Switzerland: Deep Into FX Manipulation Territory

The Swiss National Bank unveiled CHF 90bn of FX intervention in 1H20, worth more than 50% of GDP. Switzerland is well above the other two US Treasury thresholds in the period July 2019 - June 2020, but the autumn report is unlikely to be published before the US election. Still, labeling bears the risk of generating fresh CHF speculative buying.

SNB interventions confirm Switzerland could be named FX manipulator

Despite normally disclosing the size of currency interventions once a year (in the Annual Report), the SNB announced today that it engaged in currency interventions worth CHF 90bn in the first half of 2020. This narrowly exceeds 50% of Switzerland’s GDP.

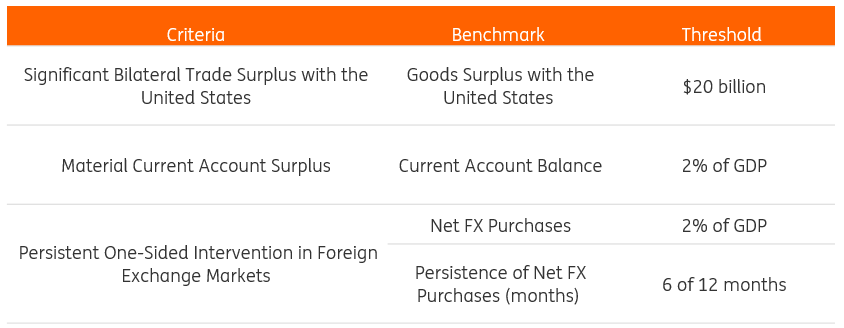

The figure is a mere confirmation of the large deployment of the FX intervention tool by the SNB to curb the strong appreciation pressures on the franc as the Covid-19 pandemic erupted. Still, a key issue is whether this will cause Switzerland to be labeled a currency manipulator by the US Treasury. Speculation about possible labeling generated upward pressure on the franc back in January when the US Treasury put Switzerland on its watchlist as it met two of the three criteria to receive the manipulator label. These criteria, and the quantitative thresholds, are reported in the table below.

Source: US Treasury, ING

In our latest preview of the US Treasury Semi-Annual FX report – which was due in May, but hasn’t been published yet – we highlighted how Switzerland was already meeting the first two criteria (trade surplus with the US and current account surplus) in the period covered by the report (Jan-Dec 2019) and was very close to the 2% threshold on the third (FX intervention) - which we estimated at 1.9% of GDP in that period.

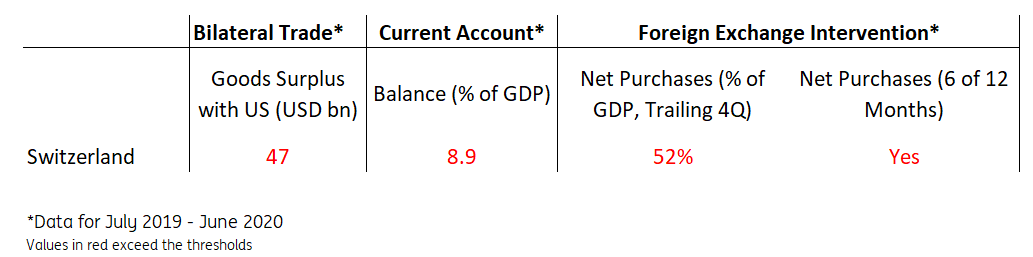

FX intervention has now been revealed to be around 50% of GDP (we estimate 52% if we take 4Q rolling sums) in 1H20, and a look at the SNB FX reserves leaves little doubt that the Bank has engaged in net purchases for at least 6 of the 12 months (we count at least 8) ending June 2020. The period July 2019 – June 2020 will be covered in the autumn edition of the Treasury FX report, which is usually published in October, but given the spring report is still to be published, it may not be drafted before the end of the year.

Still, we estimate that Switzerland has continued to exceed the trade surplus and current account surplus thresholds in the period July 2019 – June 2020, and would therefore meet all criteria to receive the FX manipulator designation (table below).

Source: ING, US Census, IMF, SNB

Does the US have an interest in labeling Switzerland?

With the US Treasury FX report having adopted strong political overtones since trade disputes took centre stage, the decision to label any country a currency manipulator will likely have to fit in the US trade/geopolitical agenda. A testament to this is the fact that the only country to receive the label in recent years was China, in August 2018, despite the country only meeting one of the three criteria.

While we have previously noted how Vietnam, Taiwan, and Thailand all exceeded the three thresholds in the 2019 calendar year, we suspected that geopolitical implications with relation to China may still spare them the unwanted label.

For Switzerland, geopolitics aren't playing a key role but there are other factors at work. The report covering July 2019 – June 2020 is unlikely to be published before the US election, and a potential change in the presidency may also imply a more light-handed approach to trade relationships. Even if President Trump stays in power, we cannot exclude that a free pass would be granted due to the extraordinary environment caused by the pandemic.

At the same time, there is a chance the Treasury decides to make an impromptu statement (like it did when labeling China) and declaring Switzerland a manipulator without publishing the full report.

Implications may be limited, but CHF speculative buying may emerge

Assuming that Switzerland is designated a currency manipulator, the implications for the country (and for trade relations with the US) would not be immediate. The Treasury provides for a period of negotiations with the monetary authority of the designated country to establish different FX intervention practices. Only if negotiations fail are more drastic measures, such as tariffs, recommended.

The implications could, however, be more significant from a market perspective, as many investors may suspect that the SNB will be forced to review the upper-bound of its tolerance band for CHF, allowing the currency to appreciate more freely. This may generate intense speculative bullish bets on CHF, putting the SNB in the uneasy position of having to increase its FX intervention despite having received the manipulation label.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more