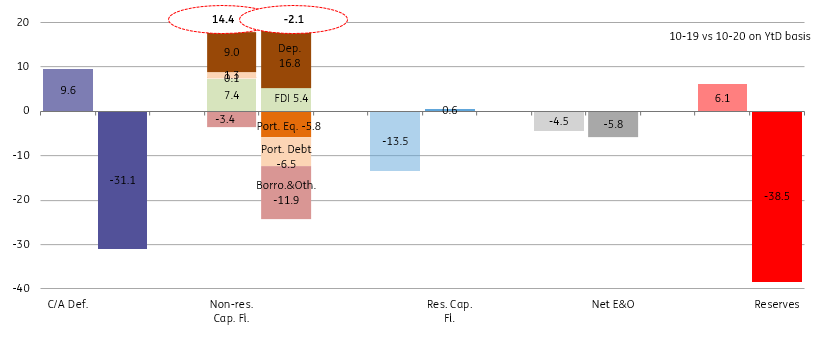

The capital account turned positive in October with US$2.9 bn inflows, thanks to residents bringing US$1.2 bn from abroad, while US$1.7 bn increase in non-resident flows was also contributed to the monthly outlook. With the small current account deficit and net errors & omissions at US$1.6 bn, reserves recorded a marked US$4.2 bn increase (vs US$38.5 bn depletion on a year-to-date basis).

In the breakdown of the non-resident flows, the impact of non-debt creating flows was limited at US$0.2 bn, mainly driven by gross foreign direct investment, while the key debt creating items witnessed US$1.4 bn inflows thanks to the Treasury’s US$2.5 bn eurobond issuance.

On the other hand, net borrowing was negative at U$-1.6 bn mainly attributable to US$2.0 bn debt repayments of the banking sector (with outflows in both short term US$1.2 bn and long-term at US$0.8 bn. This is likely attributable to the time discrepancy between maturing syndications and new borrowings. Corporates managed to borrow US$0.5 bn on net basis after ten months of consecutive net debt repayments.

Accordingly, the long-term rollover ratio for banks was at 63% vs 149% for corporates. On a 12-month rolling basis, banks’ rollover ratio has maintained improving to 85% vs 67% for corporates. Rollover ratios have generally been lower than 100% threshold in recent months, showing the extent of the deleveraging trend.

Breakdown of capital account (US$ bn, YtD)

Source: CBT, ING

Despite increasing normalization efforts by policymakers since August, the current account balance continues to deteriorate given the widening trade deficit and fall in services income. However, with higher interest rates and sharp momentum loss in lending, the widening current account deficit will hopefully slow down in the months ahead. Assuming a partial recovery in the tourism sector and some reversion in gold imports, we expect the deficit to decline next year.

The capital account situation remains challenging, particularly in the wake of the pandemic which has led to large reserve depletion due to external deleveraging, portfolio outflows, and a widening trade deficit. The policy tightening will hopefully be supportive of portfolio flows, as we have seen in November.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more