Top 3 Canadian REITs For 2020 – And Why RioCan Is Not Part Of It

Most retirees love REITs because their sole purpose is to distribute as much money as possible to their units holder. This sounds like music to the ears of those who are looking for a nice paycheck coming into their bank account every single month (or quarterly). But one must be careful and make sure the REIT chosen will be able to sustain its dividend payment, but also to increase it. This is why I’ve built this Canadian REITs ranking. This top three should give you the guidelines you need to select the right REIT for your portfolio.

Why I Won’t Talk About RioCan… for Long!

You’re going to be disappointed. My top three doesn’t include RioCan REIT (REI.UN.TO) (OTC: RIOCF). Let’s see why it should not be in your portfolio.

RioCan’s yield is huge and the REIT is well established. It owns retail REITs across Canada and RioCan is super strong. Management decided to not let shareholders down and maintain its dividends.

From there, it would be tempting to focus on the yield and to tell me: “Oh, Mike, you’re losing such a great opportunity if you don’t look at RioCan right now!”

Let’s analyze it with a different angle. Over the past 10 years, your paycheck increased by 4.3%. Let me say that again. The REIT loved by any retiree has only increased its dividend by 4.3% in 10 years total.

Would you settle for a job with an annual raise under 0.5% year after year for the next 10 years? This is what RioCan offers you! Your dividend is getting eaten up by inflation.

Plus, stock price comes with another bad news. It hasn’t done much before the pandemic and is now below $15. Again, you are losing on the dividend side because inflation is increasing faster than that.

“But Mike, the inflation is at 1% a year, you’re worrying for nothing.”

Look at your grocery bill: inflation is clearly higher than that. As a retiree, you might not buy houses, computers or cars every year; but groceries and utilities costs will continue to grow at a higher rate than 1%. You’re putting your money and your retirement at risk. This is why we are not in love with RioCan at Dividend Stocks Rock.

Finally, I don’t think that shopping malls will thrive in the future. RioCan has to find other growth vectors, which is going to be hard. Even though they have more than that, those shopping malls will stay and they will probably stay empty too…

Video Length: 00:17:06

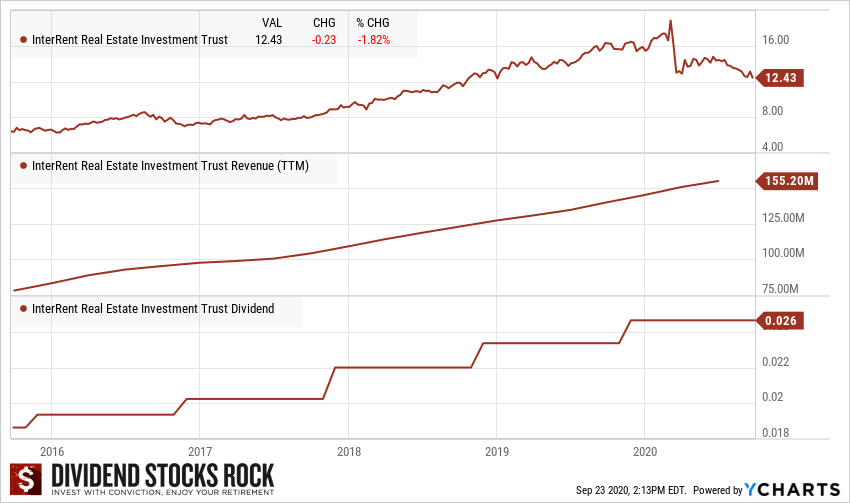

3. The Active REIT: InterRent (OTC: IIPZF)

- Company Name: InterRent REIT

- Ticker: IIP.UN.TO

- Dividend Yield: 3.43%

- Dividend growth since: 2014

- Distribution: Monthly

(Click on image to enlarge)

Business Model

InterRent Real Estate Investment Trust (IIP.UN.TO) is a growth-oriented real estate investment trust engaged in increasing unitholder value while creating a growing and sustainable distribution through the acquisition and ownership of multi-residential properties. The company operations are carried out throughout the region of Canada. IIP is mostly active in the provinces of Ontario and Quebec. Their primary market shows 7,864 suites while their secondary market is at 1,534 suites.

