Image Source: Pexels

The Central Bank of Turkey looks set to complete its tightening cycle as soon as possible while maintaining its hawkish stance in order to ensure sustained price stability. After one more hike in January, we expect the bank to remain on hold until the third quarter.

Turkey at a glance

- In its monetary policy strategy for 2024, the CBT summarised its planned policy actions: i) targeting an increase in the share of TRY deposits to 50% in the banking system and sustaining the fall in the FX-protected deposit scheme. Accordingly, FX-protected deposit accounts converted from TRY deposits will not be opened or renewed as of 1 January, while banks will continue to be able to open and renew FX-protected deposits that are converted from FX ii) maintaining its reserve build-up strategy and uptrend in international foreign currency reserves iii) implementing further quantitative tightening and taking steps in the simplification process iv) limiting its securities portfolio to TRY 200bn v) continuing to conduct swaps with banks; it plans to gradually reduce the amount of swap transactions..

- There has been renewed demand for portfolio investments among non-residents, and hence, we have seen around US$3.4bn of inflows (including repos) to government debt instruments and US$1.9bn into equities in the eight weeks to 22 December. Since June, cumulative portfolio inflows have reached US$7.2bn (US$2.9bn into stocks, US$4.3bn into debt instruments).

- Net reserve accumulation has gained pace since mid-November. Accordingly, the CBT’s net FX position (excluding swaps) has been on the rise, reaching -US$36.5bn as of 22 December from US$-56.7bn on 10 November, though the last week of 2023 witnessed a decline in both gross reserves (US$-4.4bn) and the net FX position (US$-1.1bn).

- Supported by the rise in foreign inflows to Turkish assets, the recovery in reserves implies total net FX purchases of close to US$20bn between mid-November and year-end.

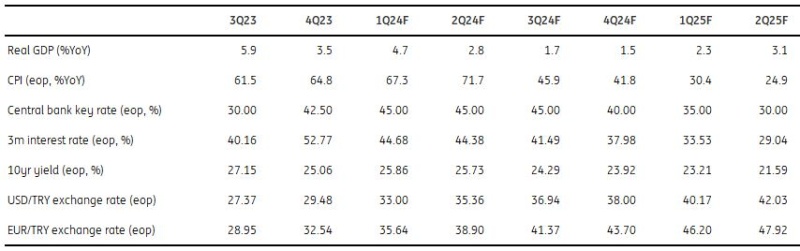

Quarterly forecasts

Image Source: Various sources, ING

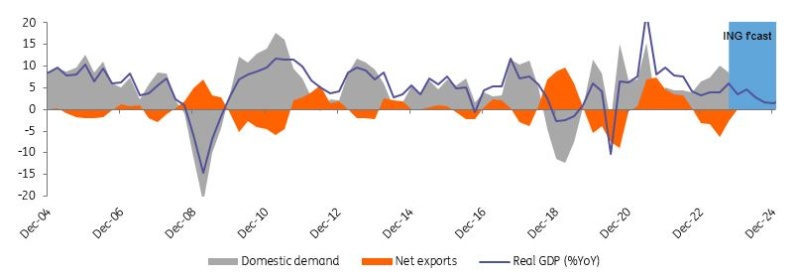

Normalisation in domestic demand is still slow

Despite the earthquakes in February, GDP recorded a strong 4.7% year-on-year rate in the first three quarters, mainly driven by domestic demand. However, there have been signs of a slowdown in the growth trend since the third quarter as the manufacturing PMI index has remained below the 50 threshold for the last five months, while confidence indices in all sectors, particularly in the corporate sector, have recorded moderate declines. Leading indicators for November also point to the continuation of the moderate slowdown trend. This development can be attributed to the effects of the ongoing slowdown in global activity on the manufacturing sector, the moderation in credit growth, and the tightening in monetary policy, which aim to normalize domestic demand. However, ongoing inflationary pressures will likely bring demand forward, and the local elections at the end of March may limit the impact of these developments in the short term. In fact, the monthly recovery in retail sales in October, strength in goods imports, and credit card expenditures suggest that the normalization in domestic demand is still relatively moderate.

