Top Canadian Picks For 2017

The main reason why the TSX has done so well in 2016 is mainly because pretty much everybody expected the economy to take the oil price drop kick in the mouth and lose some teeth in the process. But it seems that those experts were wrong (once again). As the Canadian economy doesn’t seem to need oil to grow:

Source: Ycharts.

While the oil barrel took a serious beating, the Canadian GDP only stalled for about a year before growing back again. This is explained by various reasons:

- There were several ongoing oil sand projects that continued their course;

- Helped by a weaker dollar, Canadian exportations grew up;

- Canadian service industry picked-up strongly;

- Banks remain strong and show healthy balance sheet.

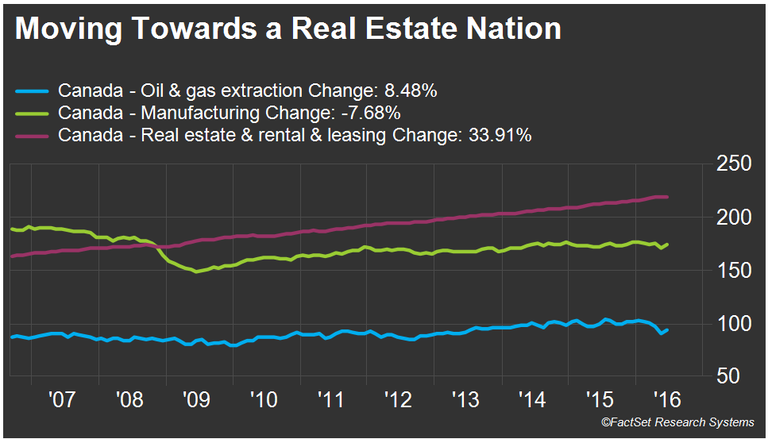

Unfortunately, while I told you to not panic at the end of 2015, I will tell you to not go ecstatic for 2017. While it is quite good news to see the Canadian economy doing well without counting on resources industries, this phenomenon hides a more pessimistic truth. If you have been reading me for a while, you will note that I’m not a big fan of the Canadian housing market. It seems that one of the main reason why Canada economy is not suffering right now is because the housing industry is doing very well:

Source: Factset

At one point or another, the Real Estate industry will not be able to stay the course. When this will happen, banks and services will suffer from Canadian consumers’ mortgage problems. I’m not saying this will happen in 2017 (nobody has a crystal ball), but I’m saying that it’s something to keep in mind while doing further investments. In other words, remain cautious about banks and aim at more defensive stocks for 2017.

I’ve started a tradition of selecting 10 Canadian companies to beat my benchmark, the XDV (iShares Dow Jns Cnd Slct Dvdnd Indx Fnd) back in 2012. Out of all my prediction, my Canadian portfolio failed only once to beat its benchmark. This article is highlighting 3 of my selections:

CINEPLEX (CPXGF)

source: Ycharts

Business model:

Cineplex is the Canada largest movie theatre operators with a huge market shares of 78% counting 164 theatres with 1,677 screens. With the rise of DVD/BlueRay and home theatre, we would have thought that the classic going to the cinema date would become outdated. However, Cineplex was able to improved consumers experience with various combo offers, games and VIP treatments.

Main strengths:

Cineplex main strength is the fact it has the lion share of the movie theatre in Canada. The entertainment business is picking up in the country as Canadian box office was up 12% in Q4 2015 and + 21.8% in Q1 2016 mainly because of the new Star Wars. With a strong movie pipeline for 2017, Cineplex should continue enjoying the uptrend. Cineplex is also improving its services toward more media and gaming offering through The Rec Room.

Potential risks:

The main downside I see with Cineplex is the fact they can’t control how many great movies Hollywood would produce in the upcoming years. Therefore, the bulk of their business is subject to external variations. The movie industry seems on a good roll, but trends in the entertainment business may shift rapidly.

Dividend growth perspective:

Cineplex has the advantage of paying a monthly dividend of over 3%. This is a great company for income seeking investor. The payout ratio has been quite hectic over the past 5 years but recent earnings growth has put it in a more sustainable situation. Management remains cautious about its payout ratio as CGX took a pause of dividend increase in 2015 while the ratio were over 100%.

