Sustainable Markets

The European Commission’s technical screening criteria for green buildings may not be a major game-changer for the issuance of green bonds, as long as issuers offer proper transparency regarding the extent their green bonds are taxonomy aligned with EU regulation. That said, the criteria could become an increasingly important differentiating factor.

In November last year, sustainable markets experienced some turmoil following publication of the European Commission’s draft delegated act establishing the technical screening criteria for climate change mitigation and climate change adaptation3. Climate change mitigation and climate change adaptation are the first two of the six environmental objectives set by the EU taxonomy regulation that came into force in July 2020.

The EU taxonomy regulation classifies economic activities as environmentally sustainable only if they meet one of the six sustainability objectives, do no significant harm (DNSH) to any of the other environmental objectives, are compliant with the defined minimum social safeguards, and comply with the technical screening criteria.

The EU taxonomy identifies the following six sustainability objectives

1) Climate change mitigation

2) Climate change adaptation

3) Sustainable use and protection of water and marine resources

4) Transition to a circular economy, waste prevention and recycling

5) Pollution prevention and control

6) Protection and restoration of biodiversity and ecosystems

The technical screening criteria will be set by separate delegated regulations. The criteria for climate change mitigation and climate change adaptation should become applicable per 1 January 2022, while the technical screening standards for the other objectives will be established at a later stage and should apply from 1 January 2023.

The finalisation of the technical screening criteria is, for many financial market participants and financial advisers, the anxiously awaited missing piece of the taxonomy puzzle. After all, as of 10 March 2021 they have to disclose to what extent their financial products or investments qualify as environmentally sustainable under the sustainable finance disclosure regulation (SFDR). Knowing whether their products or investments meet the technical screening criteria is therefore key.

However, finalising the technical screening criteria is proving to be a longer process for the European Commission than initially anticipated. The main reason is the flood of questions raised during end of last year’s consultation period regarding the November draft proposals. In particular, the technical screening criteria proposals for buildings received substantial pushback from sustainable market participants.

The green buildings criteria issue: the shift from best-in-class to EPC

Within the draft delegated act, the European Commission proposed to subject buildings built before 31 December 2020 to a class A energy performance certificate (EPC) requirement. For some countries, this would leave a negligible part of their building loans as eligible, as:

- Parts of the building stock would not have EPC labels to begin with, while

- Only a small part of the labelled buildings have an A class EPC certificate.

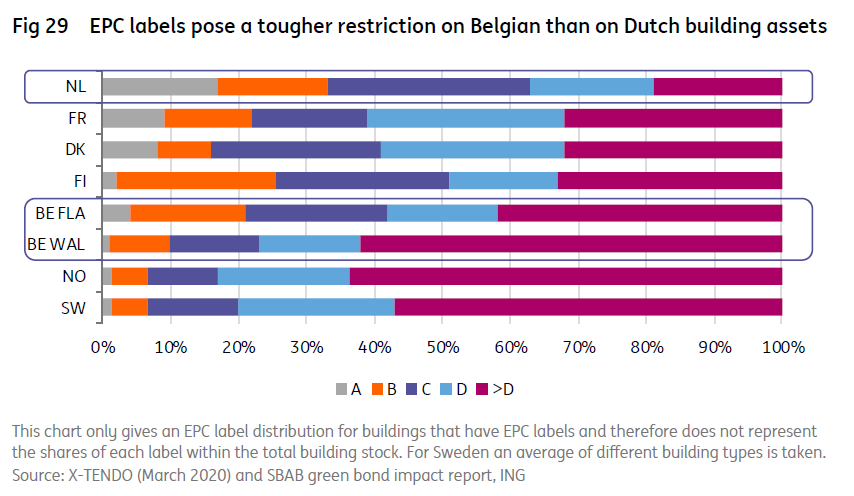

The Benelux makes a good example of the regional differences. The Belgian market is impacted far harder by this criterion (1-4% of the buildings are EPC class A) than the Netherlands where 17% of the labelled properties have an A certificate (Figure 29).

This should get better over time on the back of all the national incentives to improve the energy efficiency of existing buildings through renovation. Think, for example, of the EPC label premium introduced in Flanders, which offers a lump sum contribution of as much as €5,000 for renovations to label A. However, these renovation processes will take time. Meanwhile banks and asset managers seeking to contribute to the financing of the energy transition in buildings may be hindered in doing so by the tight EPC straitjacket.