Investment Thesis

IIP is what we describe as an “active REIT” where the company actively buys, improves and recycles properties. This was a very smart business model to manage in two growing provinces (Ont and Qc) in the past few years. InterRent seeks to acquire properties that have suffered from the absence of professional management. This is how it can buy at a lower value and “easily” improve their investment. Although IIP seems to show a solid business model, keep in mind things weren’t so peachy during the 2008 financial crisis. There seems to be lots of hype around this stock lately. The recent stock drop offers an interesting opportunity.

And one thing that is super important right now is that they do a lot of improvement in their buildings or the surrounding area. It results in higher rent rates, but it also attracts Millennials or professionals who have a good job and who can work remotely more easily. This is obviously a great competitive advantage in times of a pandemic.

Potential Risks

With an aggressive growth strategy, IIP has successfully created a lot of hype around its stock. The stock jumped by ~30% between June 2018 and June 2019. This makes IIP a great candidate for a major drop if panic hits the market again… and this is exactly what happened! The stock price has dropped by a couple dollars over the last months. Obviously, there are concerns about the economy and about the fact that most apartment REITs won’t be able to raise their rents this year to convince people to come over. There’s also a risk of having too many properties and then the offer would be too high for the demand. However, when you look at how fast InterRent grows its revenue and how fast it grows its dividend, this is definitely a company to hold in a retiree portfolio.

Dividend Growth Perspective

After a severe dividend cut during the last financial crisis (it showed an AFFO payout ratio of 300% in 2010), IIP started its dividend growth policy back up in 2012 and hasn’t missed a year since. Since their first increase, the REIT has maintained an AFFO payout ratio of around 70%. Both assets and FFO show a similar trend since 2010 (CAGR of 25% and 24% respectively). Shareholders can expect continuous dividend increases as long as the housing market is healthy.

Another great point about InterRent: they are sitting on some cash, they have liquidity available. In summary, you’re looking at a company with a solid down sheet, liquidity, and great growth perspectives in Montreal and in Toronto area. InterRent is therefore a very solid REITs offering you a respectable yield.

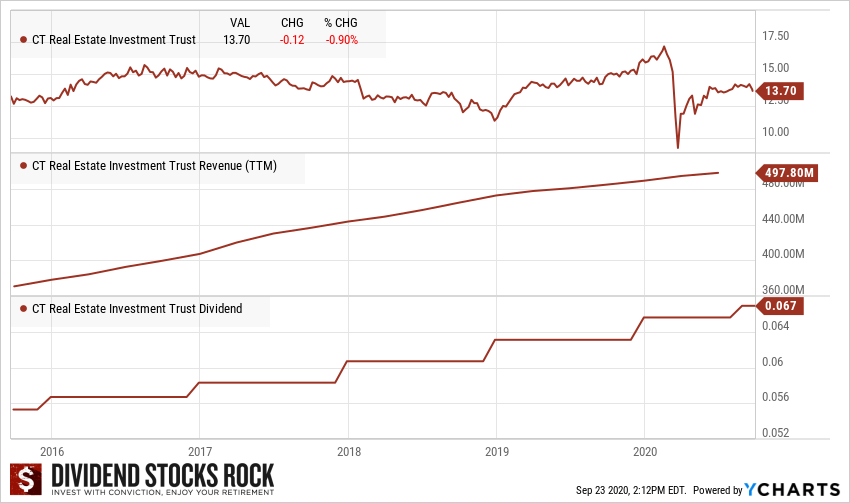

2. The Canadian Tire REIT

- Company Name: CT REIT

- Ticker: CRT.UN.TO

- Dividend Yield: 5.58%

- Dividend growth since: 2015

- Distribution: Monthly

(Click on image to enlarge)