Investment thesis:

As Cineplex has been able to evolve its business model toward more premium services, it enjoys not only a huge market share, but is able to generate interesting margins. Cineplex is also able to evolve with its time with a successful online streaming platform. Finally, CGX is gradually building a serious bond with its clients through its SCENE loyalty program. From 600,000 members in 2006, SCENE now counts 7,9 million members. Through a strong leadership presence and steady income flow, CGX will continue to reward shareholders for the upcoming years.

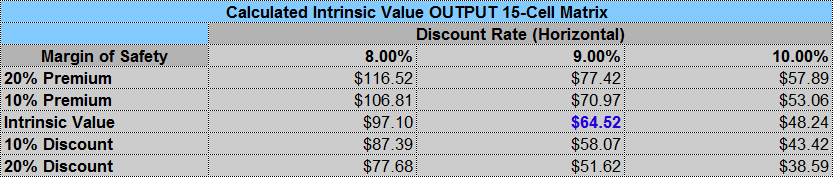

Valuation:

source: Dividend Toolkit Calculation Spreadsheet

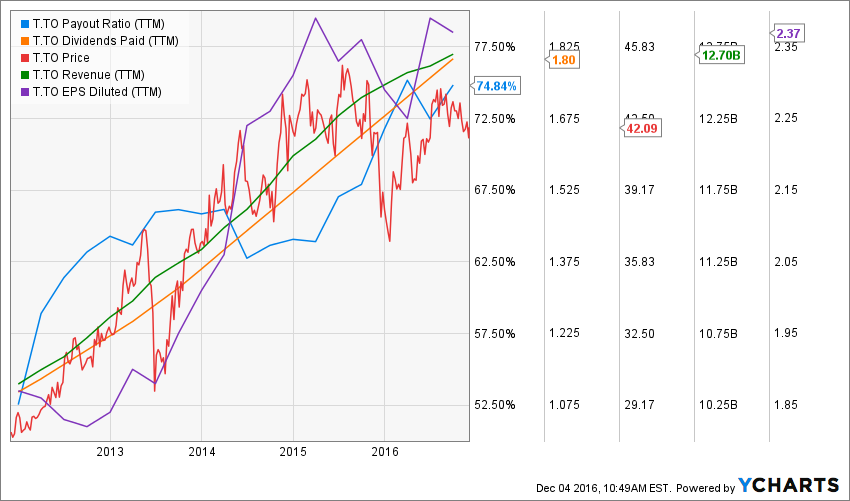

TELUS (TU)

Business model:

Telus offers residential phone, internet, TV and mobile phone services. Back in 2008, Telus also bought Emergis, a leading electronic healthcare solutions provider and then created Telus health Solutions. Considering the number of wireless subscribers, Telus is the 3rd largest provider in Canada.

Main strengths:

The reason why Telus has been part of this selective list since 2012 is mainly because it shows a perfect balance of stability, dividend increase and financial performances. Strong from its mobile revenues, Telus is now eyeing television services as a growth vector. Telus has built a solid brand through stellar client service enabling the company to show the best customer satisfaction surveys.

Potential risks:

At one point, the mobile industry in Canada is reaching a point of maturity. There isn’t much large gap to gain and since the market is shared in a small oligopoly, what Telus could gain from one side, it could lose it from the other. The fear of having a big player (like Verizon 2 years ago) is not imminent anymore, but always a possibility.

Dividend growth perspective:

Telus has aggressively increased its dividend payout over the past 5 years going from $0.29/share to $0.48/share. This had pushed the dividend payout ratio higher (75%), but the company still has enough room to increase it for several years to come. I now expect the dividend growth to slow down to high single digit (6-7%).

Investment thesis:

Similar to Rogers, Telus is more a defensive play. While the DDM calculation shows Telus fairly undervalued, I doubt the Canadian market will give it its full dividend value potential. However, if you are patient, you will earn a 4.50% dividend yield and eventually see the stock value going up.

