Headline inflation in Spain increased sharply in April for the second consecutive month in a row. We were expecting it not least because of a sharp increase in energy prices compared to a year ago.

Prices are higher for people in Spain

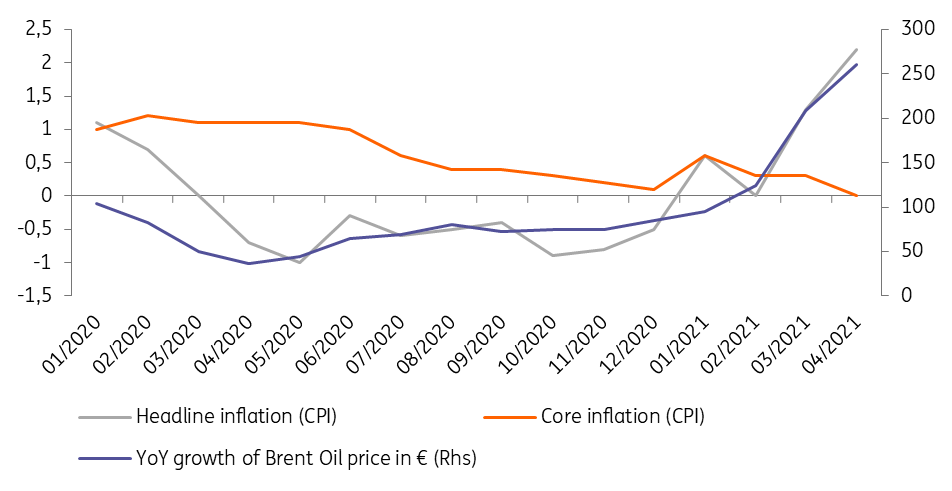

Headline inflation (CPI) rose from 1.3% in March to 2.2% in April. It is the second consecutive month that headline inflation has risen sharply but the reason's the same: Energy prices. Data on the components are not yet available, but the increase in the oil price compared to a year ago makes this obvious. Indeed, the Brent oil price in euros rose by about 260% YoY in April, while in March it grew by 208% YoY.

From next month onwards, we expect headline inflation to come down again, as the energy price impact will start to fade, albeit very slowly. So the sharp increase over the last two months is nothing to worry about.

It is all about energy price inflation

Core inflation (excluding energy, food, alcohol, and tobacco) dropped ever further from 0.3% in February and March to zero in April. This implies that the current level of economic activity is not putting upward pressure on prices that are non-energy related. We expect that core inflation is likely to edge higher once the economy reopens. During the last couple of months, prices in the Recreation and Culture and Restaurants sectors and Hotels were dropping. Once the economy reopens, with a more active tourism sector, we expect that this trend will turn. This should push core inflation up.

Given the difficult start of the year, with a postponement of the economic recovery, as result, it is not surprising that the labor market was not able to recover further in the first quarter of 2021. But at the same time, the impact of the surge of infections and corresponding restrictions at the beginning of 2021 was limited. Employment fell by 0.71% (or 137.500 persons) compared to the previous quarter. This is much more limited compared to the second quarter of 2020 when employment fell by 5.5%.

Today’s figures look worrying at first sight, but shouldn’t be. The surge in headline inflation was expected due to the sharp increase in energy prices, while the weaker labor market figures are explained by the surge of the pandemic during the first quarter. GDP growth figures for the first quarter will be published tomorrow. We expect that the economy will have contracted in Q1 by about 0.5%, but that this will likely be the end of the economic contraction

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.