Rates markets are inclined to see the economic glass as half full. Today’s Eurozone core CPI could add to the bond market’s torments. Whether or not Lagarde leans against 2022 hike expectations tomorrow, we’ll soon be looking at the whole EUR bond market trading with positive yields.

US real yields start to creep higher again

The ease back lower in US real rates post the FOMC had been a head-scratcher. Post yesterday's ISM release though, real yields have headed higher again, taking with it the 10yr back to the 1.8% area. The prices component of the ISM was the main catalyst. It's spike to the mid-70's shows that even on weakening Omicron-impacted activity, the residual inflation issue in fact only intensifies, necessitating delivery on all that hawkish Fed rhetoric.

The 5yr has also re-cheapened on the curve, having been richening in the past week or so, which had been a bit strange. The 2yr yield has also popped higher post the data (back to 1.2%). There was nothing in the data to suggest that the Fed should calm its intentions. Friday will see an Omicron-impacted weak payrolls report though. The market should be ready for it, and should focus on the wages component over the jobs one. We'll likely wait till then before the next big move.

Rates markets see the glass half full… of inflation and a tightening job market

In a week that was supposed to feature soft economic data and a prudent messaging from the ECB, the natural expectation would have been quieter trading conditions, and a slowdown in the relentless rise in EUR traded interest rates. Higher-than-expected Eurozone inflation changed that. Even if expectations of a soft growth patch over the winter months prove correct, the underlying trend of price increases and tightening job market is keeping bond markets on the back foot.

How does the ECB address these developments is an open question. Governing council members have actually rung a similar note in their public appearances over the past few months. By and large, they have been busy hedging their bets. As is understandable when the range of possible economic outcomes is particularly wide, the ECB has sought to retain as much flexibility as possible. We see its decision to set QE purchase on a clear downward path in December as a manifestation of this willingness to keep its options open.

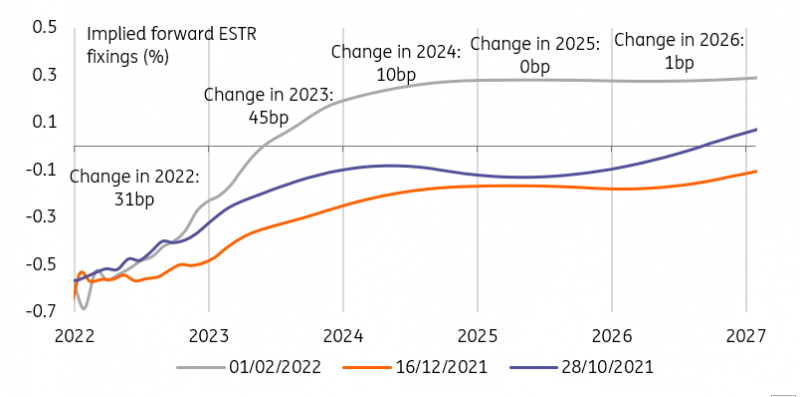

The market's belief in a 2022 ECB hike is growing

Source: Refinitiv, ING

Will Lagarde double down on no 2022 hikes?

In that same vein, it is debatable whether Lagarde will reiterate the message that no rate hike is forthcoming this year at tomorrow’s meeting. There is no easy option here. Repeating this message would make a change of tack in case of further upside inflation surprises all the more difficult, with the risk of an even sharper rates sell-off this carries. On the other hand, a lot of credibility has been invested in that message and rates markets might be tempted to price an even more aggressive path for the ECB’s deposit rate if Lagarde fails to repeat it tomorrow.

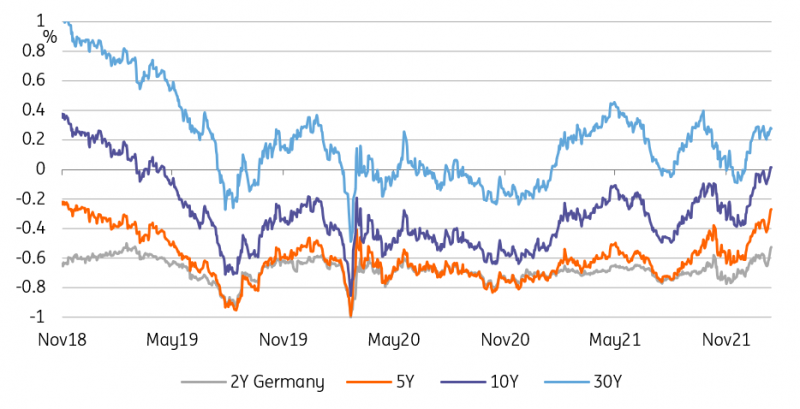

The whole of the German curve is set to trade with a positive yield next year

Source: Refinitiv, ING

Whether or not the ECB admits the possibility, the front-end is increasingly in the driving seat of the EUR curve. In Germany, 10Y yields are settling above 0% and the 2Y above the ECB’s deposit rate. As the tightening cycle approaches, it makes sense for 2Y bonds to yield more than an overnight rate, and this is a sign of things to come. As the ECB rushes to bring the deposit rate to 0% next year, we’ll soon be looking at the entire German curve trading above 0%, and by extension, the entire EUR bond market.

Today’s events and market view

Italy has mandated banks for the launch of a new 10Y inflation-linked bond which we expect to price today. Past deal sizes in the sector suggest the issuer will aim for €4bn.

The main release on today’s economic calendar is the Eurozone January CPI print. Given the Spanish, Germany, and French upside surprises, it is fair to say that markets have been primed for a high print. Nevertheless, an elevated core CPI reading would heighten the stakes of tomorrow’s ECB meeting.

In the US, the main item on an otherwise quiet release calendar is the ADP employment change. Expectations are low ahead of Friday’s payroll number and yesterday’s jump in job openings reinforced the view that the main factor constraining job growth is labor supply rather than demand.

In its quarterly refunding announcement today, the US Treasury will give the maturity breakdown of US Treasury supply.

Comments

Log in or sign up to join the conversation.