Rates Spark: In For The Long Haul

The ECB signaled it is in for the long haul, with longer than expected extensions to its main facilities. We summarise the outcome of the meeting in a table below. These add to near term economic worries in justifying low EUR rates.

Source: Shutterstock

Overnight: still not over the hill

Additional covid-related restrictions imposed in Germany and France over the Christmas period promise to weigh on investor sentiment at the open today. Overnight price action was fairly uneventful for bond futures but stocks were on the back foot. EURUSD rallied overnight, approaching its highest level since early 2018.

ECB: QE for longer

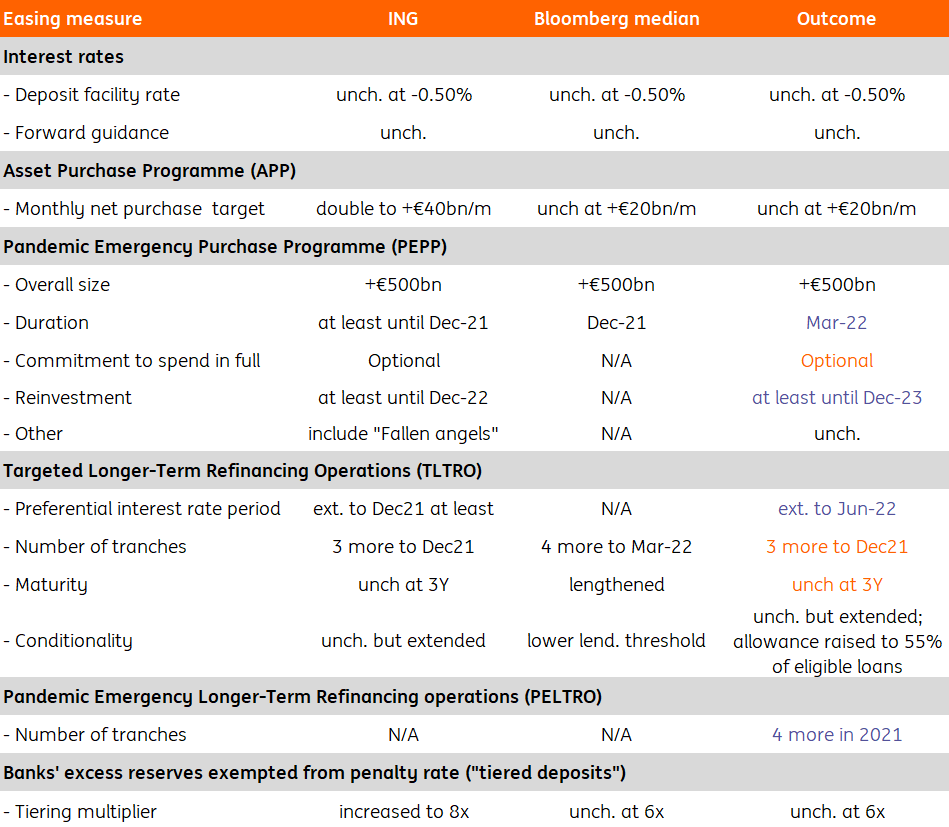

As our economics team noted, the best way to look at yesterday’s ECB package is as an extension of current accommodative monetary conditions until at least the spring of 2022. The €500bn increase in the PEPP asset purchase envelope was as expected, and the dovish risk we flagged before the meeting, of a longer extension than December 2021, was realized. The only fly in the ointment is that at the current pace of roughly €15bn/week, purchases can continue until June 2022, later than the stated March 2022 end date.

This brings two risks. Either the ECB does not spend the whole envelope in full, something Lagarde flagged as a possibility, or purchases carry on for longer than planned. Given that the ECB is only forecasting inflation at around 1.4% in 2023, we are tempted to think the dovish interpretation is the correct one. A third possibility is that of a materially faster pace of purchases which would also be a dovish outcome..

ECB beats expectations on duration

Source: Bloomberg, ECB, ING

TLTRO loans: preventing repayment

On the other main policy announcement, the extended terms for the TLTRO loans to banks, the new 12 month-long preferential interest rates period adds to our conviction that suppressed Euribor fixings are to remain a feature for at least another 18 months. Granted, reaching the new lending threshold will be more difficult for banks than the current one, but we argue it was difficult for the ECB to make that threshold lower than 0% loan growth. Combined with three more 3Y allotments in June, September, and December 2021, this should ensure less repayment pressure as the current preferential interest rate period comes to an end.

EUR rates: gloom persists

All in all, we see no basis for EUR rates gyrations around yesterday’s meeting, other than, as we have warned, so many policy tweaks were bound to deliver mixed messages. It is true that this package was all but priced beforehand, but we find it hard to overstate the importance of this level of easing maintained for at least another 15 months.

It is conceivable that the absence of any deposit rate cut came as a disappointment, thus explaining the bear-flattening yesterday, but we doubt many expected one. At the longer end, we see no strong rationale for 10Y EUR swap rates to diverge from our -0.30% year-end target (-0.60% for 10Y Bund), as markets brace themselves from prolonged covid-related disruptions to the economy.

Today's events: EU summit, US data, bond funding outlooks

Today is the second day of the EU summit.

The main data of note will come from the US: PPI and university of Michigan sentiment.

In government bond primary markets the eyes remain on the 2021 issuance outlooks. Today the Netherlands will publish its outlook for next year after having issued slightly more than €40bn in bonds this year. The German funding outlook can be expected for next week.

Over the past days, we have seen the funding outlook from France, which has indicated an unchanged €260bn of bond issuance (net of buybacks) in line with preliminary guidance. It also flagged the possibility of a new 30Y and a 50Y bond via syndication plus plans for a new 20Y green bond. Elsewhere, Ireland flagged a €16-20bn bond funding target for next year, compared to €24bn this year.

Today Belgium will tap two 5Y bond in an optional reverse inquiry auction for €0.5bn completing its supply for the year.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more