Real GDP (%YoY) and contributions (ppt)

Image Source: TurkStat, ING

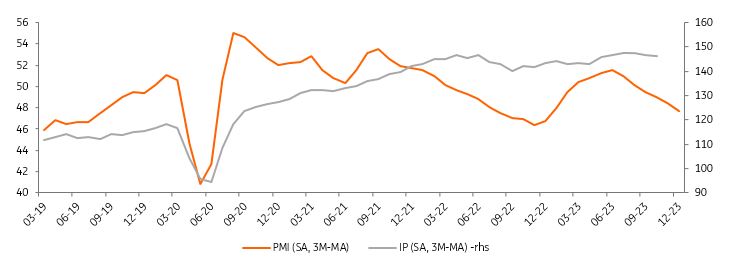

Industrial production continued to contract

In October, calendar-adjusted industrial production (IP) recorded a 1.1% YoY increase, while the seasonally- and calendar-adjusted index dropped by 0.4% month-on-month, signaling a continued loss of strength. However, extending its decline to the fourth month, seasonally adjusted IP has remained close to the pre-earthquake levels. While heavy-weight manufacturing production and electricity & gas dropped on a month-on-month basis, mining has remained in positive territory, supporting the industry sector performance. In the breakdown, a sequential contraction in capital and non-durable consumer goods determined the monthly performance, despite slight increases in intermediate goods, durables, and energy. Among the sub-groups of the manufacturing industry, the manufacture of other transport equipment (dominated by defense industry products) pulled the headline down most by subtracting 0.7ppt, followed by computer, electronic, and optical products, and clothing. Among the total number of 24 sub-sectors of the manufacturing industry, 13 of them recorded a drop on a monthly basis. This shows that the loss of momentum in production continued moderately at the beginning of the last quarter.

IP vs PMI

Image Source: ICI, TurkStat, ING

Strength in October retail sales

Retail sales volumes on a calendar-adjusted basis increased by 13.7% YoY in October, the lowest monthly reading in 2023, though the seasonally and calendar-adjusted index showed a sharp 2.0% recovery on a sequential basis after two straight months of decline. The data implied that domestic demand growth, which lost strength in the third quarter, started the last quarter with an improvement. Among subgroups, non-food and food sales increased by 3.0% MoM and 0.9% MoM, respectively, while automotive fuel sales dropped by 0.2% MoM. The highest annual increase in non-food sales was observed in computer and communication devices group at 6.5% MoM. On the other hand, the (seasonally-adjusted) unemployment rate inched down to 8.5% in October, the lowest rate since late 2012, from 9.0% a month ago. In the breakdown, male unemployment is at the lowest point of the current series, which began in 2005, at 7.0%, while the improvement in female unemployment has remained relatively limited at 11.3% vs the series low of 7.8%.

Retail sales vs consumer confidence

Image Source: TurkStat, ING

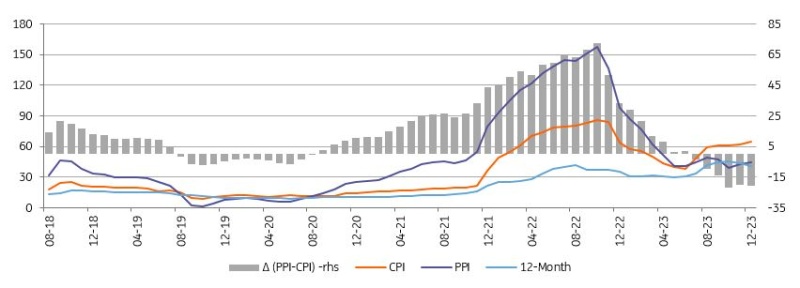

Inflation rises in December

With monthly inflation at 2.93%, slightly below consensus, annual inflation in 2023 turned out to be 64.8% YoY (vs the CBT's forecast in the latest inflation report of 65%), increasing from 62% a month ago on the back of higher food and energy prices. October PPI, on the other hand, stood at 1.1% MoM, translating into 44.2% YoY. The decline in annual PPI from close to triple digits at the end of last year shows improvement in cost pressures despite the YoY increase in the TL equivalent of import prices due to commodity price developments and exchange rate increases. Core inflation (CPI-C) came in at 2.31% MoM, inching up to 70.6% on an annual basis on the back of pricing behavior, exchange rate developments, adjustments in administered prices, and inertia in services. On a seasonally-adjusted basis, headline inflation remained broadly unchanged in the last month of 2023 despite increasing goods inflation as services recorded the lowest monthly reading last year, offsetting the impact from the goods.