Business Model

CT Real Estate Investment Trust is an unincorporated real estate investment trust that invests in retail properties across Canada. The most significant portion of properties are located in Ontario, followed by Quebec and Western Canada. The trust generates the vast majority of revenue from leasing its properties to Canadian Tire Corporation, which operates the Canadian Tire retail stores. The trust’s portfolio primarily consists of properties anchored by a Canadian Tire retail store, in addition to retail properties not anchored by Canadian Tire, distribution centers, and mixed-use commercial property.

Investment Thesis

An investment in CT REIT is primarily an investment in the real estate business of Canadian Tire. If you think this Canadian retail giant will do well in the future, but you are more interested in dividend than pure growth, CT REIT is the answer. The fact that CRT is paying a monthly dividend with a yield of over 5% is highly attractive for income-seeking investors. On top of that, CT REIT shows a decent dividend growth rate policy matching (and beating) inflation. This makes it a perfect candidate for an income-focused portfolio. The upcoming months will be difficult, but the REIT quality assets will remain.

Canadian Tire is an icon in the Canadian landscape; they have strong brand recognition among small, medium and urban size cities. The fact they own their own brands could help them to battle against Amazon and other e-commerce. You can’t buy Motorcraft or Motomaster pieces elsewhere than at Canadian Tire. This provides them with a very strong advantage. Since the beginning of the pandemic, Canadian Tire has also pushed a lot on its e-commerce (up by 400% in Q2). It could help protecting them against e-commerce giants.

Potential Risks

We often like diversified businesses when we want to add a company to our portfolio. This is not the case with CT REIT. It is mostly leasing all its properties to Canadian Tire. Therefore, if Canadian Tire can’t keep up its growth (we all know how hard it is in the retail business these day), CT REIT will not have many options to compensate. While we like the Canadian Tire business model, we are still talking about a brick & mortar retail store. The pandemic is not helping, either.

All that being said, Canadian Tire is pretty solid right now. Their stores were opened during the shutdown and still are. They should make money this year again, and we shouldn’t see a bunch of Canadian Tire stores being closed.

Dividend Growth Perspective

Similar to InterRent, the stock price got hit. It’s already on the rebound, which tells you that the market is believing in CT REIT. This REIT continues to grow and show a low AFFO payout ratio. This means your paycheck will continue to rise faster than the inflation. Shareholders can expect to cash a solid 5%+ yield with a 2-3% growth rate going forward. This is a good example of sleep-well-at-night type of holding. They also have access to $200 million in revolving line of credit, which means they have flexibility. As the stock price decreased during the pandemic, the REIT now offers a yield close to 6%. If it ever goes pass the market of 6%, this will become a red flag.

