The ECB’s Dashboard And Implications For Asset Markets

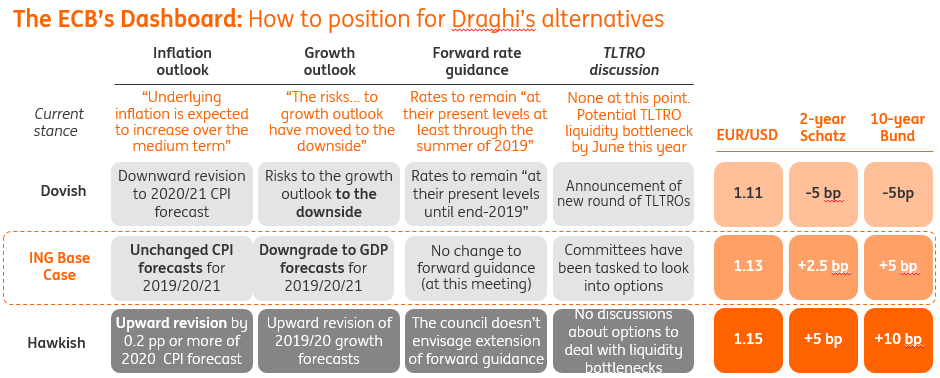

The cautious ECB tone this Thursday in the currently USD-supportive environment suggests modest downside to EUR/USD. We reiterate our 1- to 3-month EUR/USD forecast of 1.1200. The upside to bund yields remains limited. Figure 1 shows our ECB Dashboard

Source: Shutterstock

Source: ING

EUR: Still very limited near term upside

We don’t expect the euro to get much of a boost from the ECB meeting this week. The general message should remain cautious (see ECB preview: Trying not to get lost in transition for details) with the ECB attempting to avoid unintentional tightening of monetary conditions. Here a potential hint at further LTLROs should reinforce such a message.

With the ECB remaining cautious and the rate differential between the USD and EUR intact (if anything, it should widen again as markets start pricing in a 3Q19 Fed hike, cementing the dollar’s status of one of the high yielders in the G10 FX space), the upside to EUR/USD looks very limited in coming months. We reiterate our forecast for EUR/USD 1.12 for 1- and 3-month time horizons.

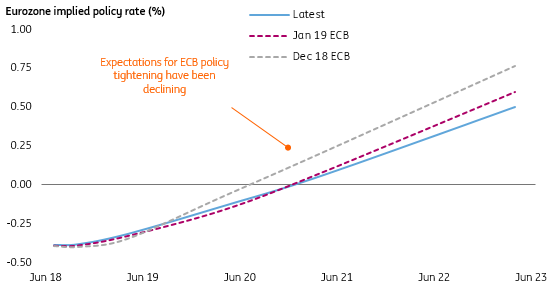

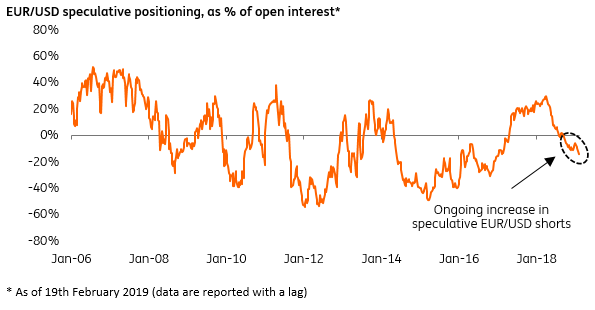

Indeed, the lack of catalysts for a more meaningful reversal in the dovish ECB stance (as per Fig 2, the market is assigning a fairly low probability to any meaningful ECB tightening in coming quarters) as well as the non-negligible costs of shorting USD vs EUR have been some of the factors behind why the speculative community has been reducing EUR longs or increasing EUR shorts over recent weeks (Fig 3).

Market assigning a low probability to any meaningful ECB tightening

Source: ING, Bloomberg

While Eurozone data may improve, this is unlikely to translate into a hawkish ECB stance

While we see a lack of near-term catalysts for EUR/USD upside, we also think the downside to the cross is limited, particularly if EZ data improves (as per Eurozone PMI: early signs of an economy pulling through, the EZ Feb PMIs showed the first tentative signs of EZ data bottoming).

However, we note that unless any positive EZ data surprise translates into a shift in the ECB stance (from the current cautious one to a more hawkish stance) the scope for an idiosyncratic EUR rally (as was the case in 2017 when the market started pricing in ECB QE tapering) is fairly limited. Indeed, the EZ data surprise index increased modestly in February while the US index fell sharply (in large part due to poor December US retail sales). EUR/USD remained flat and didn’t benefit from the relative reversal in the data surprises.

We see it as unlikely that the ECB will deliver a meaningful tightening during this cycle (as CPI will remain below the target) meaning that any meaningful EUR/USD upside should be a function of the peak in the USD cycle (and subsequent across-the-board USD softness) rather than ECB generated euro strength.

Speculative EUR/USD shorts rising modestly

Source: CFTC

Bond markets: Fairly limited upside to bund yields

Our base case looks for yields being biased slightly higher as a wait-and-see stance might not be enough to live up to market expectations. More clarity on a potential new round of TLTROs seems to be the base case, where “tasking committees” would be the bare minimum. Should hints emerge of the new operations being conducted at less generous terms, the bias higher in rates could be felt even more in Eurozone periphery bond yields, though. Still, ECB reluctance to act now should not lead markets to price out a low-for-longer scenario, meaning the upside in yields should be limited.

Disclosure: None.