Three Takeaways From The Treasury’s April FX Report

The first FX Report under Secretary Janet Yellen saw a change in language from previous ones, as it dropped the manipulator tag for Vietnam and Switzerland and spared Taiwan, despite all meeting the three criteria. In practice, the implications for the countries are broadly unchanged, but the risk is the Treasury sounds too soft on FX manipulation.

The semi-annual US Treasury’s FX Report was published on Friday (here is the full text). In what was the first report under the new US administration and new Treasury Secretary Janet Yellen, the differences with the previous editions (under former President Trump and Secretary Steven Mnuchin) emerged quite clearly.

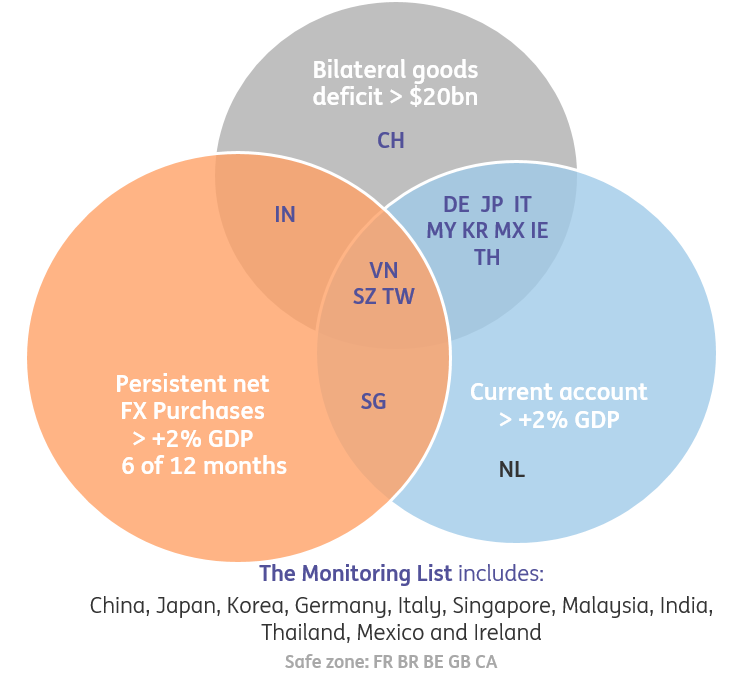

We provide a summary of the content of the FX Report in the chart below and discuss in this article what we think are the key takeaways for markets.

The Treasury’s calculations found that three countries met all three criteria (shown in the chart) to be named a currency manipulator in the four quarters to December 2020: Switzerland, Vietnam and Taiwan. The first two had been named FX manipulators by the previous administration in December 2020, but the Treasury removed the label and refrained from labelling Taiwan.

While countries meeting all three criteria are subject to extra monitoring and dialogues with US officials geared towards ending FX intervention in particular, there is little in the report to suggest other policy interventions, notably on US trade policy or US-China relations. Along with a familiar call for countries with current account surpluses to contribute to rebalancing, this report links insufficient fiscal support for domestic demand to risks of economic scarring in the aftermath of the pandemic. Here, China is singled out for a "focus" on policies which boosted external demand, leaving its recovery vulnerable to weak household consumption.

In general, it appears that the Treasury has started to slowly shift towards a new approach when it comes to the three criteria, possibly adding more weight to FX intervention over trade-related quantitative thresholds.

The report also alludes to ways in which higher trade barriers are reshaping global trade relationships. Vietnam's record surplus with the US is partly explained by "ongoing shifts in Asian supply chains". A policy objective of greater fossil fuel "independence" is flagged as a factor which could contribute to a growing trade surplus for Mexico with the US.

Here, we look at the three main takeaways for markets from last week’s FX Report.

1 Language has changed, implications have not

There was indeed a change in language in the April 2021 FX Report compared to the latest editions under Secretary Mnuchin. The decision to drop the manipulators tag from Switzerland and Vietnam – and by extension, not labelling Taiwan - was accompanied by an analysis of the conditions that would allow the Treasury to designate a manipulator. According to the 1988 Act that established the FX Report, a country is named a manipulator if its currency practices are aimed at preventing balance of payment adjustments or gaining an unfair competitive advantage in international trade.

