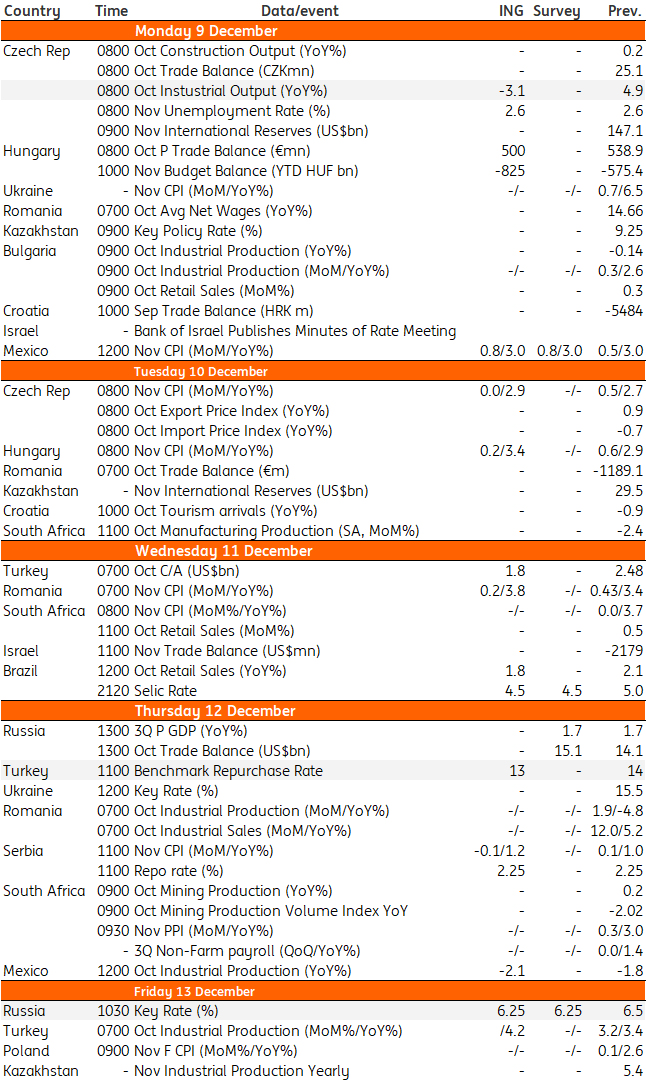

Next Week's Key Events In EMEA And Latam

A packed calendar in EMEA next week - the focus will be on Turkey's and Russian's central bank meetings which should result in a cut following lower than expected inflation numbers. Also, keep an eye out for Czech industrial production and inflation reading from Hungary.

Turkey: Expect a cut

Given the downside surprise in November inflation, improving inflation expectations, currency stability and low-interest-rate environment globally, we expect the central bank to act, with a modest 100 basis point rate cut, pulling the policy rate down to 13%. Read our full preview here.

Russian's central bank likely to cut

In November, CPI continued to underperform expectations (3.5% YoY) while inflationary expectations in November reached their lowest levels since April 2018, so it is possible that December CPI will approach the lower bound of the CBR's target of 3.2-3.7%, building the case for a 25 basis point cut in the key rate in December.

With few internal obstacles, only a negative external surprise (including a hawkish Federal Reserve) could prevent the CBR from cutting.

Hungary: All eyes on inflation

The most important release in Hungary next week is the inflation reading. With previous price increases in energy products falling out of the base, there is upward pressure on the year-on-year headline rate. Against this backdrop, we see fuel prices along with more expensive food items pushing the headline reading up 3.4% from a year ago. As inflation in market services is expected to strengthen further, core inflation could rise to 4.1% year-on-year. However, as tax effects remain significant, core inflation excluding indirect taxes is expected to come in at 3.8%, an 11-year high. Separately, we expect the budget to post a notable deficit in November due to seasonal factors, but the year-to-date reading should remain significantly better than planned.

Czech: Industrial production still on a downward path amid weaker foreign demand

October industrial production will fall in YoY terms – mainly due to the calendar bias, as October had one less working day. But even the adjusted figures should confirm the trend of previous months, i.e. stagnation or a slight YoY decline in domestic industrial production due to weaker foreign demand.

November inflation will be the most interesting release next week, however, as there is potential to hit the 3% upper tolerance band if food prices increase more than 0.4% month-on-month. Even weaker monthly growth will push annual food prices significantly higher due to the base effect, from 2.8% in September to more than 4.5% YoY, which will increase the contribution of food prices to YoY CPI growth by 0.3 percentage points. If inflation does break the 3% upper tolerance band, it will be because of volatile food prices and this isn't likely to affect the CNB's decision to stay on hold in December.

EMEA and Latam Economic Calendar

(Click on image to enlarge)

Source: ING, Bloomberg

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more