Image Source: Unsplash

April retail sales growth was supported by low base effects, “consumption smoothing” by domestic consumers as well as purchases by and for refugees from Ukraine. Construction output growth eased and has serious headwinds ahead. In June, the MPC may hike the main policy rate by 100bp in order to curb inflationary pressure

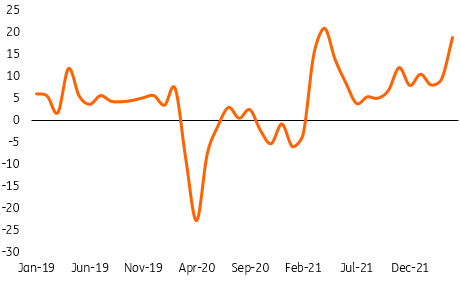

Strong retail sales from a low reference base

The consumer boom continues. In April, retail sales jumped by 19.0% year-on-year (ING: 16.7% YoY; consensus: 16.1% YoY). Such a strong annual growth was facilitated by a low reference base from April 2021, but that is not the only explanation for the strong reading.

Retail sales, %YoY

GUS.

Buoyant consumer spending is supported by solid domestic demand. Soaring prices have not significantly reduced purchases as consumers continue to spend despite higher price levels. The monthly seasonally-adjusted real data for different sales categories looks robust. This is all happening despite high inflation, very poor consumer sentiment, and uncertainty caused by war. Demand for goods is fuelled by rising wages and fiscal expansion, including tax cuts.

The inflow of refugees from Ukraine is an additional boost to consumption, particularly in sales of clothing and footwear (up by 121.4% YoY). The high volatility of sales in this category is also linked to the lifting of Covid-19 restrictions.

The implied retail sales deflator increased to 12.1% YoY in April from 11.3% YoY in March. Consumer demand remains robust and high price pressures persist.

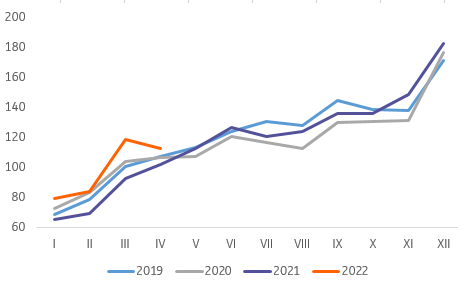

Construction activity slows amid declining home sales

Signs from construction are clearly less optimistic as activity softened visibly last month. Construction output rose by 9.3% YoY vs. an increase of 27.6% YoY in March (ING: 16.6%YoY; consensus: 18.7%YoY). Seasonally-adjusted data points to a 5.1% MoM decline. The decline in activity was broad-based, however, the smallest monthly drop was reported in civil engineering, due to ongoing spending of local and EU funds on infrastructure. The coming months will be tough for residential construction due to: (1) the hit to housing demand from higher interest rates and more restrictive regulations, (2) the sharp upswing in prices of materials, and (3) mounting shortages of labor, including outflows of Ukrainian workers and (4) elevated uncertainty linked to the war in Ukraine.

Construction output, 2015=100 (S.A.)

GUS.

Bottom line

The beginning of 2Q22 brings buoyant consumer demand and persistently high price pressures. Retail sales data, although somewhat distorted by a low reference base, points to strong consumer demand. This could fuel second-round effects (producers passing higher costs onto output prices). The scale of upward pressure on producers’ costs is reflected in the PPI index, which jumped by 23% YoY in April, so companies have higher costs, which should drive up inflation in the coming months.

Data on retail sales, PPI, and wages provide strong arguments for further interest rate hikes. The MPC should take further policy action in order to prevent inflation from spiraling. In June, the MPC may hike the main policy rate by 100bp. We still see the NBP reference rate at 7.5% this year and the terminal rate at 8.5%, with upside risk.

Comments

Log in or sign up to join the conversation.