Rates Spark: ECB All-In As The Fed Eases Back

Interesting to see the Fed ease back on the need for Wall Street support, as the market self heals. Meanwhile the ECB remains all-in with lots more to do. Month-end typically sees curves flatten. The move could reverse next week provided sentiment continues to improve. Long-dated ECB purchases have so far helped flatten the curve.

Source: ECB, ING

EUR Rates to remain suppressed into month-end

Optimism is palpable in financial markets, for instance in the stock market rally and in the tightening of sovereign spreads. Rates remain stubbornly low, however. This is a discrepancy we have highlighted recently and that looks set to persist for the foreseeable future as our economics team expects the ECB to announce €500bn of QE purchases at next week’s meeting, and an extension of the PEPP programme until mid-2021. We expect the announcement is largely priced in so a one-off impact on the day is possible but should be limited. Indeed the majority of economists surveyed by Bloomberg expect the same size and extension as us. Two weeks ago, the median of a Reuters survey was €375bn.

Ahead of this, we expect rates to trade in lockstep with stocks but to somewhat outperform what one would normally expect. We explain: month-end rebalancing flow should help to flatten yield curves and push rates lower. This effect is temporary and should unwind at the start of next week provided the current wave of optimism can extend until then. This is not a given. We regard simmering geopolitical tensions as a key risk in the coming sessions. Trump said he will announce further sanctions against China today whilst a Chinese probe into Japanese and US exports was extended today.

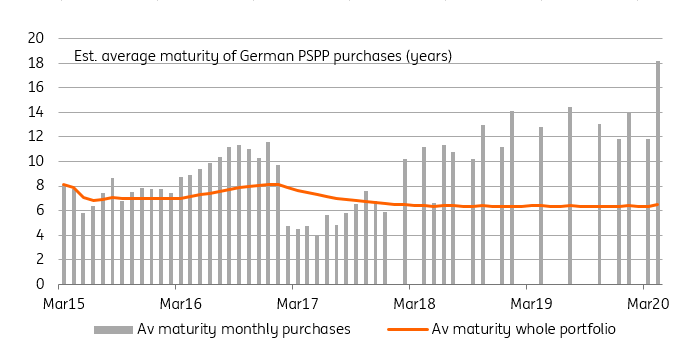

ECB purchases helped keep the German curve flat

The ECB has so far proved a tailwind for curve flatteners in Germany due to the long duration of bond purchases. We show in the chart above our estimate for the average maturity of monthly gross PSPP German bond purchases. In some months, the purchases are simply too small to make a decent guess. In April however, we think the average maturity was above 18 years, a record. Since average maturity numbers are published on a monthly basis, we will only be able to provide an estimate for May when new statistics are released next Tuesday. This should also be the first opportunity to look at the country breakdown of PEPP purchases, which are only released bi-monthly.

Overall Fed support for wall street continues to ease

Latest data (for last week through to the close on Wednesday) optically shows big increases in use of the commerical paper and corporate credit support facilities, but this is reflective not of increased support but of the transfer of equity support for these facilities from the US Treasury.

The underlying spend on the corporate credit market through ETF purchases remained in the range of US$1-2bn. So the annualized amount being spent is still in the US$35bn area when we calculate through to September. This remains quite tame compared with a possible spend of up to US$750bn.

At the same time, a bigger spend is not really needed as the market continues to self-heal against record corporate issuance numbers, that illustrates a near fully functioning credit market.

And its a similar story elsewhere, coming from another reduction is support needed for money market funds, as this fell by another US$4bn. And loan support for primary dealers was also down by another US$2bn, showing that this market is well capable at this point of standing on its own feet.

Spending on a paycheck protection programme illustrates a continued need to support mainstreet (or smaller corporates more precisely). This was up US$4bn. There was also a US$2.4bn increase in central bank liquidity lines, showing that off-shore requirements for US dollars remain elevated.

Stress eases on Wall Street but remains elevated on Main Street, and off-shore pressure too remains in play.

Today's events: Euro area flash inflation, Italian bond sales

In data, we will see releases of Euro area inflation estimate for May, with market consensus seeing a drop of the headline rate to 0.1% from 0.4% year-on-year on the back of a drop in energy prices. The core inflation rate is seen slightly lower at 0.8% versus 0.9% in the prior month. Deflationary forces stemming from the economic damage of the pandemic will keep inflation depressed, and as Banque de France's Villeroy argued earlier this week low inflation provides the ECB with room to act "rapidly and powerfully". We will also see the final GDP figure for France and Italy - given the extraordinary circumstances statisticians are facing revisions might be larger than usual.

Italy will be active in the Eurozone government bond primary market, selling up to €7.5bn across 5Y and 10Y bonds and a floating rate note. Italian bonds have enjoyed a decent tailwind from the bold EU recovery plans. The 10Y spread of Italian BTPs over Bunds has narrowed to close to 190bp after starting the week at around 215bp. The prospect of more ECB purchase capacity to be announced very soon seems to have been largely priced in to give the muted reactions to dovish ECB comments, but we would regard that as a necessary precondition for any benign spread dynamics.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more