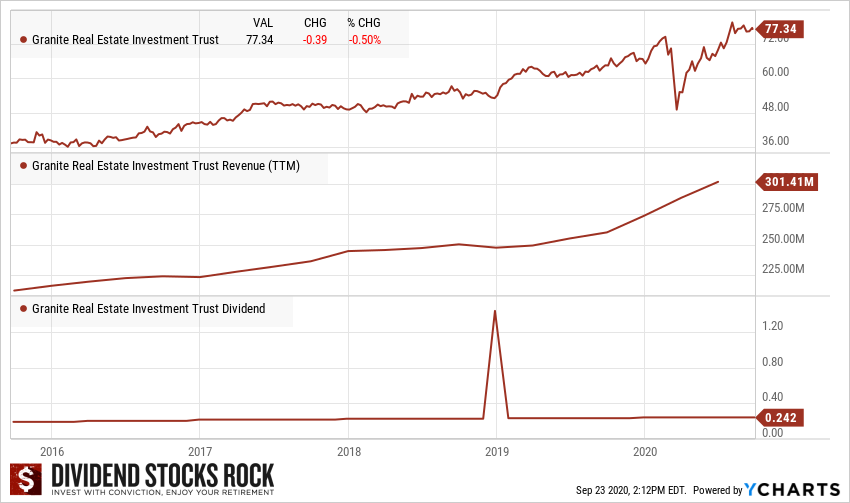

1. The Rock Solid REIT: Granite

- Company Name: Granite REIT

- Ticker: GRT.UN.TO

- Dividend Yield: 3.74%

- Dividend growth since: 2012

- Distribution: Monthly

(Click on image to enlarge)

Business Model

Granite Real Estate Investment Trust, or Granite, is a real estate investment trust engaged in the acquisition, development, and management of primarily industrial properties in North America and Europe. Granite’s portfolio is comprised of various manufacturing, corporate office, warehouse and logistics, and product engineering facilities. The vast majority of the company’s assets are logistics and distribution warehouses and multipurpose buildings split fairly evenly amongst Canadian, Austrian, and U.S. locations. Granite derives nearly all of its revenue in the form of rental income from its properties. The company’s largest tenant is Magna International which accounts for the majority of Granite’s lease income.

Investment Thesis

Granite REIT is ont of my favorites for a long time. It used to be an extension of Magna International (MG.TO). Back in 2011, Magna represented about 98% of its revenues. It is now down to 31% (with Amazon as its second largest tenants with 9% of revenue). Management has transformed this industrial REIT into a well-diversified business without hurting shareholders (quite the opposite in fact!). The company now manages 97 properties (+7 under development) spread across 9 countries. The REIT also shows an investment grade rating of BBB/BAA2 stable. With a low FFO payout ratio (around 80%), shareholders can enjoy a ~4% payment that should grow and match/beat the inflation.

Most properties owned by Granite are modern logistic properties and special purpose properties so it’s an industrial REITs. GRT is looking at large businesses and it is well diversified among several segments. About 60% of its revenue is coming from North America (Canada and the US), but it still has some international exposure, which could help in case there’s a recession in a specific country. Its increased exposure to Amazon (or any distribution center) could turn into a nice growth vector and while having stable tenants.

Granite’s stock price has suffered very quickly during the March crisis but it has fully recovered. In fact, it’s going up because of the interest around the ecommerce.

Potential Risks

One word: Magna. If the car part maker hit a slow down and is forced to close some of its plants, GRT would be one of the first victims. Management is aware of this risk and made efforts to diversify its portfolio through further acquisitions. To reduce its exposure to Magna’s business model, Granite is also selling some of its properties. There is no guarantee that new acquisitions will host tenants as solid as Magna, either. So far, the company has dissipated the risk around a recession and the stock has fully recovered from the March market crash.

Dividend Growth Perspective

GRT has maintained a solid dividend growth policy over the past 5 years (~5% CAGR). With its FFO payout ratio well under control, shareholders should expect a mid single-digit dividend growth rate going forward. In fact, if Magna International business is doing well, GRT will perform and keep increasing its dividend. The REIT also has about one billion in liquid assets, which is spread between cash and equivalent and credit facility. In other words, Granite has everything you need as a retiree… When compared to RioCan, the dividend is a lot lower, but also a lot safer; and it will increase. At DSR, we have issued a buy rating on Granite a while ago. It’s still a buy, but the easy money is gone.

Final Thoughts

As a retiree, you want to select stocks that will provide some income and I totally understand that. However, chasing yield only will create the exact opposite. Instead, look for REITs and other dividend stocks that will provide you with a mix of yield and growth. If you want to learn more about my investing strategy, I suggest you download my free recession-proof portfolio workbook. It could help you build the portfolio you really need.

Disclaimer: Each month, we do a review of a specific industry at our membership website; Dividend Stocks Rock. In addition to have full access to 12 real-life portfolio models, readers can also ...

more