Inflation outlook (%)

Image Source: TurkStat, ING

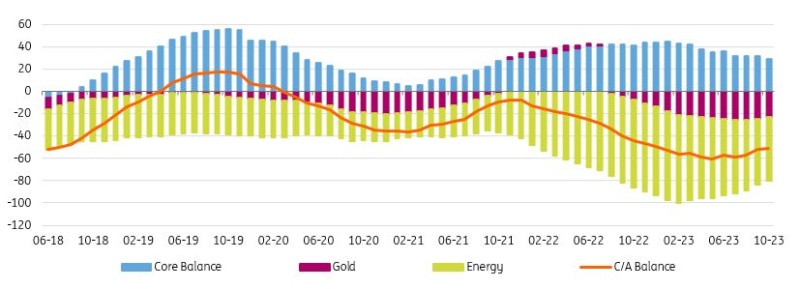

The current account mildly improved in October

Standing at US$+0.2bn, the current account surplus in October came in lower than the consensus forecast and our projection (both US$+0.8bn). Accordingly, the 12M rolling deficit showed a mild improvement, at US$50.7bn (translating into c.4.8% of GDP) from US$51.7bn a month ago. The breakdown of monthly data reveals that the energy and gold balance were the major drivers, despite a narrowing core trade surplus and smaller services income with easing transport revenues. The capital account on the other hand witnessed net identified inflows of US$2.7bn. Net errors & omissions stood at US$-2.7bn (another outflow after US$-2.4bn in September) and reached US$-8.1bn on a year-to-date basis with significant fluctuations before and after the May elections. With the monthly c/a surplus and large outflow via net errors & omissions, official reserves recorded a mere US$0.2bn increase. In the first 10 months of 2023, registered capital inflows remained below the accumulated deficit, leading to a marked reserve depletion at US$10.7bn.

Current account (12M rolling, US$bn)

Image Source: CBT, ING

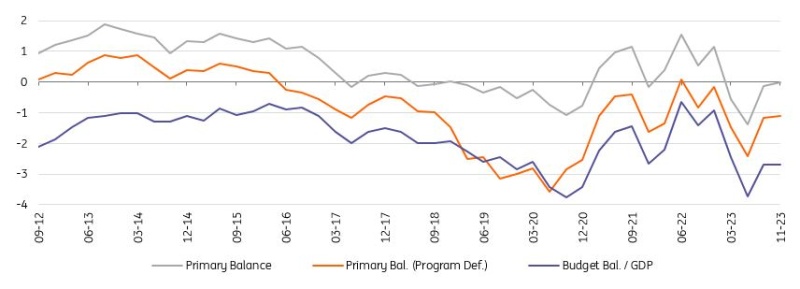

12M rolling deficit below the MTP target in November

November budget results showed a decline in the seasonal surplus to TRY75.6bn, down by 30%, on the back of i) the continued deterioration in non-interest due to the acceleration in transfers to SEEs and earthquake-related spending and ii) a significant increase in interest expenditures, despite strength in direct and indirect tax collection following the measures introduced after the elections. Accordingly, while the central government budget posted a deficit of TRY532.4bn in the first 11 months of the year, the deficit for the last 12 months reached TRY651.1bn (translating into c.2.7% of GDP). Additionally, the budget for 2024 was determined in line with the latest Medium Term Plan (MTP) and approved in the National Assembly. In the newly approved budget, earthquake-related spending is foreseen at TRY762bn in 2023 (vs TRY1,633bn total deficit) and TRY1,028bn in 2024 (vs TRY2,652bn budget deficit). Given this backdrop, the ratio of the budget deficit to GDP excluding earthquake expenditures is projected to be 3.4% in 2023 and 2024. This confirms that fiscal policy will not be fully helping the CBT in the disinflation process.

Budget performance (% of GDP)

Image Source: Ministry of Treasury and Finance, ING

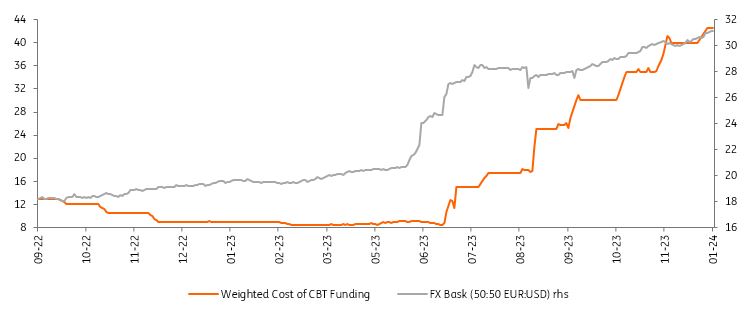

Slower pace of hike in December

Following its guidance in November and in line with the consensus, the Central Bank of Turkey (CBT) raised the policy rate by 250bp to 42.5% in the last rate-setting meeting of this year. After large rate hikes totaling 31.5ppt since June, the CBT signaled a slowdown in the pace of hikes to complete the tightening cycle in a short period of time. According to the December statement, however, the wording has changed a little stating that the tightening cycle would be completed as soon as possible. This is based on the bank’s assessment that the extent of monetary tightness is close to the required level to achieve disinflation. Regarding the micro and macro-prudential framework: i) the bank announced it would hold TRY deposit purchase auctions to strengthen the monetary transmission mechanism and increase the diversity of sterilization instruments ii) continuing its simplification moves, the bank also cut the security maintenance requirements on FX liabilities to 4% from 5% previously.