Understanding national EPC label differences is a hard nut to crack

That many were caught off guard by the European Commission’s proposals for green buildings can be explained by the shift that was made versus the technical screening criteria recommendations of the Technical Export Group (TEG) in March last year4. In line with market practice, the TEG proposed the use of a best in class approach, where green buildings should belong to the top 15% low-carbon buildings. Certification schemes such as EPCs could be used as evidence of meeting the top 15% requirement. However, the TEG explicitly refrained from mentioning a minimum EPC reference level, recognising that more work needed to be done in order to define the absolute thresholds corresponding to the top 15% of the building stock.

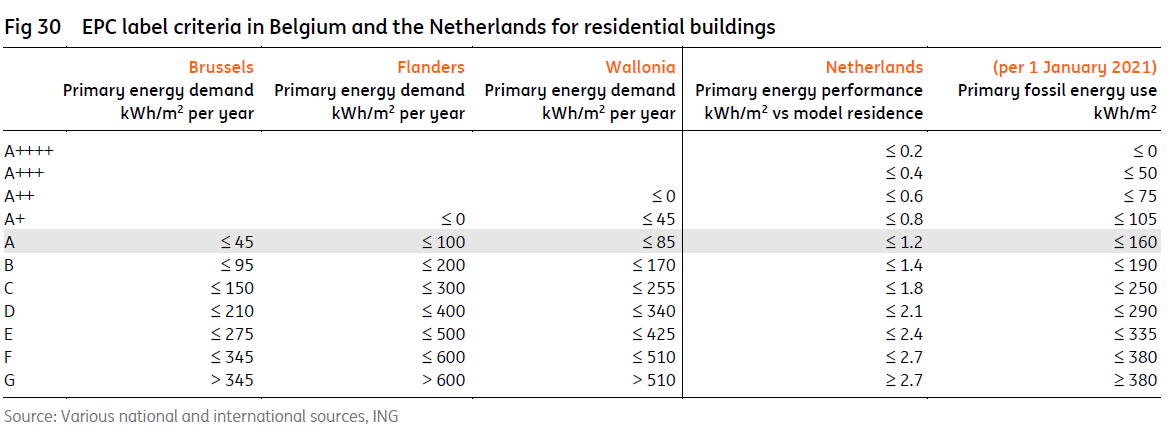

Indeed, it is commonly known that EPC labels differ widely from country to country and often lack comparability. Some countries use primary energy demand as a reference, while others refer to final energy use. Some jurisdictions have set their EPC label requirements on a country level, whereas elsewhere EPC definitions are set on a regional level and may vary from region to region. In some regions, the EPC criteria may differ per property type (for instance, houses versus apartments or residential versus commercial buildings). While most label definitions are ultimately based on a measure of the energy used in kWh/m2/y, there are also countries that express their labels in terms of a building’s energy performance in comparison to a reference building. For those that do, even the simple definition of a reference building is far from uniform. Figure 30 highlights some of these applicable differences for the Netherlands and Belgium. The result is that countries that have set the strictest A label definitions, may be harmed the most by technical screening criteria that use EPC labels as a reference for green buildings.

So what now?

Given the amount of push back received by the European Commission regarding the draft technical screening criteria for buildings, it is by no means certain that the EPC label of A will remain the key reference for buildings built before 31 December 2020. It may very well be that the European Commission will re-introduce the 15% best in class approach in line with the TEG proposals, and/or loosen the EPC label criteria to include an EPC label of B. The latter would align the EPC label reference for buildings with the European Commission’s ‘do no significant harm’ to climate change mitigation proposals under the climate change adaptation objective. An EPC label B reference would also be in line with the TEG’s first technical screening criteria recommendations. Both would allow banks to identify a significantly larger portfolio of taxonomy aligned assets for green bond issuance purposes than under the current EPC label A recommendations.

However, the latter option (broaden the EPC label criterion to include class B buildings) would still not solve the fact that differences in national EPC label methodologies may result in buildings being labelled A or B in one country, while for a country with a similar type of building stock but stricter EPC criteria, a comparable building could be labelled C. Another complicating factor is that, for banks issuing green bonds, it is often not as straightforward as it may seem to know, or otherwise obtain, the required EPC label information for their mortgage lending books. This is why issuers often rely on year of construction information to be able to identify the 15% most energy efficient buildings.

That said, even in the worst-case scenario where the EPC label of A is maintained as a technical screening criterion for existing buildings, banks may still continue to apply a 15% best in class approach. This would give them ample opportunity to issue green bonds while, for investors, transparency on the percentage of the green asset portfolio that is taxonomy aligned may withstand. After all, for SFDR disclosure purposes it should be sufficient for investors to know which share of their bond investments can be considered environmentally sustainable under the taxonomy’s definition.