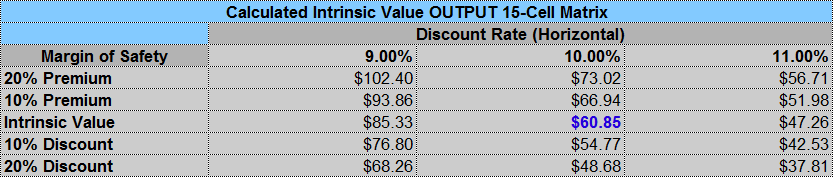

Valuation:

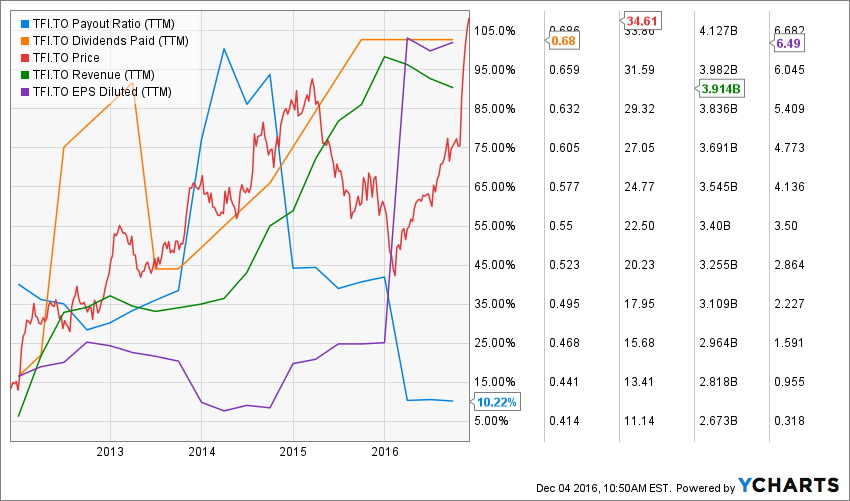

TRANSFORCE (TFI.TO)

Business model:

TransForce is Canada’s largest trucking company and the 9th largest for-hire trucking company in North America. In total, TransForce operates a fleet of 5,348 power units and 17,814 trailers. Headquartered in Montreal, TransForce has 278 terminals across Canada and 91 in the United States.

Main strengths:

As opposed to the railroad industry, Transforce benefited from a surge in truck transportation over the past few years. Being the biggest player in Canada offers TFI more contracts than anybody else during a slowing down economy. TFI also continues growing with the purchase of 3,000 tractors and 7,500 trailers from XPO’s U.S. TL division. Through this transaction, TFI expands its geographic presence as 30% of TL division was from crossing the borders toward Mexico.

Potential risks:

While road transportation is currently beating railroads on many aspect, the contrary shift could also happen. We have seen the transportation industry as a highly cyclical one and stock value could suffer during down turns. At the moment, there is no reason to believe oil price will go up, giving a few good years ahead for companies like TFI. Still, this is always a risk to be considered. Also, there are great expectations coming from their most recent acquisition. A failure to create synergy could drag the stock price down momentarily.

Dividend growth perspective:

While TFI shows a 5 year dividend growth rate of 9.58% (CAGR), the payout ratio remains very… very low (10%). This gives lots of room for management to increase their dividend payout. However, we remained cautious in our calculation as the payout ratio was nearly at 100% not so long ago. We would wish for a smoother trend of earnings, but the dividend payouts are not at risk at the moment.

Investment thesis:

As Transforce is expanding, I believe it is the time to jump in their truck and ride it for a while. Expanding outside of Canada is their smartest move as both U.S. and Mexico economy seems to grow faster in the upcoming years. The economy is doing okay, but not great. With a larger fleet, TFI will be there to pick-up any steady growth in the future. Investing in a leader in Canada and overall North America is a safe bet for anyone building a dividend growth portfolio.

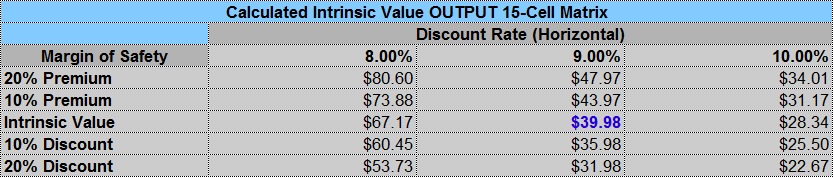

Valuation:

Disclosure: Each month, we do a review of a specific industry at our membership website; Dividend Stocks Rock. In addition to have full access ...

more