CBT funding rate (%) vs FX basket

Image Source: Refinitiv, ING

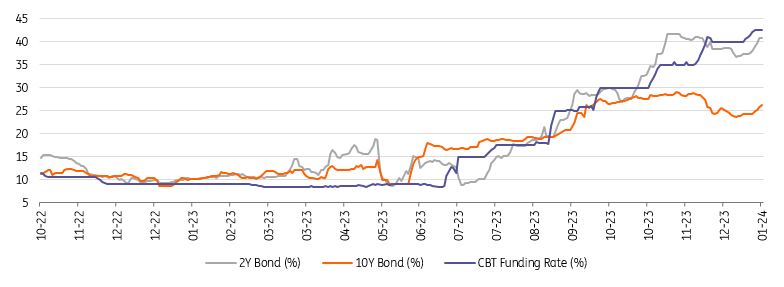

FX and rates outlook

While the central bank has maintained its hawkish stance and its commitment to monetary policy normalization, the carry has remained high as the terminal rate pricing has moved to near 45%. Despite relatively higher external debt repayments in the last two months of 2023, reserve accumulation accelerated in recent weeks with higher foreign inflows. Fundamentals on the balance of payments are expected to improve this year given that the policy-induced slowdown in the economy will support a recovery in the trade deficit and hence the current account balance.

Additionally, the sentiment in local debt markets has significantly improved since November. The risk-on mood and consequent foreign inflows have helped to reduce the risk premium and high government bond yields, and we have seen a strong rally with a downward shift in the yield curve. Accordingly, 2Y bonds rate dropped to around 36% from the 41-42% range in the second half of November. However, the global risk-off sentiment since the last week of December has led to an increase in yields back to around 40%. The 10Y bond yield, meanwhile, came down below 25% from around 28%, though has since risen close to the 26% level again. Whether foreign inflows continue will be key for the bond market in the period ahead.

Local bond yields vs CBT funding rate

Image Source: Refinitiv, ING

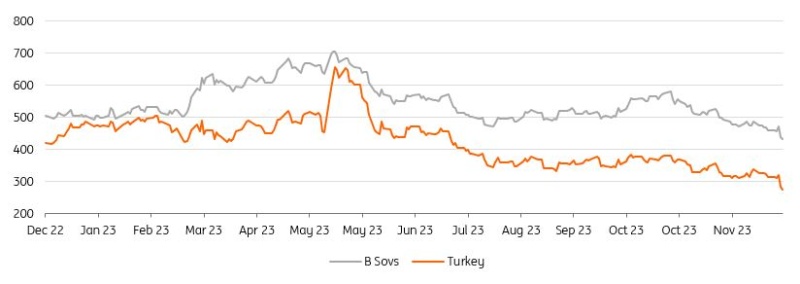

Sovereign credit: markets expecting rating upgrades

After a strong performance across 2023, investors in Turkey's dollar sovereign bonds will now be anticipating improvements in the nation's sovereign credit rating from the current (B3/B/B) levels, with Moody's upcoming planned review on 12 January in focus first. Despite credit spreads moving slightly wider to start the year, in line with the market movements, Turkey's dollar bonds remain, on average, around 150bp tighter than the single-B peer group.

If the central bank's commitment to monetary policy normalization continues in the coming months, further improvements in sentiment and more significant foreign inflows into local debt should support macro fundamentals, which could catch up with the move lower in sovereign risk premiums priced by the market. However, the path towards further gains will likely be bumpy given the speed of the rally seen last year, especially with new external debt supply already coming to market via the nation's banks, and local elections that could present headline risks in the coming months.

ICE US$ Bond Sub-Index Spreads vs USTs

Image Source: Refinitiv, ING

More By This Author:

Eurozone Unemployment Rate Falls To Historic Low In NovemberFX Daily: If In Doubt, Seek Carry

Asia Morning Bites For Tuesday, January 9

Comments

Log in or sign up to join the conversation.