However, while an A label outcome does not necessarily have to hinder the primary market activity in green bonds, it could become a differentiating factor to the performance of green bonds. After all, financial market participants are likely to search for those bonds in particular that provide them with a high taxonomy alignment, or otherwise request more compensation from bonds that are less taxonomy aligned.

The impact on Benelux green bonds

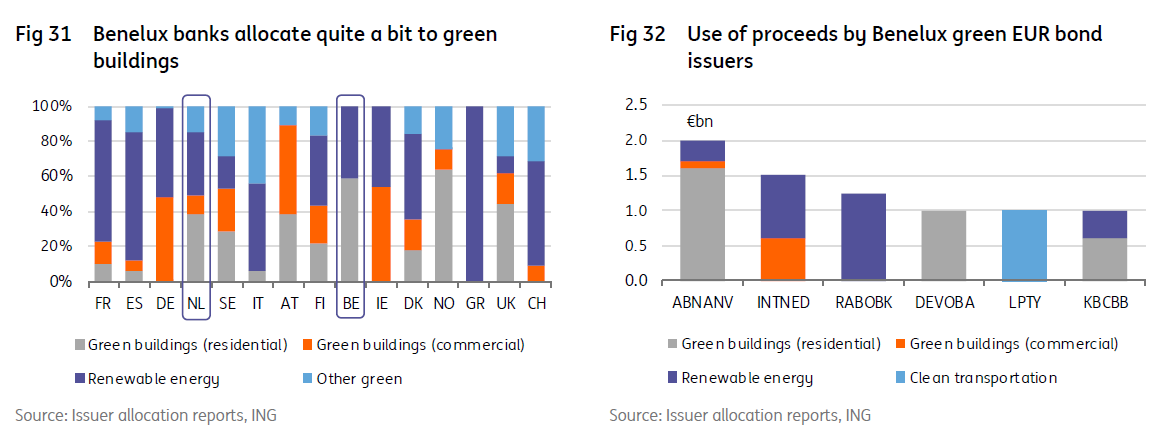

The Netherlands and Belgium are among the markets for which the technical screening criteria for green buildings is of high relevance for the green bond issuance by banks. After all, 49% and 59%, respectively, of the (non-covered) green bond proceeds in these markets has been allocated to green building assets. In other markets, such as France and Spain, almost 70% of the green bond proceeds is allocated to renewable energy loans.

Nonetheless, even in the Benelux market the use of proceed differences are substantial. Some allocate 100% of their green bond proceeds to residential buildings, while others allocate 100% of their proceeds renewable energy loans, or to clean transportation.

Banks that are not impacted by the strict building criteria because they allocate their proceeds to other assets, such as renewable energy loans, may face less difficulty meeting the technical screening criteria and may see this being rewarded with a better taxonomy alignment and consequently tighter pricing levels for their green bonds.

However, as discussed above, the Netherlands is one of the few countries in which the portion of building assets in the EPC label category of A is quite high. For that reason, Dutch banks already apply a minimum EPC label of A as one of the asset eligibility criteria for green buildings in their green bond frameworks.

KBC remains the only Belgian issuer of green bonds to date. The issuer’s current green bond framework does not use EPC labels as its selection criterion. Instead, for residential real estate assets the requirements of the Flemish Region building code as of 2014 or later (E-level ≤ 60) are used as a reference, under the condition that the first drawdown has occurred after 1 January 2016.

Figures 33 to 36 give an overview of the current trading levels of Belgian and Dutch green bonds versus vanilla adjacents. KBC’s green bonds trade modestly through the issuer’s non-green bonds, whereas on the Leaseplan curve such tighter spreads are not visible.

Whether technical screening criteria considerations already play a role in these observations remains difficult to say. Factors such as scarcity (ie, fewer green bonds outstanding), size, or alternatives outstanding in the green bond’s maturity bucket also play an important role when looking at the relative spreads of green versus vanilla bonds. This may well be the reason why other green bonds issued by Benelux banks are quoted notably less through non-green comparables than the two bonds highlighted.

Besides, the technical screening criteria for climate change mitigation and climate change adaptation are not set in stone yet and will only apply as of 2022. Nonetheless, we do believe that once these criteria are finalised, investors may already start prepositioning themselves by focusing on buying bonds that will allow them to tick the box “taxonomy aligned” to the largest possible extent.

In that regard, Dutch green bonds, including those with proceed allocations towards buildings, could stand to benefit versus other green bonds with building allocations. This would particularly be the case if the technical screening criteria for building assets were to stay as they are in the current Commission proposals. This advantage would clearly diminish with the reintroduction of a 15% best in class approach, which in the end would still be the preferable outcome for the broader green bond market.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more