Poland: Retail Sales Miss Estimates While Construction Outperforms

In October, not much was left of the sales boom recorded in the second and third quarters, but the drop was much shallower than at the beginning of the first wave. Construction and assembly production reported slightly better results.

Shoppers at the Poznan City mall in Poland

The gap in sales is widening

Retail sales in October dropped by 2.3% YoY in real terms vs. 2.5% YoY in September. The consensus was for a 0.7% YoY decline. Seasonally adjusted figures indicate a drop of 2.1% month-on-month, hence the level of sales in October was around 4.0% lower than in February, the period before the first wave of the pandemic. In September, the gap was 2%.

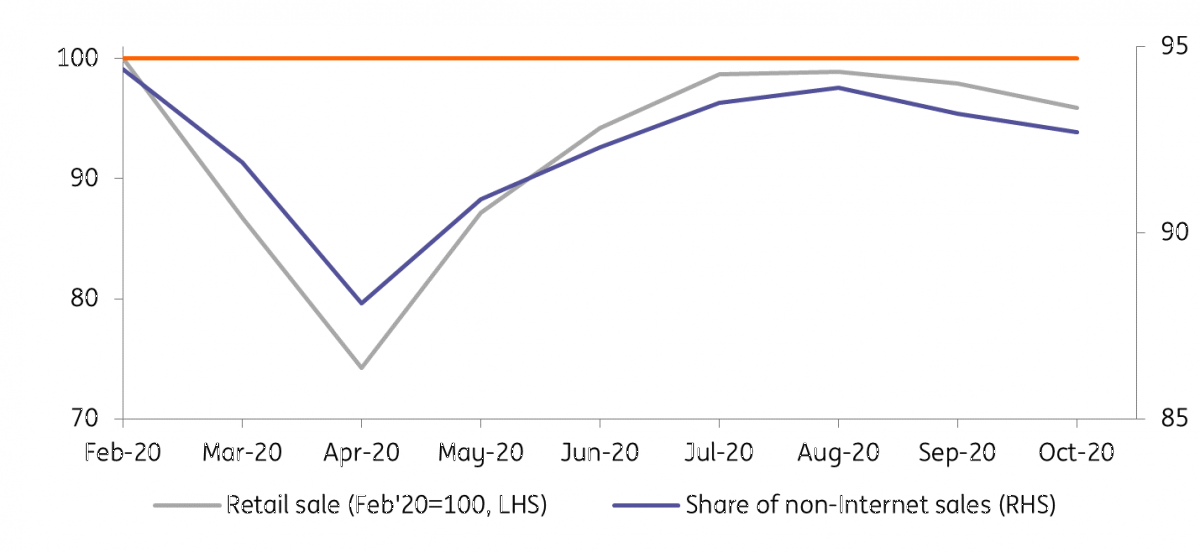

In October, similar to September, the share of internet sales increased. A strong increase in the internet share was last recorded in March and April. However, the chart below shows that, at least for the time being, the internet will not replace traditional sales channels. To date, the increase in the share of internet sales has coincided with a decrease in the total sales volume.

Retail sales, volume against share of non-internet sales

Detailed data shows a decrease in car sales in October, falling by 8.0% YoY after 4.9% YoY growth in September. Fuel sales also deteriorated. Clothing sales fell sharply, probably due to the still-warm autumn weather.

On the other hand, sales growth continued to be high for furniture, consumer electronics, and appliances: 11.9% YoY in October vs. 8.6% YoY in September. This shows the shift in demand towards durables after service consumption restrictions were introduced. Poles forced to work and study at home are also adapting their properties to their new role.

What the transactional data shows

Our data on payments shows that the sale of goods (i.e. the one described by today's data) performed much better (in October and early November) than the sale of services. Before the announcement of new safety restrictions by the government, Poles were probably stocking up on goods. In the week following the restriction announcement, turnover actually fell but remained at a relatively high level. The situation in services was much worse - transactional data indicates that the level of turnover, e.g. in culture and recreation, is similar to that of 2Q20. That's why we estimate that the service sector suffered the most in November. The last assessment of the economic situation by companies operating in the area of accommodation and food services is already almost as bad as in April this year when historic lows were recorded. As in 2Q20, services will see a deeper correction, while sales of goods will be smaller. Today's data shows that the pandemic shock in 4Q20 will be shallower than that recorded in 2Q20.

The industry will suffer relatively less during the second wave of Covid-19 - the government action are directed to maintain the economic situation in this sector, which is additionally supported by the still good economic data from Asia.

Construction and assembly production slightly above expectations

Data on construction and assembly production was better than expected. In October, it fell by 5.9% YoY vs. 9.8% YoY in September. The relative improvement is mainly due to smaller declines in the group of civil engineering facilities and specialized construction. The data on EU funds' disbursements shows a large jump of 37.5% YoY in 3Q20 and 6% YoY in October.

Production in this sector still remains clearly below last year's levels, although there are already optimistic signals. While in September, the seasonally-adjusted figure was at a similar level to August 2020, in October, it recorded a 1.8% m/m increase. On a monthly basis, growth continues to be recorded by companies engaged in specialized works, which may suggest an acceleration of infrastructure investment in the coming months.

What do we see in the October figures?

We already have information on the performance of key monthly hard data from the Polish economy in October. The annual growth rates of industry and retail sales were worse than in September, construction and assembly production recorded a smaller decline. However, this is already history. The second wave of the pandemic resulted in a sharp tightening of administrative restrictions and a restriction of population mobility in November. Our index aggregating this data is now more than 20 points below the October average (this is as much as two-thirds of the drop between April and March 2020 when the first wave of Covid-19 hit). In November the business climate in manufacturing, construction, trade, and services fell sharply. Our trading partners also introduced severe restrictions to sustain the next wave of Covid-19. November will bring further economic slowdown.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more