The Treasury found “insufficient evidence” to determine that any country in the report has manipulated their currencies for those specific purposes. But since Switzerland, Vietnam and Taiwan met all three criteria, the Treasury decided to either continue (Switzerland and Vietnam) or start (Taiwan) bilateral talks with the local monetary authorities. That is not different from what an official manipulator designation would imply, at least in the first year.

So, in practice, the implications for the three countries have not changed materially, and they will still need to prove that they are not manipulating their currencies to gain competitive advantage in the bilateral talks that are set to extend for longer. While this may not be particularly problematic for a country like Switzerland, which has been explicitly used FX intervention as a monetary policy tool, two heavily export-oriented countries like Vietnam and Taiwan will likely continue to run a bigger risk of being treated as a manipulator.

2 The Treasury is likely moving away from the equally-weighted criteria approach

It is highly likely that the Treasury had the intent to signal discontinuity from the previous administration by switching to a more gradual approach to the manipulator designation, stressing how meeting all three criteria does not (or at least no longer) automatically imply that a country will be labelled a manipulator.

From a forward-looking perspective, there is a possibility that this report signals a transition from a quantitative criteria-based approach to addressing foreign FX practices. Even before the release, media reports suggested an ongoing discussion in the Treasury to review the criteria and the quantitative thresholds.

Indeed, there is also a possibility that sparing Switzerland, Vietnam and Taiwan from the the manipulator tag was due to the out-of-the-ordinary nature of the pandemic situation and its distortive impact on global trade flows in 2020 (the Treasury did highlight that in the report), and that the Treasury has no plans to change the criteria-based approach.

But what appears clear is that the Treasury will hardly continue to give the same weight to the three criteria, and more focus should be on actual FX intervention rather than the current account and trade data. In the summary table included in this edition of the FX Report, FX intervention was reported in the first column, rather than the third one as in previous reports, pointing to the bigger weight this is set to have in the future.

3 Yellen may have to compensate for having sent the wrong message

While a more gradual approach to the manipulator designation is indeed suitable – if nothing else because of the pandemic emergency – this edition of the FX Report may have conveyed a message that is in contrast with the pledge by Secretary Yellen to tackle FX mispractices.

Indeed, failing to use the manipulator tag for the three countries that meet the criteria may be read by some as a transition to a lighter-touch approach by the new administration.

This may ultimately cause some countries to be more comfortable when intervening to curb their domestic currencies’ appreciation for trade advantages, which could become a dominant theme as global trade rebounds from the pandemic crisis and a resumption of the dollar downtrend (which is our base-case) offers room for emerging market currencies to appreciate.

We doubt that the Treasury and the current administration will be at ease with such a dynamic playing out, so we may see some further comments on the matter to reiterate that the Treasury remains firmly determined to fight currency manipulation.

Another risk is that the FX Report, and by extension the manipulator designation, might have lost some credibility considering the change in rules and approach from one edition to the other, suggesting it may still retain a strong political overtone. Furthermore, we suspect that the Treasury might have turned a blind eye to Thailand’s FX intervention, trusting the bilateral disclosure of intervention worth 1.9% of GDP (right below the 2% threshold) by Thai authorities. As in the previous edition of the report, we estimate actual FX intervention was above 2% of GDP, but the lack of transparency about the calculations inevitably leaves some significant room for discretion, and possibly dents the report’s credibility.

In conclusion, we think it is still too early to make a full assessment of the Treasury’s stance on FX manipulation under Secretary Yellen, and we will need to see more FX Reports to gauge how those will be used to assist the US trade agenda. But, in general, we doubt the Treasury will allow the message of a softer approach to FX manipulation to consolidate among trading partners, so we remain of the view that once the dollar decline gathers pace again in the coming months (as per our expectations), EM countries (especially in Asia) may still feel some pressure to refrain from FX intervention, as their domestic currencies appreciate.

Incidentally, those countries that take steps to tighten policy as their domestic recovery gathers pace might struggle to keep up the pace of intervention without this being seen as a clear mercantilist maneuver.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more